HOUSE_OVERSIGHT_016121.jpg

{kind=link}

Extracted Text (OCR)

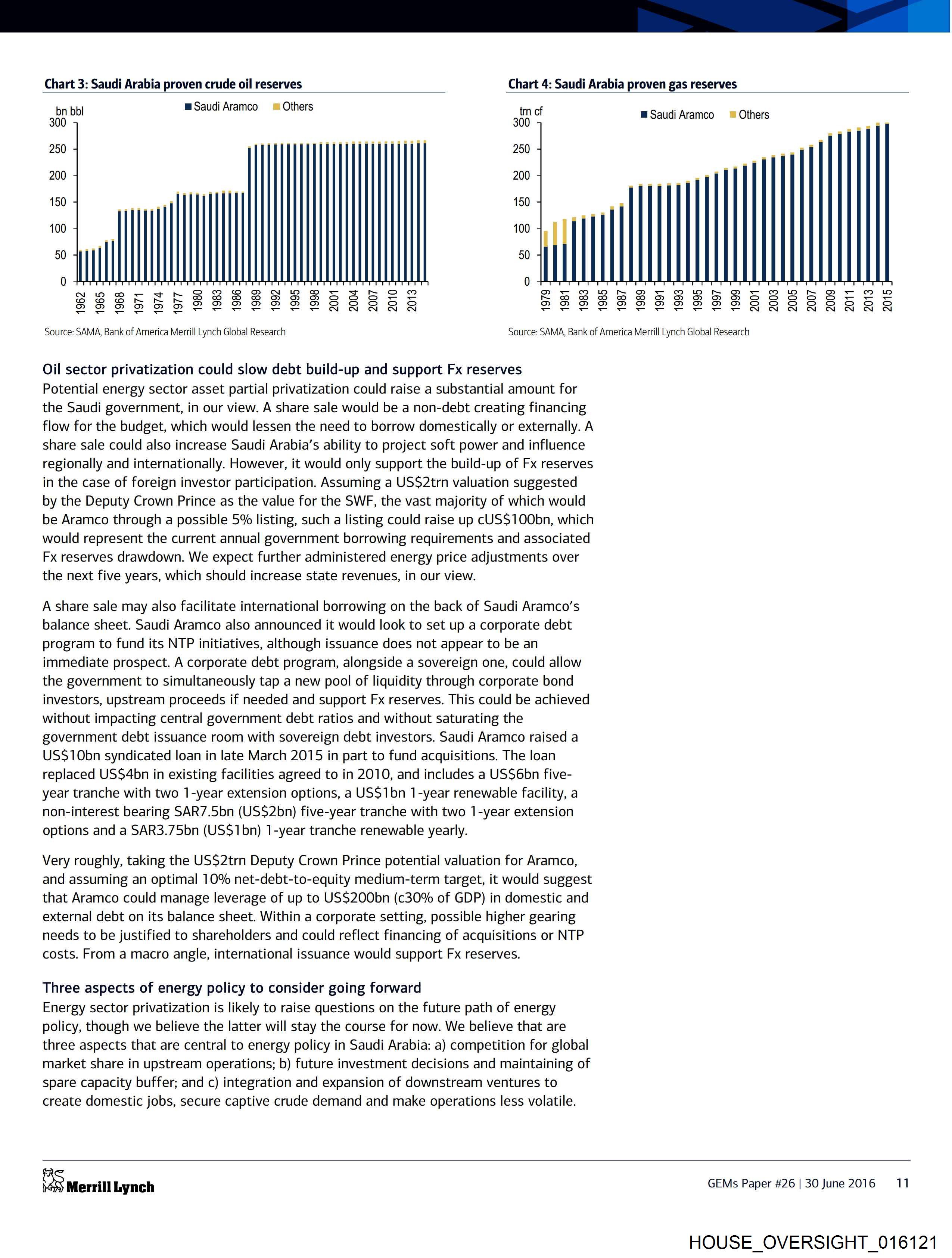

Chart 3: Saudi Arabia proven crude oil reserves Chart 4: Saudi Arabia proven gas reserves

bribbi mSaudi Aramco = Others tn cf eSandidvenos withers

0 300 unt

250 mn 250

200 200

150 | Tl 150

100 100 +

50 50

N wore wastr re @GOMeWweoenwonorwyFtrtrseo om ao" oe @See OwnTr Oey OMWMse B= o wD

ooonrenrenrewewewernwvoodooo ono eo rt ~YTiowdonwdoenaonoooomoodononoecoddcaoeoeog4r r=

DODD AaD&OOOWDDPDSe SSS FS DMPODWDDADWWADHA DOGG FSG So fo GS

+ BS BS v ied BS bs NNN NN ba 7 x x v e v ied v = + NNNNN NN N

a a

Source: SAMA, Bank of America Merrill Lynch Global Research Source: SAMA, Bank of America Merrill Lynch Global Research

Oil sector privatization could slow debt build-up and support Fx reserves

Potential energy sector asset partial privatization could raise a substantial amount for

the Saudi government, in our view. A share sale would be a non-debt creating financing

flow for the budget, which would lessen the need to borrow domestically or externally. A

share sale could also increase Saudi Arabia’s ability to project soft power and influence

regionally and internationally. However, it would only support the build-up of Fx reserves

in the case of foreign investor participation. Assuming a USS2trn valuation suggested

by the Deputy Crown Prince as the value for the SWF, the vast majority of which would

be Aramco through a possible 5% listing, such a listing could raise up CUS$100bn, which

would represent the current annual government borrowing requirements and associated

Fx reserves drawdown. We expect further administered energy price adjustments over

the next five years, which should increase state revenues, in our view.

A share sale may also facilitate international borrowing on the back of Saudi Aramco’s

balance sheet. Saudi Aramco also announced it would look to set up a corporate debt

program to fund its NTP initiatives, although issuance does not appear to be an

immediate prospect. A corporate debt program, alongside a sovereign one, could allow

the government to simultaneously tap a new pool of liquidity through corporate bond

investors, upstream proceeds if needed and support Fx reserves. This could be achieved

without impacting central government debt ratios and without saturating the

government debt issuance room with sovereign debt investors. Saudi Aramco raised a

US$10bn syndicated loan in late March 2015 in part to fund acquisitions. The loan

replaced USS4bn in existing facilities agreed to in 2010, and includes a USS6bn five-

year tranche with two 1-year extension options, a US$1bn 1-year renewable facility, a

non-interest bearing SAR7.5bn (USS2bn) five-year tranche with two 1-year extension

options and a SAR3.75bn (US$1bn) 1-year tranche renewable yearly.

Very roughly, taking the US$2trn Deputy Crown Prince potential valuation for Aramco,

and assuming an optimal 10% net-debt-to-equity medium-term target, it would suggest

that Aramco could manage leverage of up to US$200bn (c30% of GDP) in domestic and

external debt on its balance sheet. Within a corporate setting, possible higher gearing

needs to be justified to shareholders and could reflect financing of acquisitions or NTP

costs. From a macro angle, international issuance would support Fx reserves.

Three aspects of energy policy to consider going forward

Energy sector privatization is likely to raise questions on the future path of energy

policy, though we believe the latter will stay the course for now. We believe that are

three aspects that are central to energy policy in Saudi Arabia: a) competition for global

market share in upstream operations; b) future investment decisions and maintaining of

spare capacity buffer; and c) integration and expansion of downstream ventures to

create domestic jobs, secure captive crude demand and make operations less volatile.

OS merrill Lynch GEMs Paper #26 |30June2016 11

HOUSE_OVERSIGHT_016121

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_016121.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,873 characters |

| Indexed | 2026-02-04T16:27:02.355553 |