HOUSE_OVERSIGHT_014473.jpg

{kind=link}

Extracted Text (OCR)

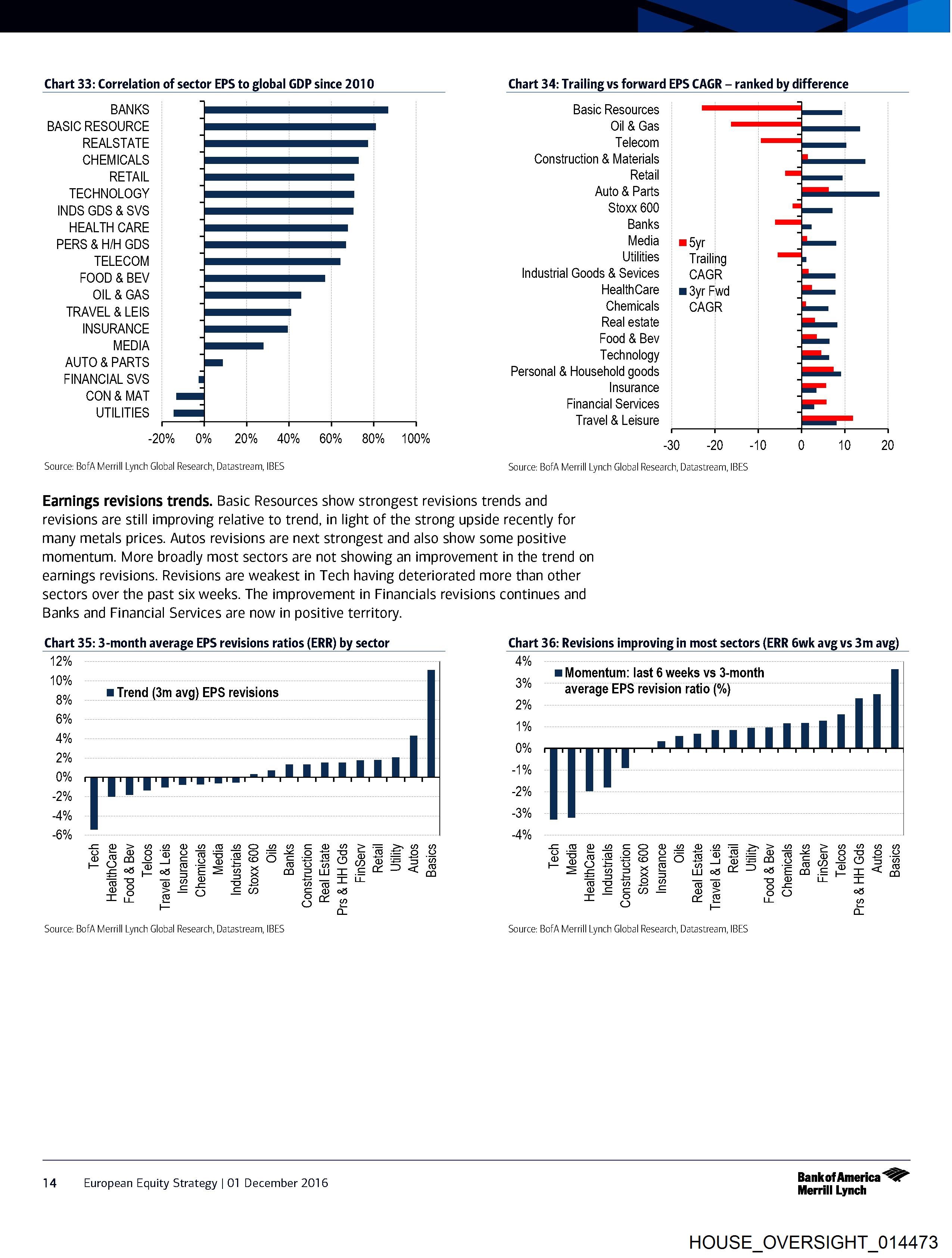

Chart 33: Correlation of sector EPS to global GDP since 2010 Chart 34: Trailing vs forward EPS CAGR - ranked by difference

BANKS Basic Resources

BASIC RESOURCE Oil & Gas

REALSTATE Telecom

CHEMICALS Construction & Materials

RETAIL Retail

TECHNOLOGY Auto & Parts

INDS GDS & SVS Stoxx 600

HEALTH CARE Banks

PERS & H/H GDS Media = m5yr |

TELECOM Utilities Trailing

FOOD & BEV Industrial Goods & Sevices CAGR

OIL & GAS HealthCare — m 3yr Fwd

TRAVEL & LEIS Chemicals CAGR

INSURANCE Real estate

MEDIA Food & Bev

Technology

AUTO & PARTS Personal & Household goods

FINANCIAL SVS (nerarerriea

GEN MAL Financial Services

UTILITIES Travel & Leisure

-20% 0% 20% 40% 60% 80% 100% 30 20 40 0 40 20

Source: BofA Merrill Lynch Global Research, Datastream, IBES Source: BofA Merrill Lynch Global Research, Datastream, IBES

Earnings revisions trends. Basic Resources show strongest revisions trends and

revisions are still improving relative to trend, in light of the strong upside recently for

many metals prices. Autos revisions are next strongest and also show some positive

momentum. More broadly most sectors are not showing an improvement in the trend on

earnings revisions. Revisions are weakest in Tech having deteriorated more than other

sectors over the past six weeks. The improvement in Financials revisions continues and

Banks and Financial Services are now in positive territory.

Chart 35: 3-month average EPS revisions ratios (ERR) by sector Chart 36: Revisions improving in most sectors (ERR 6wk avg vs 3m avg)

12% 4%

m= Momentum: last 6 weeks vs 3-month

10% 3% a sae

& Trend (3m avg) EPS revisions average EPS revision ratio (%)

)

Bi 2%

6%

1%

4% ;

2% O%

‘0

-1%

0% °

99

2% 2th

-A% 3%

6% 4%

SEOFRANAMADADAHE HDA FZTPE*”A RK SEREMOHR COMA HA HM H=~a SPFHHFHMAA”R

Gof ® 6 ° SO=zr~s~ onus SH’ so oO oO = Soot Sf ® ee on 6 Oo

PSagir gs Bessy sO$ sess PBSLSS ESCORT SSASESSSER

SePfsa SSS Se mastirer Ag SPEGSES Oot -weme Prt s

eB p22 38 G@aertt esreaS2 a8 epee * =

® 8 re) En SO es ®9EeEecVnE o> 85 oS

Iie © & Cw = & [ae rm oO

E 2 E 2

oO oO

Source: BofA Merrill Lynch Global Research, Datastream, IBES Source: BofA Merrill Lynch Global Research, Datastream, IBES

5: Bankot America

14 European Equity Strate: 01 December 2016 i

P quity By | Merrill Lynch

HOUSE_OVERSIGHT_014473

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014473.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 2,274 characters |

| Indexed | 2026-02-04T16:22:37.273178 |