HOUSE_OVERSIGHT_014973.jpg

{kind=link}

Extracted Text (OCR)

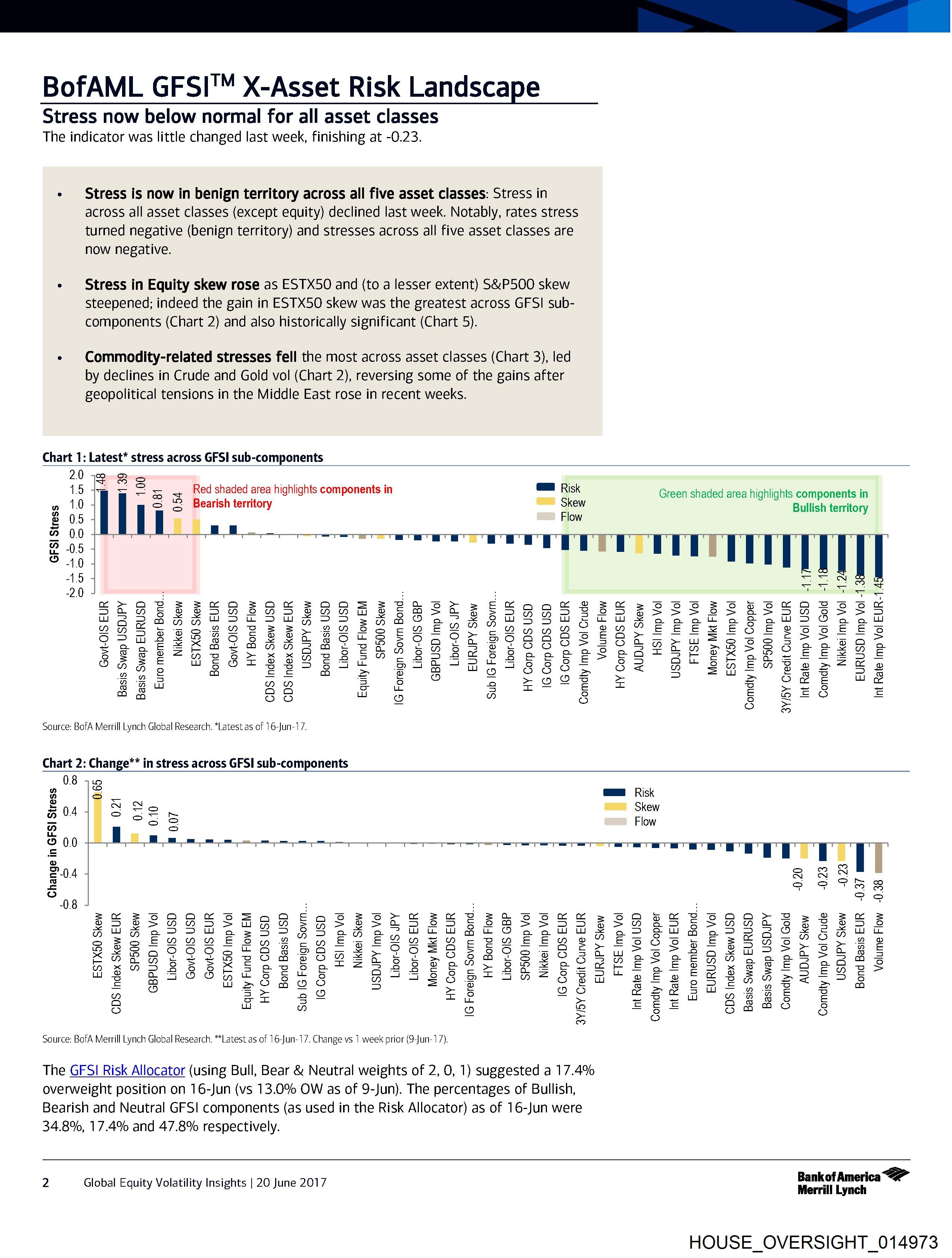

BofAML GFSI™ X-Asset Risk Landscape

Stress now below normal for all asset classes

The indicator was little changed last week, finishing at -0.23.

¢ Stress is now in benign territory across all five asset classes: Stress in

across all asset classes (except equity) declined last week. Notably, rates stress

turned negative (benign territory) and stresses across all five asset classes are

now negative.

« Stress in Equity skew rose as ESTX50 and (to a lesser extent) S&P500 skew

steepened; indeed the gain in ESTX50 skew was the greatest across GFSI sub-

components (Chart 2) and also historically significant (Chart 5).

¢ Commodity-related stresses fell the most across asset classes (Chart 3), led

by declines in Crude and Gold vol (Chart 2}, reversing some of the gains after

geopolitical tensions in the Middle East rose in recent weeks.

Chart 1: Latest* stress across GFSI sub-components

2.0 12 Bo

15 me a == y Red shaded area highlights components in GS Risk Green shaded area highlights components in

» 1.0 so © Bearish territory “—* Skew Bullish territory

& 05 Flow

a 00 -

2 05

© 410

-1.5 4 mS es cs

erarg “ea ae aa BDaoor Ew ec ® ia oi rate npe

SEO SEES DEBS EBSBRSEEHSHE EES SSS SSS ESSSSEsResesHssss

UMeapawnntrbebouZFrrAszsnamaPaea GPRS GZtrSDSUSFtUSse oat easawrFso ou

ARS exp sSYREERS OHESERELL EPH FHRLPRPEEEXPESELSESEES

C2 eee BOS See BSCE S SCALE SORES SESE ZY wWZS8SES5 zzz aS

tae g eEtZtRaO#tDTHHVNA2eOLVARBGtinsae ft OO Rat SPaAa nH BF HSBPSSE 2 eSLFR Ba

6€ ae tH soe>xxAwvsBSEG” B S8@t& 682 an 822 eqatitsF ox ite) EEX Ee

8s e2eE OeezGEELRZL:2 ce S2@PFtP5 242 E25 € F 55 aust eozt-=szg-

CAG uweo caportrtoat aia 78 8ogs oma 2) 2nE”n 3 2 BS se

a 2 co £E co 2 2 © ane > 5 =u Fos - 3

Bas = 4 = > oO = os Ore Ww

es @w Ze fom 2 2 oa e <= = >= 8 =

oD

Source: BofA Merrill Lynch Global Research. *Latest as of 16-Jun-17.

Chart 2: Change** in stress across GFSI sub-components

0.8 y19 .

2 4 Gas Risk

o ~N N

B04 ss =e ~ “> Skew

= oe Flow

“td fo)

© 00 ™T a ee ee a a ee os se ee ae ee ee os i

re rrvTTTTT

ine]

P04 gaan

= oe FR Ss

(s) S656

08 ; ; ;

ia saaks a =e i) ore eso asnonoee ease Psoeaogar?rs ® [a4

BS ESBBSSHBABESS ESE, ESS eGE SSS SEER RES ELSSRESBESSESS

Au AFeaer- Messer -FZ<SeHFf eSGfteusat_ COeaeatosear- Frage er rpg ZS5GHUE

SESEHHHRESHPSEHREZFELZLVEREPMEERGLESSSERZSERS RSLS eB

22S8n900 Cet a gana Ss, P0OfRG B80 e 7, SBS uz aozen La -F=egesagsg

Hern LE #te#eeoEovOmM DORMXEA 5 Le Satis 2 Onadane2z#se2E6EQ97MN Ql 25 ans

AxGHDSSSKSeavsetrtzAnassgsee®s SPxBerTrerERgEsSS xe FSEaeRsu

mus "rr f#38 8h er Ss §t 5 AASSS8SEtTIAGZSZRAt* eEetEXe Ss eER2=EBE

f= a mpomAao 5 = ‘p £ Sea see De? ans >” «a

g © 22 290 = 2 a SeeCua"e2e¢es5 =F

a om ral ral ao 8

O uw a 2) ee £Ee ga ao 8

1S) > 8

foe]

Source: BofA Merrill Lynch Global Research. **Latest as of 16-Jun-17. Change vs 1 week prior (9-Jun-17).

The GFSI Risk Allocator (using Bull, Bear & Neutral weights of 2, 0, 1} suggested a 17.4%

overweight position on 16-Jun (vs 13.0% OW as of 9-Jun}. The percentages of Bullish,

Bearish and Neutral GFSI components (as used in the Risk Allocator) as of 16-Jun were

34.8%, 17.4% and 47.8% respectively.

Z Global Equity Volatility Insights | 20 June 2017 oat a

HOUSE_OVERSIGHT_014973

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014973.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,201 characters |

| Indexed | 2026-02-04T16:24:22.629241 |