HOUSE_OVERSIGHT_014876.jpg

{kind=link}

Extracted Text (OCR)

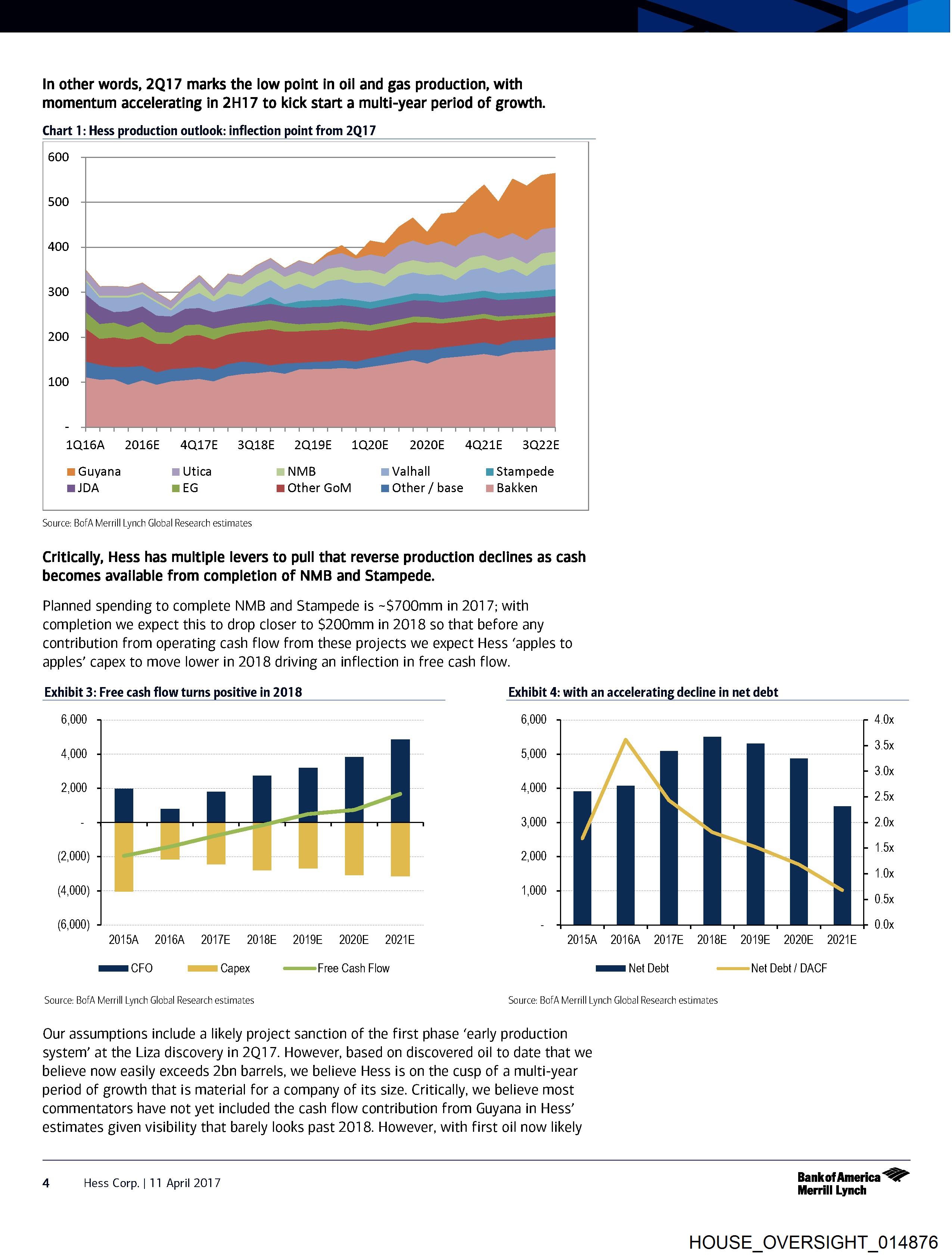

In other words, 2Q17 marks the low point in oil and gas production, with

momentum accelerating in 2H17 to kick start a multi-year period of growth.

Chart 1: Hess production outlook: inflection point from 2Q17

600

500

400

300

200

100

1Q16A 2016 4Q17E 3Q18E 2Q19F 1Q20E 2020E 4Q21E 3Q22E

m Guyana m Utica m= NMB Valhall m Stampede

gJDA mEG m Other GoM mOther/base mBakken

Source: BofA Merrill Lynch Global Research estimates

Critically, Hess has multiple levers to pull that reverse production declines as cash

becomes available from completion of NMB and Stampede.

Planned spending to complete NMB and Stampede is ~$700mm in 2017; with

completion we expect this to drop closer to $200mm in 2018 so that before any

contribution from operating cash flow from these projects we expect Hess ‘apples to

apples’ capex to move lower in 2018 driving an inflection in free cash flow.

Exhibit 3: Free cash flow turns positive in 2018 Exhibit 4: with an accelerating decline in net debt

4,000 5,000 3.x

3.0x

2,000 4,000 2.5x

3,000 2.0x

1.0x

(4,000) 1,000 0.5x

2015A 2016A =2017E = 2018E 2019E 2020E 2021E 2015A 2016A 2017E 2018E 2019E 2020E 2021E

me CFO lt Capex o===Free Cash Flow mas Net Debt == Net Debt / DACF

Source: BofA Merrill Lynch Global Research estimates Source: BofA Merrill Lynch Global Research estimates

Our assumptions include a likely project sanction of the first phase ‘early production

system’ at the Liza discovery in 2Q17. However, based on discovered oil to date that we

believe now easily exceeds 2bn barrels, we believe Hess is on the cusp of a multi-year

period of growth that is material for a company of its size. Critically, we believe most

commentators have not yet included the cash flow contribution from Guyana in Hess’

estimates given visibility that barely looks past 2018. However, with first oil now likely

4 Hess Corp.| 11 April 2017 Bankof America “>

Merrill Lynch

HOUSE_OVERSIGHT_014876

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014876.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 1,932 characters |

| Indexed | 2026-02-04T16:23:57.408689 |