HOUSE_OVERSIGHT_014468.jpg

{kind=link}

Extracted Text (OCR)

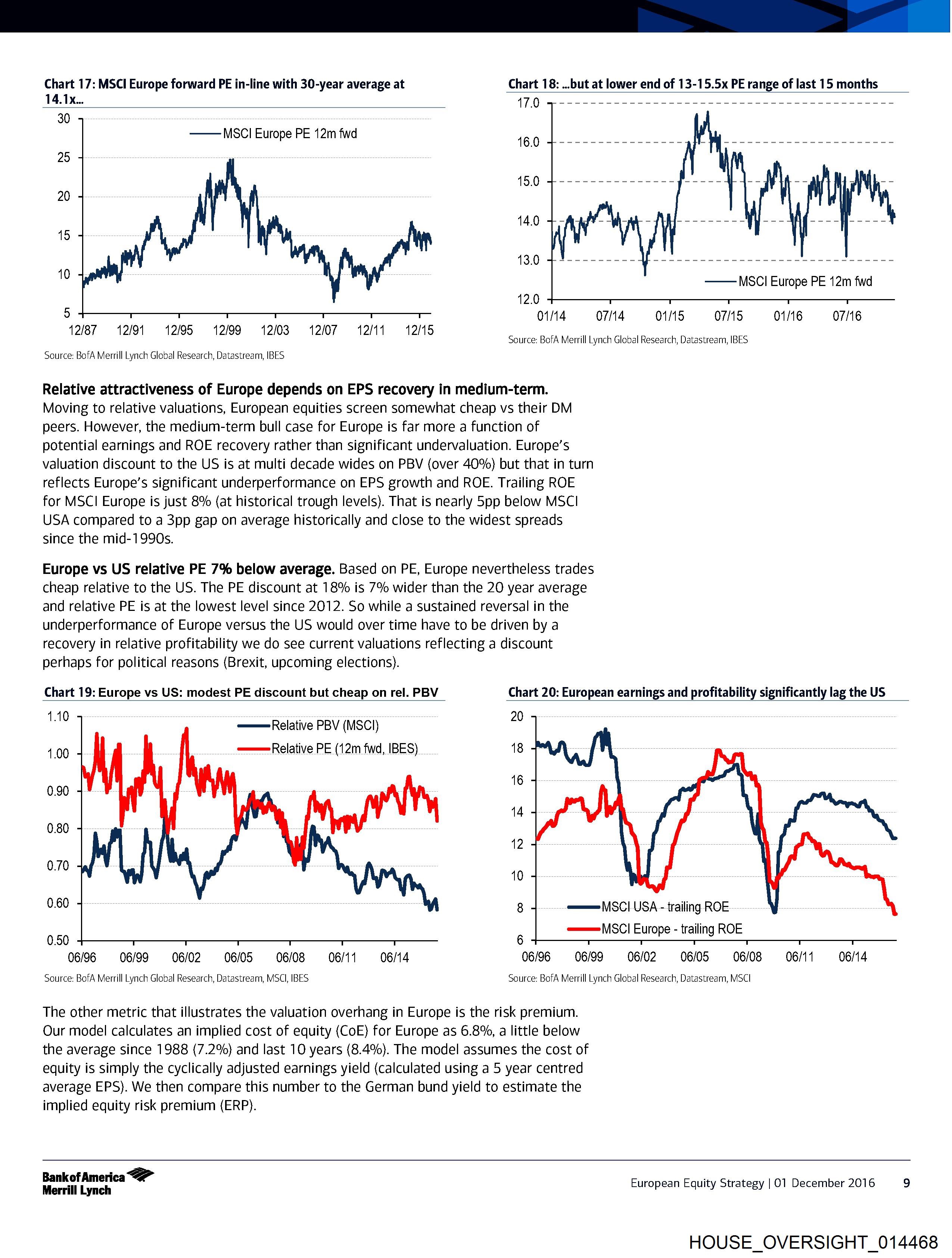

Chart 17: MSCI Europe forward PE in-line with 30-year average at

Chart 18: ...but at lower end of 13-15.5x PE range of last 15 months

14.1x... 17.0

30

——MSClI Europe PE 12m fwd 16.0

25

15.0

20

14.0

15

13.0

10 —MSCl Europe PE 12m fwd

12.0

) O14 = O74 OMS SCOTS SCOOT

12/87 12/91 12/95 9612/99 912/03 12/07 12/11 12/15 ;

Source: BofA Merrill Lynch Global Research, Datastream, IBES

Source: BofA Merrill Lynch Global Research, Datastream, IBES

Relative attractiveness of Europe depends on EPS recovery in medium-term.

Moving to relative valuations, European equities screen somewhat cheap vs their DM

peers. However, the medium-term bull case for Europe is far more a function of

potential earnings and ROE recovery rather than significant undervaluation. Europe’s

valuation discount to the US is at multi decade wides on PBV (over 40%) but that in turn

reflects Europe’s significant underperformance on EPS growth and ROE. Trailing ROE

for MSCI Europe is just 8% (at historical trough levels). That is nearly 5pp below MSCI

USA compared to a 3pp gap on average historically and close to the widest spreads

since the mid-1990s.

Europe vs US relative PE 7% below average. Based on PE, Europe nevertheless trades

cheap relative to the US. The PE discount at 18% is 7% wider than the 20 year average

and relative PE is at the lowest level since 2012. So while a sustained reversal in the

underperformance of Europe versus the US would over time have to be driven by a

recovery in relative profitability we do see current valuations reflecting a discount

perhaps for political reasons (Brexit, upcoming elections).

Chart 19: Europe vs US: modest PE discount but cheap on rel. PBV

1.10

Chart 20: European earnings and profitability significantly lag the US

——Relative PBV (MSCl)

——Relative PE (12m fwd, IBES)

1.00

0.90

0.80

0.70

0.60

=——=MSCI USA - trailing ROE

=———=|MSCI Europe - trailing ROE

0.50

06/6 = 06/99.——«<OG/O2—s«OG/OS.s«OG/OS = (OG/11 (06/14 06/96 «= 06/99—sC«OG/O2—sCOGNS—isi«G/OSCG 11 S(O 14

Source: BofA Merrill Lynch Global Research, Datastream, MSCI, IBES Source: BofA Merrill Lynch Global Research, Datastream, MSCI

The other metric that illustrates the valuation overhang in Europe is the risk premium.

Our model calculates an implied cost of equity (CoE) for Europe as 6.8%, a little below

the average since 1988 (7.2%) and last 10 years (8.4%). The model assumes the cost of

equity is simply the cyclically adjusted earnings yield (calculated using a 5 year centred

average EPS). We then compare this number to the German bund yield to estimate the

implied equity risk premium (ERP).

Bankof America

Merrill Lynch European Equity Strategy | O01 December 2016 9

HOUSE_OVERSIGHT_014468

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014468.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 2,718 characters |

| Indexed | 2026-02-04T16:22:36.696197 |