HOUSE_OVERSIGHT_014927.jpg

{kind=link}

Extracted Text (OCR)

Wayfair (Neutral, $44 PO)

Stock view: Timeline on profitability still an issue, but comps ease in 2Q’17

Wayfair’s two issues have been deceleration in U.S. revenue growth and negative

operating margins as the company continues to aggressively invest in logistics,

international expansion, marketing, and new categories. 1Q customer and order growth

comps remain tough, which was one of the drivers of revenue growth guidance below

expectations. Wayfair also attributed weak guidance to caution on the retail

environment and added investment. Growth comps ease in 2Q/3Q, and there is potential

for more stable growth in 2Q guidance to drive improving investor sentiment.

As for margins, management guided to EBITDA margin of (3.5%)-(3.8%), a deceleration

from (2.8%) in 1Q’16 due to a lower opex absorption in the quarter on seasonally lower

sales. The US is expected to swing back to EBITDA losses in 1Q’17, while Intl losses are

expected to remain steady. We forecast EBITDA margin of (2.4%}, with (0.2%) EBITDA

margin in the US and (19.0%) margin in International. The company continues to expect

little to no ad spend leverage given increase International ad spend.

Management historically builds conservativism into its guidance and, until last year, had

a track record of beating the upper end of its sales outlook by ~10%. Recently, revenue

has been by a low-single digit percentage. Our above consensus 1Q revenue forecast

implies 1% upside to the high end of the guidance range, in line with the trend over the

past 3 quarters. We think investors expect sales growth above the guidance range as

well.

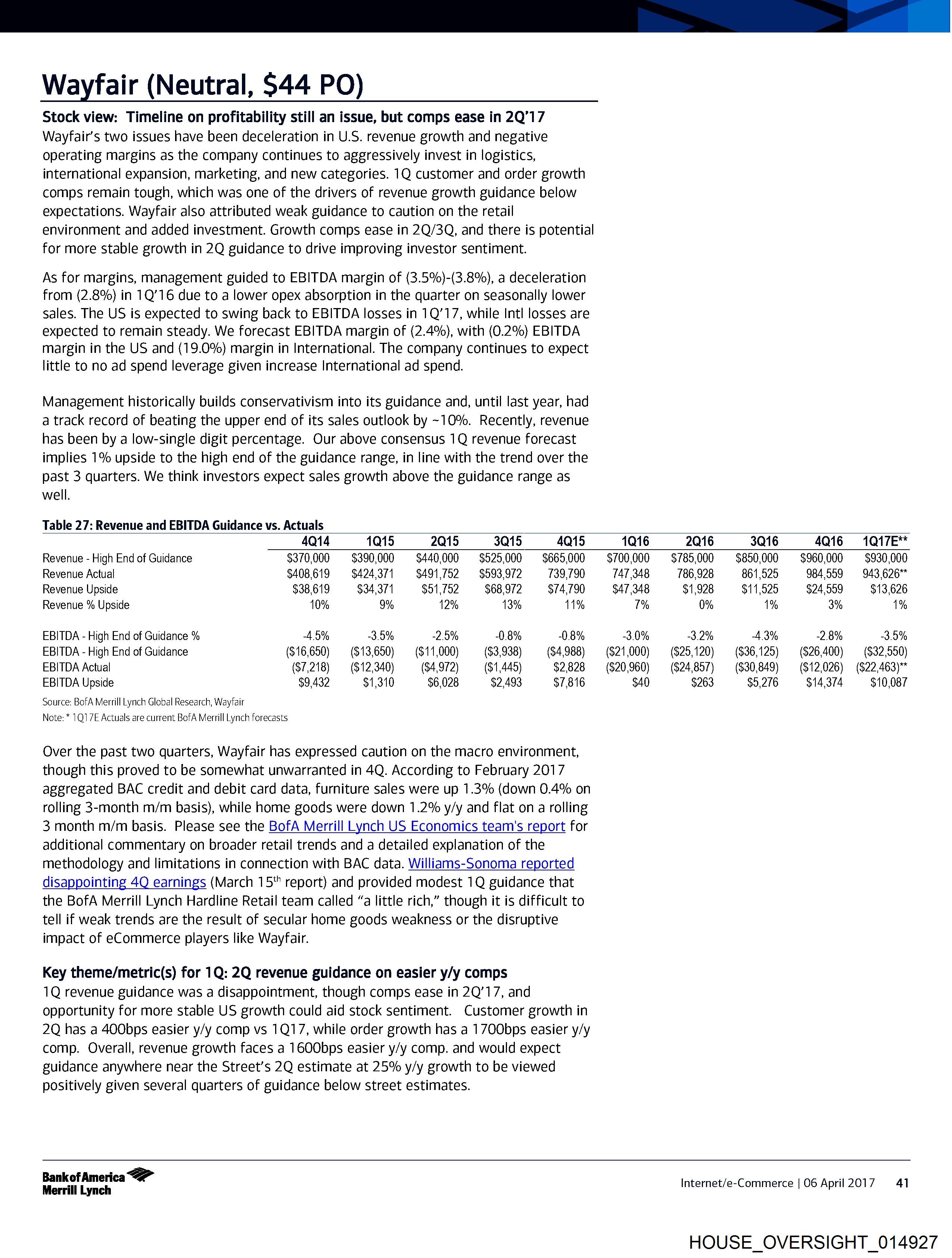

Table 27: Revenue and EBITDA Guidance vs. Actuals

4Q14 1015 2Q15 3Q15 4Q15 1Q16 2016 3Q16 4Q16 1Q17E**

Revenue - High End of Guidance $370,000 $390,000 $440,000 $525,000 $665,000 $700,000 $785,000 $850,000 $960,000 $930,000

Revenue Actual $408,619 $424.371 $491,752 $593,972 739,790 147 348 786,928 861,525 984,559 943.626"

Revenue Upside $38,619 $34,371 $51,752 $68,972 $74,790 $47 348 $1,928 $11,525 $24,559 $13,626

Revenue % Upside 10% 9% 12% 13% 11% 1% 0% 1% 3% 1%

EBITDA - High End of Guidance % 45% -3.5% -2.5% -0.8% -0.8% -3.0% -3.2% 43% -2.8% -3.5%

EBITDA - High End of Guidance ($16,650) ($13,650) ~~ ($11,000) ($3,938) ($4,988) ($21,000) = ($25,120) ($36,125) ($26,400) ($32,550)

EBITDA Actual ($7,218) — ($12,340) ($4,972) (51,445) $2,828 ($20,960) ($24,857) ($80,849) = ($12,026) ($22,463)*

EBITDA Upside $9,432 $1,310 $6,028 $2,493 $7,816 $40 $263 $5,276 $14,374 $10,087

Source: BofA Merrill Lynch Global Research, Wayfair

Note: * 1Q17E Actuals are current BofA Merrill Lynch forecasts

Over the past two quarters, Wayfair has expressed caution on the macro environment,

though this proved to be somewhat unwarranted in 4Q. According to February 2017

aggregated BAC credit and debit card data, furniture sales were up 1.3% (down 0.4% on

rolling 3-month m/m basis), while home goods were down 1.2% y/y and flat on a rolling

3 month m/m basis. Please see the BofA Merrill Lynch US Economics team's report for

additional commentary on broader retail trends and a detailed explanation of the

methodology and limitations in connection with BAC data. Williams-Sonoma reported

disappointing 40 earnings (March 15* report) and provided modest 1Q guidance that

the BofA Merrill Lynch Hardline Retail team called “a little rich,” though it is difficult to

tell if weak trends are the result of secular home goods weakness or the disruptive

impact of eCommerce players like Wayfair.

Key theme/metric(s) for 1Q: 2Q revenue guidance on easier y/y comps

1Q revenue guidance was a disappointment, though comps ease in 2Q’17, and

opportunity for more stable US growth could aid stock sentiment. Customer growth in

2Q has a 400bps easier y/y comp vs 1Q17, while order growth has a 1700bps easier y/y

comp. Overall, revenue growth faces a 1600bps easier y/y comp. and would expect

guidance anywhere near the Street’s 2Q estimate at 25% y/y growth to be viewed

positively given several quarters of guidance below street estimates.

Bankof America

Merrill Lynch Internet/e-Commerce | 06 April2017 41

HOUSE_OVERSIGHT_014927

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014927.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 4,136 characters |

| Indexed | 2026-02-04T16:24:10.300079 |