HOUSE_OVERSIGHT_012082.jpg

{kind=link}

Extracted Text (OCR)

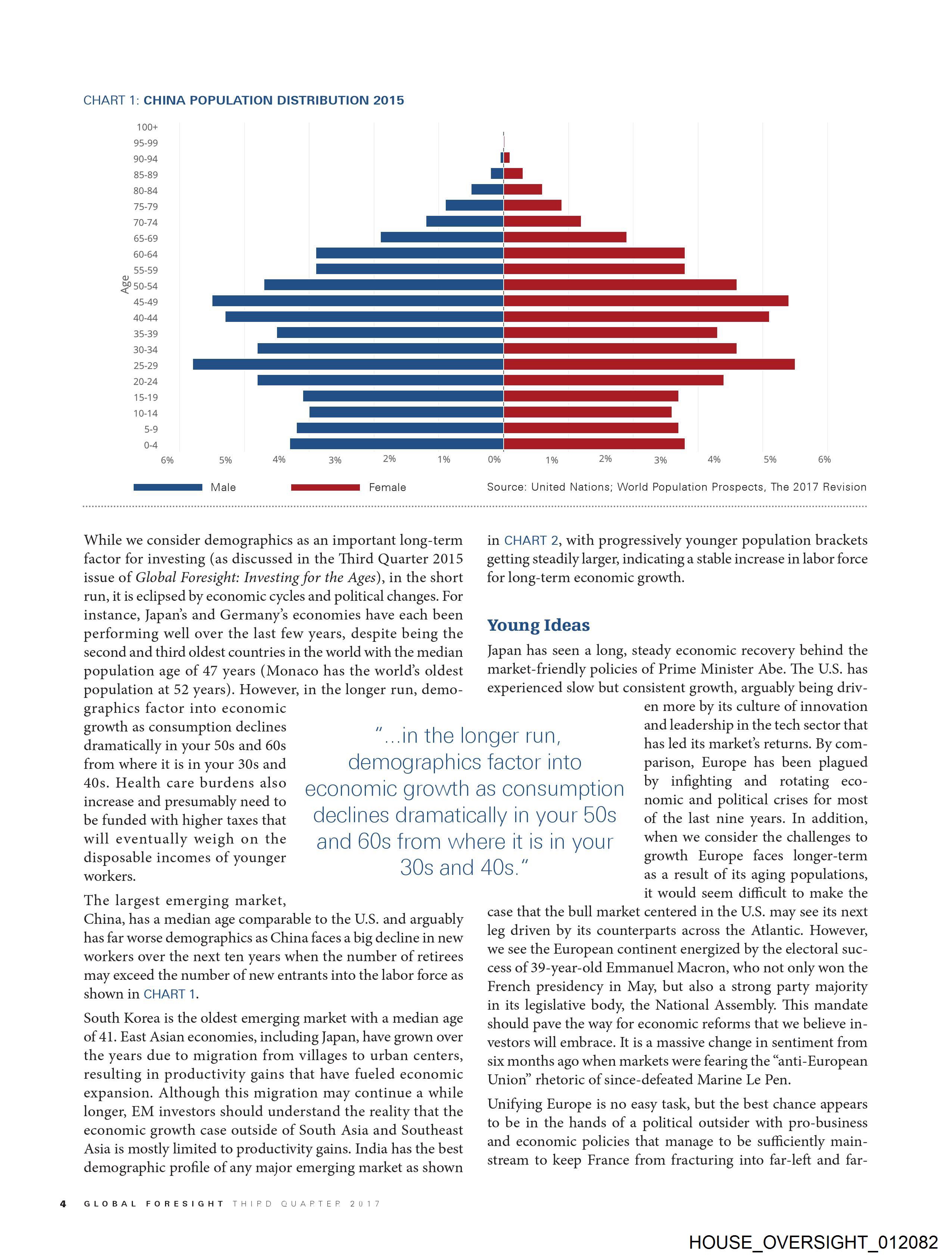

CHART 1: CHINA POPULATION DISTRIBUTION 2015

100+ ;

95-99 |

90-94 it

85-89 OE

80-84 eee ee

75-79 | |

70-74 a

65-69 EE

60-64 ee

y ed a

2950-54 NN EE—E>E=—E—E—E—E—Ee

45-49 ——_ee

40-44 Le

35-39 NN EE—E—E—E—E—E—E

30-34 CONE —————e——~E TE

25-29 _ eS ee

20-24 EEE

15-19 (I

10-14 aaa

5-9 EEE

0-4 (Ee

6% 5% 4% 3% 2% 1% 0% 1% 2% 3% 4% 5% 6%

While we consider demographics as an important long-term

factor for investing (as discussed in the Third Quarter 2015

issue of Global Foresight: Investing for the Ages), in the short

run, it is eclipsed by economic cycles and political changes. For

instance, Japan’s and Germany’s economies have each been

performing well over the last few years, despite being the

second and third oldest countries in the world with the median

population age of 47 years (Monaco has the world’s oldest

population at 52 years). However, in the longer run, demo-

graphics factor into economic

growth as consumption declines

dramatically in your 50s and 60s

from where it is in your 30s and

40s. Health care burdens also

increase and presumably need to

be funded with higher taxes that

will eventually weigh on the

disposable incomes of younger

workers.

The largest emerging market,

China, has a median age comparable to the U.S. and arguably

has far worse demographics as China faces a big decline in new

workers over the next ten years when the number of retirees

may exceed the number of new entrants into the labor force as

shown in CHART 1.

South Korea is the oldest emerging market with a median age

of 41. East Asian economies, including Japan, have grown over

the years due to migration from villages to urban centers,

resulting in productivity gains that have fueled economic

expansion. Although this migration may continue a while

longer, EM investors should understand the reality that the

economic growth case outside of South Asia and Southeast

Asia is mostly limited to productivity gains. India has the best

demographic profile of any major emerging market as shown

GLOBAL FORESIGHT THIRFD QUAPTER 2017

"...in the longer run,

demographics factor into

economic growth as consumption

declines dramatically in your 50s

and 60s from where tt is in your

30s and 40s."

in CHART 2, with progressively younger population brackets

getting steadily larger, indicating a stable increase in labor force

for long-term economic growth.

Young Ideas

Japan has seen a long, steady economic recovery behind the

market-friendly policies of Prime Minister Abe. The U.S. has

experienced slow but consistent growth, arguably being driv-

en more by its culture of innovation

and leadership in the tech sector that

has led its market’s returns. By com-

parison, Europe has been plagued

by infighting and rotating eco-

nomic and political crises for most

of the last nine years. In addition,

when we consider the challenges to

growth Europe faces longer-term

as a result of its aging populations,

it would seem difficult to make the

case that the bull market centered in the U.S. may see its next

leg driven by its counterparts across the Atlantic. However,

we see the European continent energized by the electoral suc-

cess of 39-year-old Emmanuel Macron, who not only won the

French presidency in May, but also a strong party majority

in its legislative body, the National Assembly. This mandate

should pave the way for economic reforms that we believe in-

vestors will embrace. It is a massive change in sentiment from

six months ago when markets were fearing the “anti-European

Union” rhetoric of since-defeated Marine Le Pen.

Unifying Europe is no easy task, but the best chance appears

to be in the hands of a political outsider with pro-business

and economic policies that manage to be sufficiently main-

stream to keep France from fracturing into far-left and far-

HOUSE_OVERSIGHT_012082

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_012082.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,810 characters |

| Indexed | 2026-02-04T16:15:42.693177 |