HOUSE_OVERSIGHT_014465.jpg

{kind=link}

Extracted Text (OCR)

Marine Le Pen victory could bring into question both the future of the EU and also the

euro, should the polls be close it could make the uncertainty and market moves around

Brexit look like a walk in the park.

2017 - Reflation, Reversal, Rotation, Relief or Revolt?

2017 is likely to have a number of cross currents as themes. Recovery and Rotation go

hand in hand. The stronger the recovery the more yields can rise the more we can see

the rotation extend. Should investors become concerned that the recovery is stalling or

that yields are peaking the rotation would likely stall potentially even reverse. Reversal

refers to the ECB. Our economists are not yet convinced that the ECB will start to

unravel some of its easing measures in 2017 but they do expect the debate to be a

vigorous one within the ECB. For the first time Gilles Moec thinks there is a chance that

the ECB will indeed choose to taper. Relief or Revolt relates to the French election. Will

Europe follow the UK and US lead of 2016 and go down the route of populism (revolt

from the voters) or will we find relief for the markets if by the end of 2017 froma

Fillon/Merkel duo being in charge of the two largest economies in the Euro Area.

Recovery —- the world looks a better place going into 2017

Reflation has been the big theme of the second half of the year. As we had noted in

previous publications there had been something of an improvement in the global growth

picture emerging even before the US election. It started with Emerging Market growth,

which our GEMScycle has been showing to be accelerating for some months, but seems

to have spread to other parts of the developing world. US GDP for Q3 has just printed a

revised 3.2%, with a number of indicators, such as ISM’s, PMI’s and consumer

confidence pointing to a solid Q4 to follow. That quarter is currently tracking at 3.6%

according to the Atlanta Fed.

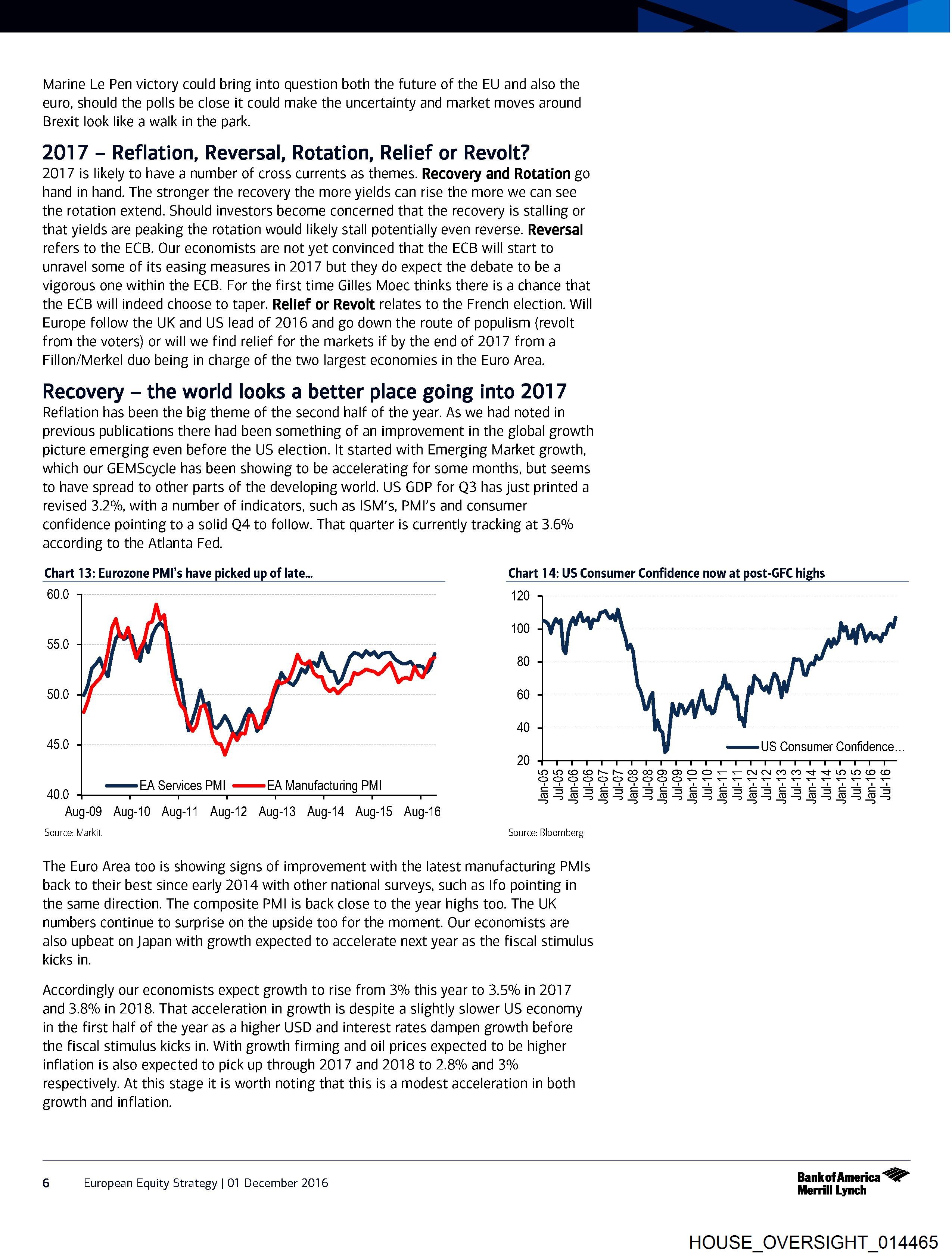

Chart 13: Eurozone PMI’s have picked up of late... Chart 14: US Consumer Confidence now at post-GFC highs

60.0 120

100

55.0

80

50.0 60

40

45.0 ——=US Consumer Confidence...

20

400 ——— EA Services PM] =====EA Manufacturing PMI

Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Source: Markit Source: Bloomberg

The Euro Area too is showing signs of improvement with the latest manufacturing PMIs

back to their best since early 2014 with other national surveys, such as Ifo pointing in

the same direction. The composite PMI is back close to the year highs too. The UK

numbers continue to surprise on the upside too for the moment. Our economists are

also upbeat on Japan with growth expected to accelerate next year as the fiscal stimulus

kicks in.

Accordingly our economists expect growth to rise from 3% this year to 3.5% in 2017

and 3.8% in 2018. That acceleration in growth is despite a slightly slower US economy

in the first half of the year as a higher USD and interest rates dampen growth before

the fiscal stimulus kicks in. With growth firming and oil prices expected to be higher

inflation is also expected to pick up through 2017 and 2018 to 2.8% and 3%

respectively. At this stage it is worth noting that this is a modest acceleration in both

growth and inflation.

BankofAmerica <2”

6 European Equity Strategy | 01 December 2016 Merrill Lynch

HOUSE_OVERSIGHT_014465

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014465.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,281 characters |

| Indexed | 2026-02-04T16:22:35.608374 |

Related Documents

Documents connected by shared names, same document type, or nearby in the archive.