HOUSE_OVERSIGHT_014462.jpg

{kind=link}

Extracted Text (OCR)

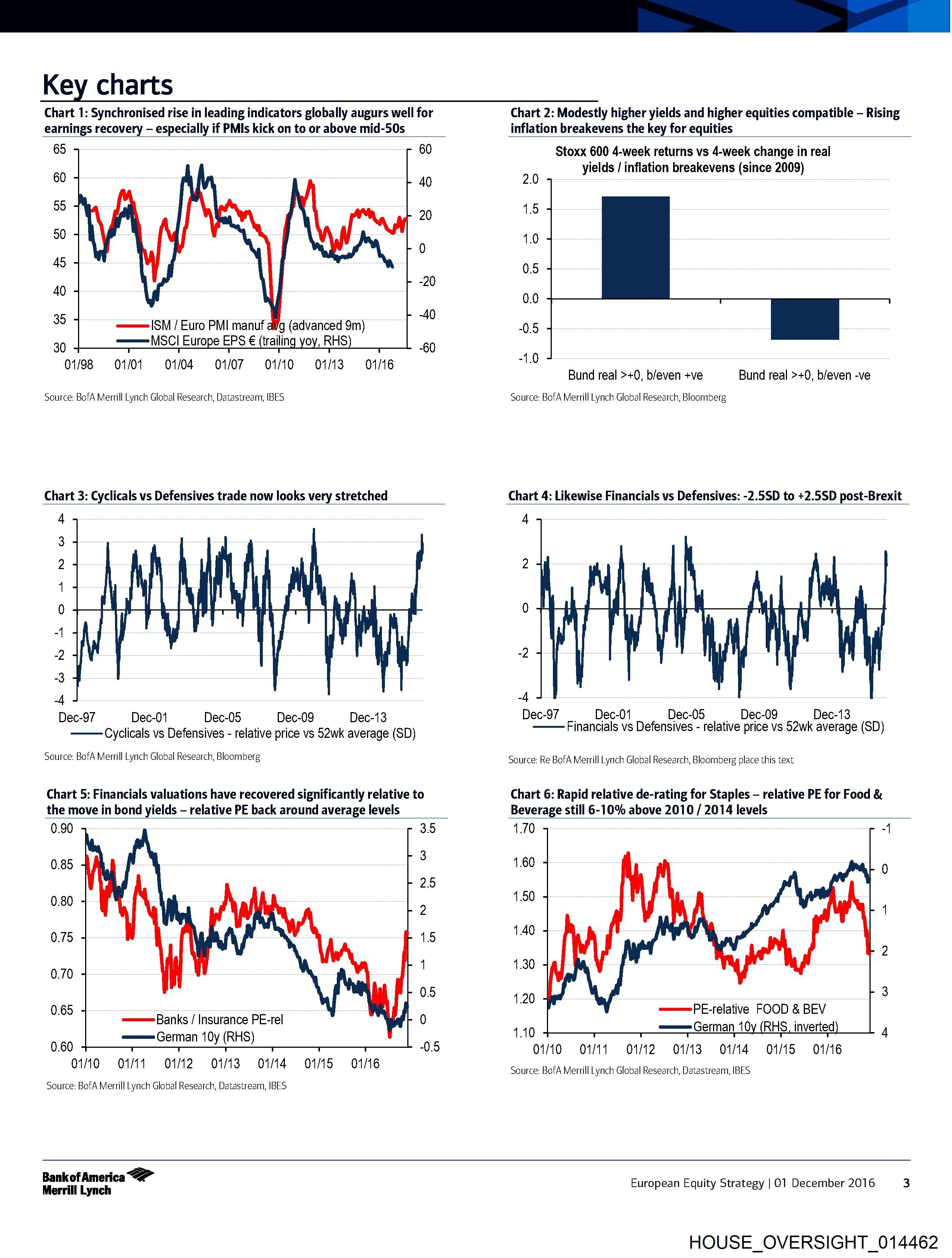

Key charts

Chart 1: Synchronised rise in leading indicators globally augurs well for

earnings recovery — especially if PMIs kick on to or above mid-50s

65 60

60 40

55 20

50

0

45

40 “20

35 ; 40

—— ($M / Euro PMI manuf alg (advanced 9m)

30 == |\iSCI Europe EPS € (trailing yoy, R 60

01/98 «= 01/01 0104 01/07 O10 O13 O16

Source: BofA Merrill Lynch Global Research, Datastream, IBES

Chart 3: Cyclicals vs Defensives trade now looks very stretched

4

3

2

1

0

|

-2

3

-4

Dec-97 Dec-01 Dec-05 Dec-09 Dec-13

Cyclicals vs Defensives - relative price vs 52wk average (SD)

Source: BofA Merrill Lynch Global Research, Bloomberg

Chart 5: Financials valuations have recovered significantly relative to

the move in bond yields — relative PE back around average levels

0.90 3.5

0.85 y 3

25

0.80 9

0.75 15

0.70 i

0.5

0.65 ——— Banks / Insurance PE-rel 0

0.60 == German 10y (RHS) 05

O1N0 =O1f1 O12 01/13 0104 O15 801/16

Source: BofA Merrill Lynch Global Research, Datastream, IBES

Chart 2: Modestly higher yields and higher equities compatible — Rising

inflation breakevens the key for equities

Stoxx 600 4-week returns vs 4-week change in real

an yields / inflation breakevens (since 2009)

1.5

1.0

0.5

0.0

0.5

-1.0

Bund real >+0, b/even +ve Bund real >+0, b/even -ve

Source: BofA Merrill Lynch Global Research, Bloomberg

Chart 4: Likewise Financials vs Defensives: -2.5SD to +2.5SD post-Brexit

4

4

Dec-97 _ _Dec-01 Dec-05 —_—— Dec-09 Dec-13

Financials vs Defensives - relative price vs 52wk average (SD)

Source: Re BofA Merrill Lynch Global Research, Bloomberg place this text

Chart 6: Rapid relative de-rating for Staples — relative PE for Food &

Beverage still 6-10% above 2010 / 2014 levels

1.70

1.60

1.50

1.40

1.30

1.20

———PE-relative FOOD & BEV

110 eee German 10y (RHS, inverted

01/10 = O1/11 =O1N2 «013 «01/14 =(01/15 (01/16

Source: BofA Merrill Lynch Global Research, Datastream, IBES

Bankof America

Merrill Lynch

European Equity Strategy | O01 December 2016 3

HOUSE_OVERSIGHT_014462

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014462.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 2,013 characters |

| Indexed | 2026-02-04T16:22:34.216433 |