HOUSE_OVERSIGHT_014529.jpg

{kind=link}

Extracted Text (OCR)

positive sentiment are the foundation for continued gains in the equity markets and an investor

rotation from overexposure to long-dated fixed income into under owned equities.

This rotation will need a few periods of confirmation, given the still uncertain broader global macro

outlook, but we expect price-to-earnings multiples to remain elevated, despite higher rates,

throughout the year. S&P 500 earnings have a wide range of forecasts due to the potential for

sizable tax cuts in 2017. Based on this, the S&P 500 could add extra earnings on top of normalized

growth, which is expected to be around 9%. At present, a reasonable range, albeit a wide one, is

considered to be between $129 and $138 with the potential for further upside. In this scenario,

where we get pro-growth policies filtering into a higher earnings number, an S&P 500 bull case

level of 2700 at the high end is possible.

Improving profits and growth should take equities higher

For now, a base case utilizing the five factor framework from BofA Merrill Lynch Global

Research, which combines sentiment, valuation and technical, equates to 2300 for the S&P 500 at

year end. The two components that include long-term valuation and 12-month price momentum are

indicating that S&P 500 levels between the base and bull case are increasing in probability. Of

course, there are a number of scenarios that could unfold that would indicate a wide range of

outcomes depending on the multiple or earnings number that ultimately develops. In the end, it all

comes down to the path of corporate profits and the visibility on growth, both of which are

improving.

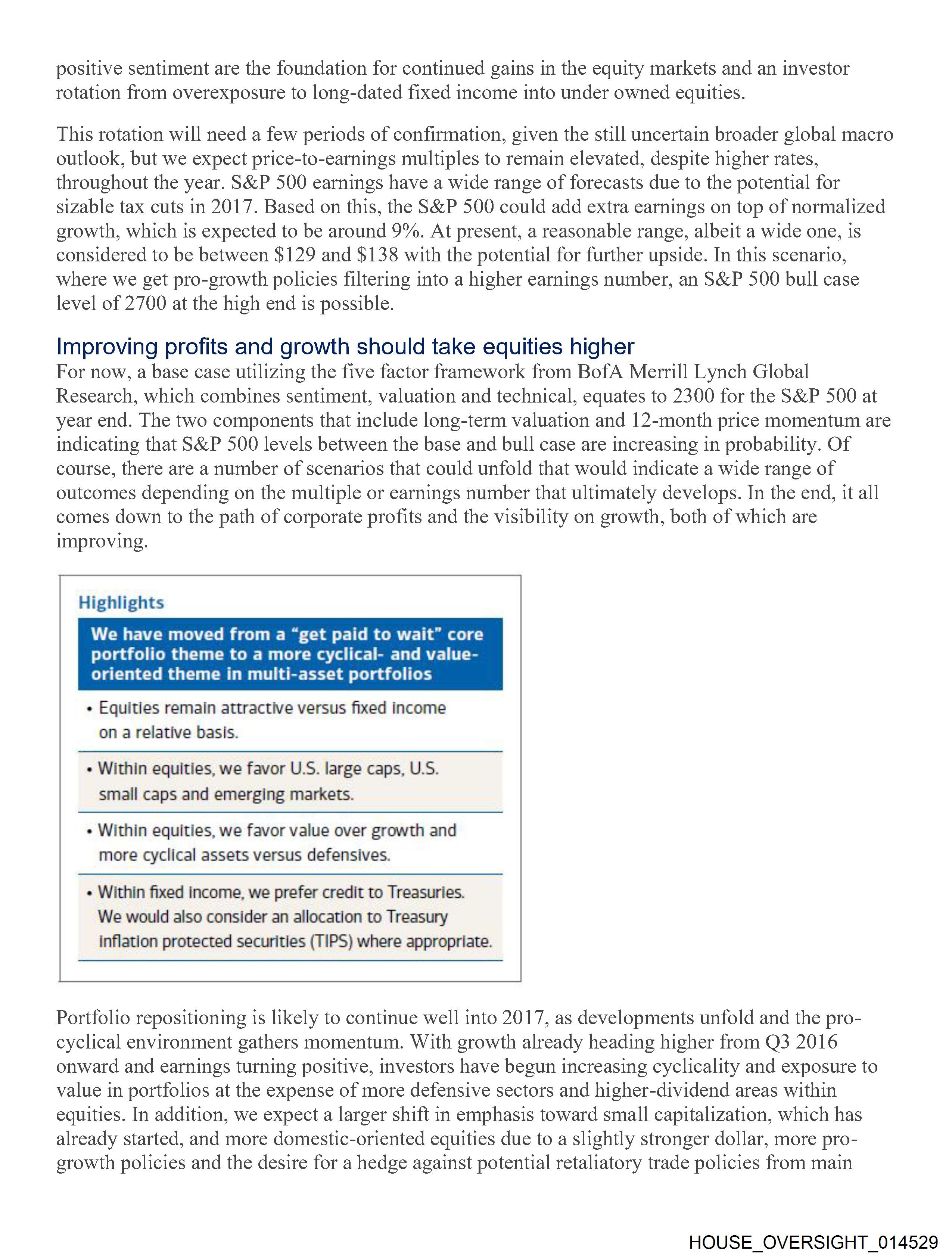

Highlights

We have moved from a “get paid to wait” core

portfolio theme to a more cyclical- and value-

oriented theme in multi-asset portfolios

¢ Equities remain attractive versus fixed income

on a relative basis.

« Within equities, we favor U.S. large caps, U.S.

small caps and emerging markets.

« Within equities, we favor value over growth and

more cyclical assets versus defensives.

« Within fixed income, we prefer credit to Treasuries.

We would also consider an allocation to Treasury

inflation protected securities (TIPS) where appropriate.

Portfolio repositioning is likely to continue well into 2017, as developments unfold and the pro-

cyclical environment gathers momentum. With growth already heading higher from Q3 2016

onward and earnings turning positive, investors have begun increasing cyclicality and exposure to

value in portfolios at the expense of more defensive sectors and higher-dividend areas within

equities. In addition, we expect a larger shift in emphasis toward small capitalization, which has

already started, and more domestic-oriented equities due to a slightly stronger dollar, more pro-

growth policies and the desire for a hedge against potential retaliatory trade policies from main

HOUSE_OVERSIGHT_014529

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014529.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 2,878 characters |

| Indexed | 2026-02-04T16:22:49.670553 |

Related Documents

Documents connected by shared names, same document type, or nearby in the archive.