HOUSE_OVERSIGHT_021046.jpg

{kind=link}

Extracted Text (OCR)

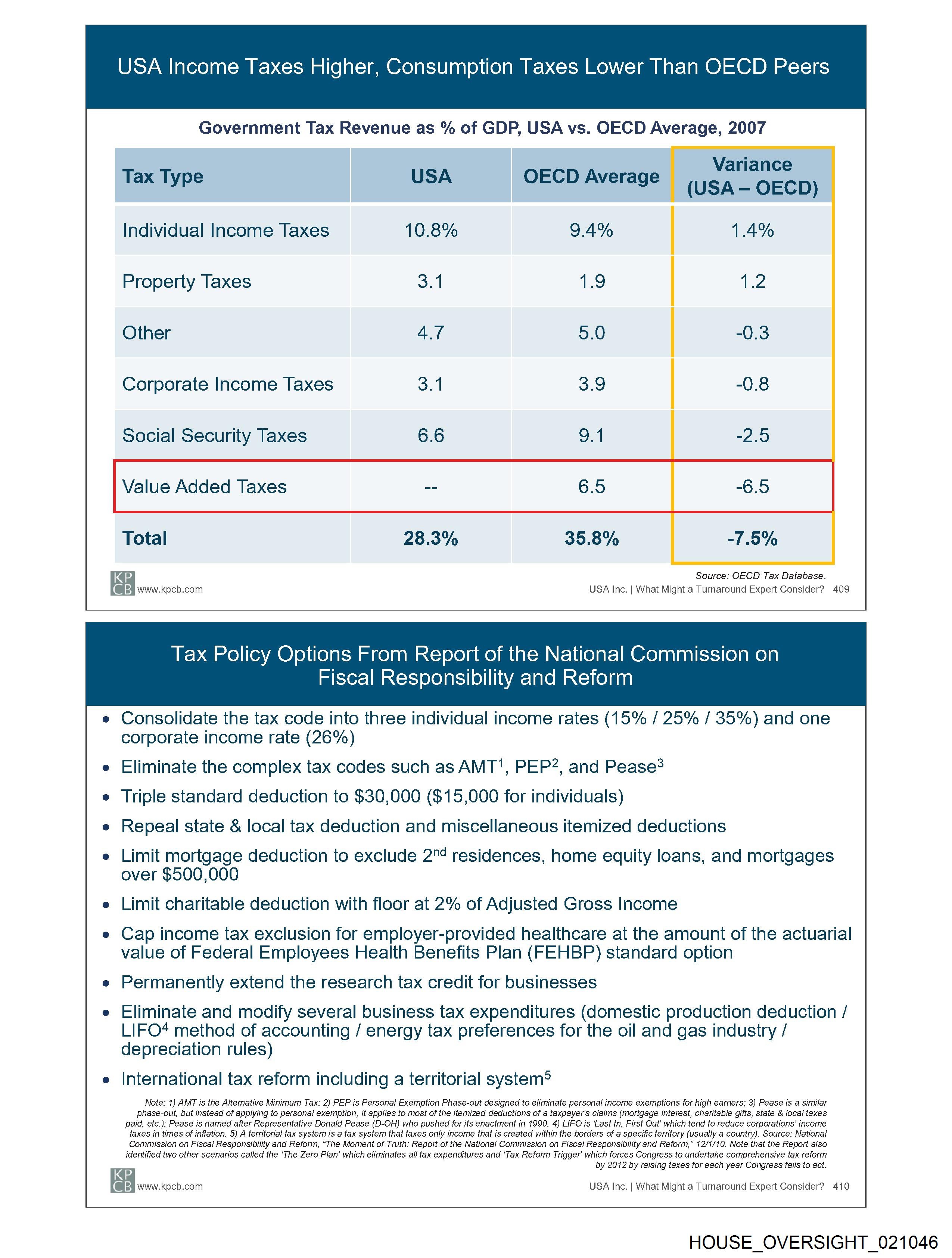

USA Income Taxes Higher, Consumption Taxes Lower Than OECD Peers

Government Tax Revenue as % of GDP, USA vs. OECD Average, 2007

Variance

Tax Type USA OECD Average (USA — OECD)

Individual Income Taxes 10.8% 9.4% 1.4%

Property Taxes a1 1.9 1.2

Other 4.7 5.0

Corporate Income Taxes 3.1 oo

Social Security Taxes

Value Added Taxes

Total

KP Source: OECD Tax Database.

(@ 4 www.kpcb.com USA Inc. | What Might a Turnaround Expert Consider? 409

Tax Policy Options From Report of the National Commission on

Fiscal Responsibility and Reform

e Consolidate the tax code into three individual income rates (15% / 25% / 35%) and one

corporate income rate (26%)

e Eliminate the complex tax codes such as AMT', PEP2, and Pease?

e Triple standard deduction to $30,000 ($15,000 for individuals)

e Repeal state & local tax deduction and miscellaneous itemized deductions

e Limit mortgage deduction to exclude 2™ residences, home equity loans, and mortgages

over $500,000

e Limit charitable deduction with floor at 2% of Adjusted Gross Income

e Cap income tax exclusion for employer-provided healthcare at the amount of the actuarial

value of Federal Employees Health Benefits Plan (FEHBP) standard option

e Permanently extend the research tax credit for businesses

e Eliminate and modify several business tax expenditures (domestic production deduction /

LIFO* method of accounting / energy tax preferences for the oil and gas industry /

depreciation rules)

e International tax reform including a territorial system®

Note: 1) AMT is the Alternative Minimum Tax; 2) PEP is Personal Exemption Phase-out designed to eliminate personal income exemptions for high earners; 3) Pease is a similar

phase-out, but instead of applying to personal exemption, it applies to most of the itemized deductions of a taxpayer's claims (mortgage interest, charitable gifts, state & local taxes

paid, etc.); Pease is named after Representative Donald Pease (D-OH) who pushed for its enactment in 1990. 4) LIFO is Last In, First Out’ which tend to reduce corporations’ income

taxes in times of inflation. 5) A territorial tax system is a tax system that taxes only income that is created within the borders of a specific territory (usually a country). Source: National

Commission on Fiscal Responsibility and Reform, “The Moment of Truth: Report of the National Commission on Fiscal Responsibility and Reform,” 12/1/10. Note that the Report also

identified two other scenarios called the ‘The Zero Plan’ which eliminates all tax expenditures and ‘Tax Reform Trigger which forces Congress to undertake comprehensive tax reform

K P by 2012 by raising taxes for each year Congress fails to act.

|

(@ EB) www.kpcb.com USA Inc. | What Might a Turnaround Expert Consider? 410

HOUSE_OVERSIGHT_021046

Document Preview

Click to view full size

Extracted Information

Dates

Document Details

| Filename | HOUSE_OVERSIGHT_021046.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 2,779 characters |

| Indexed | 2026-02-04T16:43:29.697369 |