HOUSE_OVERSIGHT_014767.jpg

{kind=link}

Extracted Text (OCR)

Characterizing carry

Efficient carry strategies involve buying and selling dynamic portfolios of currencies

with certain risk characteristics. Carry strategies are supposed to work better over long

investment horizons, so that the cushion provided by the carry compensates for the

currency volatility through mean reversion.

Here, we analyze carry from a different perspective, as our goal is to identify standalone

attractive carry opportunities. We define the investment horizon to end 1Q17. We sort

currencies based on risk-adjusted carry. We then characterize the factor exposure of

currency returns, isolating global and idiosyncratic sources of risks, in order to identify

smart carry trades that are not highly exposed to a massive re-pricing of global factors,

such as US rates, USD, commodity prices and global risk aversion. We identify carry

trades that have low exposure to global factors, in particular the USD factor, and offer

attractive risk-rewards.

Not surprisingly, purely based on carry considerations, EM currencies appear more

attractive than DM ones, which are mostly candidates for funding currencies. However,

carry trades returns are highly volatile, exhibit negative skewness and fat tails. Even

controlling for different measures of risk such as volatility or maximum drawdown, and

according to this criteria only, we find that EM currencies are the most attractive, in

particular ARS, BRL in LatAm, RUB, TRY and ZAR in EEMEA and INR, IDR and CNY in

Asia (Chart 63).

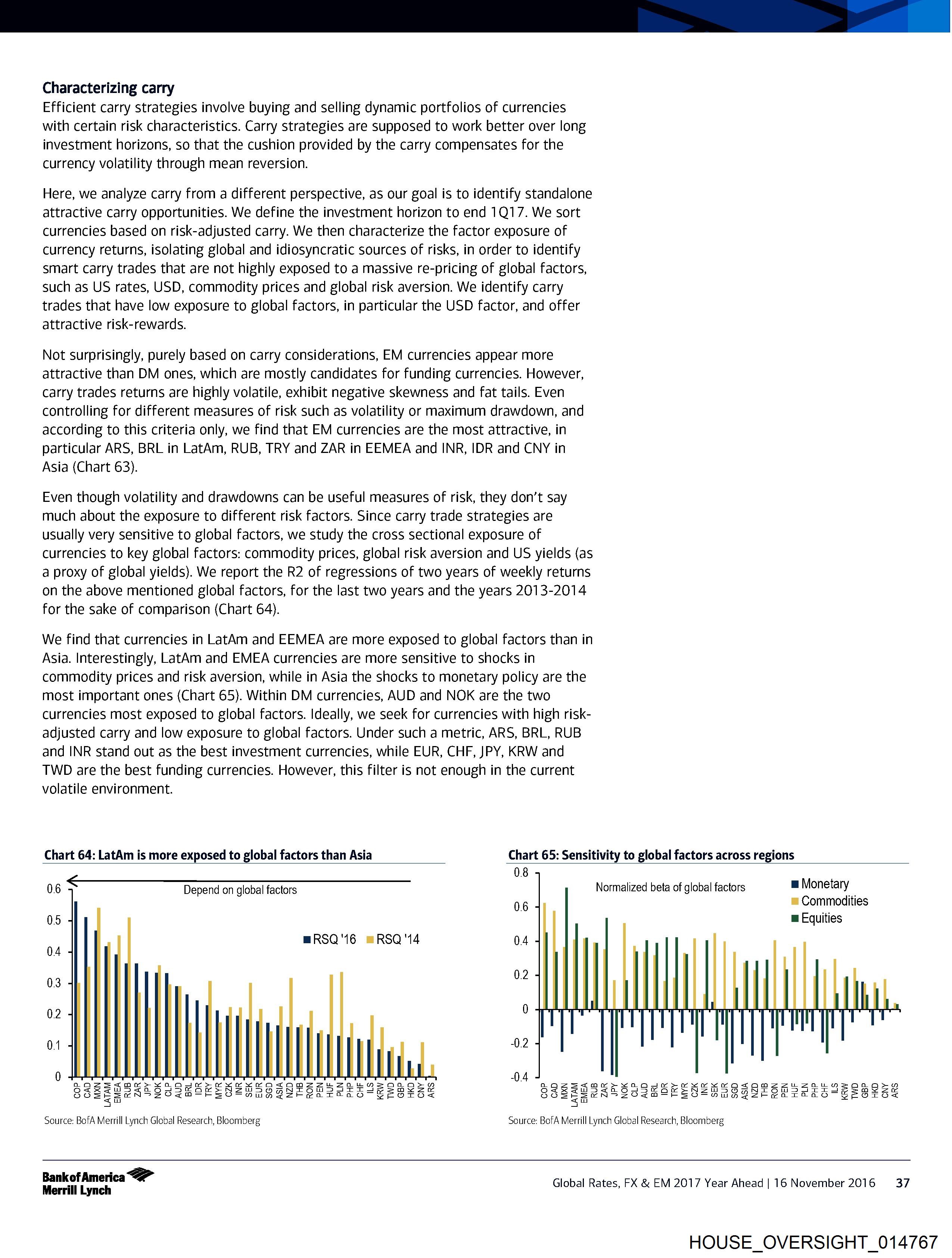

Even though volatility and drawdowns can be useful measures of risk, they don’t say

much about the exposure to different risk factors. Since carry trade strategies are

usually very sensitive to global factors, we study the cross sectional exposure of

currencies to key global factors: commodity prices, global risk aversion and US yields (as

a proxy of global yields}. We report the R2 of regressions of two years of weekly returns

on the above mentioned global factors, for the last two years and the years 2013-2014

for the sake of comparison (Chart 64).

We find that currencies in LatAm and EEMEA are more exposed to global factors than in

Asia. Interestingly, LatAm and EMEA currencies are more sensitive to shocks in

commodity prices and risk aversion, while in Asia the shocks to monetary policy are the

most important ones (Chart 65). Within DM currencies, AUD and NOK are the two

currencies most exposed to global factors. Ideally, we seek for currencies with high risk-

adjusted carry and low exposure to global factors. Under such a metric, ARS, BRL, RUB

and INR stand out as the best investment currencies, while EUR, CHF, JPY, KRW and

TWD are the best funding currencies. However, this filter is not enough in the current

volatile environment.

Chart 64: LatAm is more exposed to global factors than Asia Chart 65: Sensitivity to global factors across regions

08

nn 2

06 Depend on global factors Normalized beta of global factors m Monetary

06 = Commodities

05 mw Equities

mRSQ'6 @RSQ'14 04

04

03 0.2

02 0

01 -0.2

SSSESANS SO ZHOF SOSH AReSHRa reas“ EESTS = SSEEEZNS2O2H SF SSS GRG SSE RE PALS“ EEBTSS

Source: BofA Merrill Lynch Global Research, Bloomberg Source: BofA Merrill Lynch Global Research, Bloomberg

Bankof America Global Rates, FX & EM 2017 Year Ahead | 16 November 2016 37

Merrill Lynch

HOUSE_OVERSIGHT_014767

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014767.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,336 characters |

| Indexed | 2026-02-04T16:23:40.834141 |