HOUSE_OVERSIGHT_022354.jpg

{kind=link}

Extracted Text (OCR)

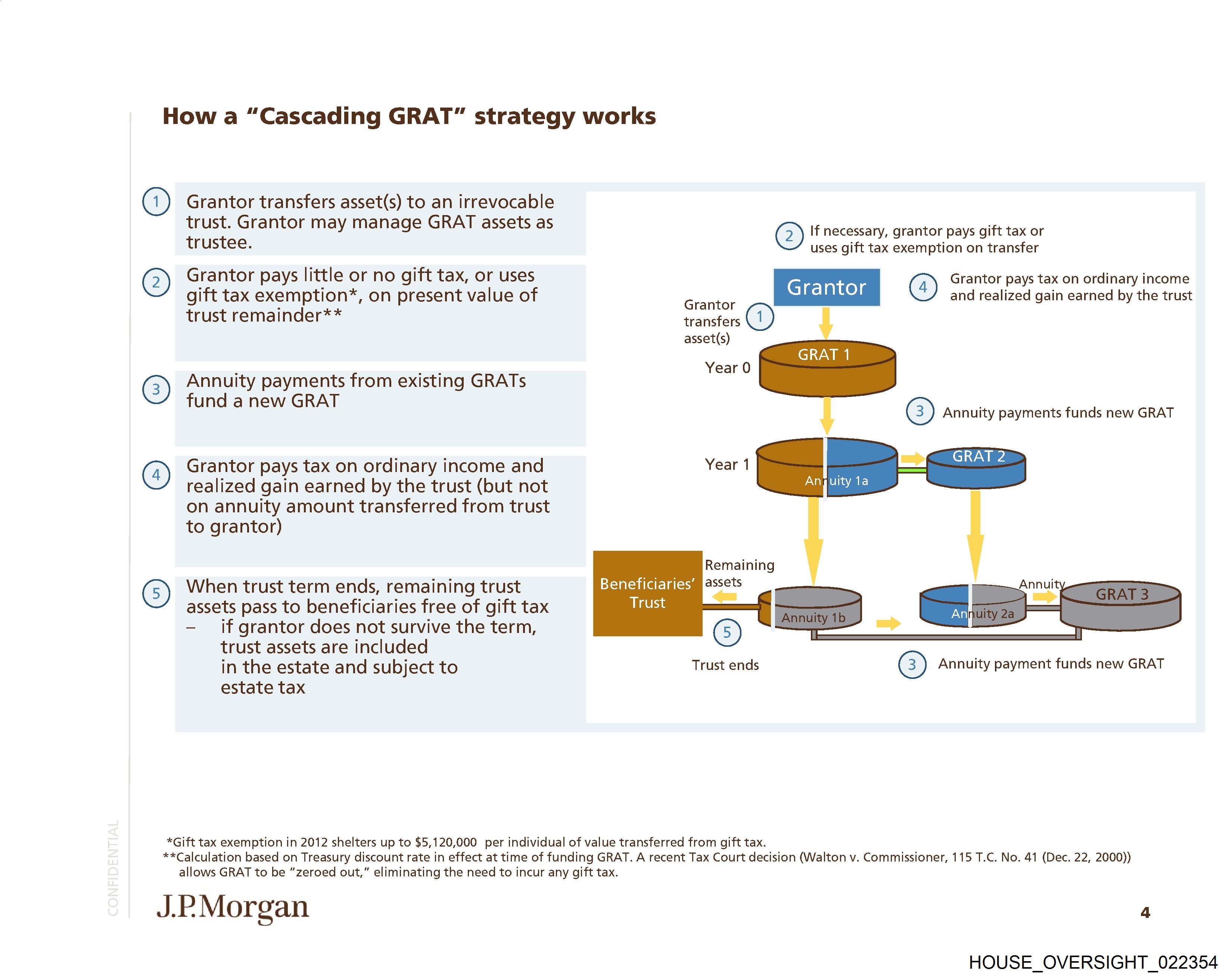

How a “Cascading GRAT” strategy works

G) Grantor transfers asset(s) to an irrevocable

trust. Grantor may manage GRAT assets as

trustee.

@ Grantor pays little or no gift tax, or uses

gift tax exemption*, on present value of

trust remainder**

Annuity payments from existing GRATs

fund a new GRAT

Grantor pays tax on ordinary income and

realized gain earned by the trust (but not

on annuity amount transferred from trust

to grantor)

©; When trust term ends, remaining trust

assets pass to beneficiaries free of gift tax

if grantor does not survive the term,

trust assets are included

in the estate and subject to

estate tax

Beneficiaries’ Estas

If necessary, grantor pays gift tax or

uses gift tax exemption on transfer

Grantor

Grantor

transfers G)

asset(s)

Year 0

Grantor pays tax on ordinary income

and realized gain earned by the trust

@) Annuity payments funds new GRAT

Year 1

Anguity 1a

Remaining

©

Trust ends

@) Annuity payment funds new GRAT

*Gift tax exemption in 2012 shelters up to $5,120,000 per individual of value transferred from gift tax.

**Calculation based on Treasury discount rate in effect at time of funding GRAT. A recent Tax Court decision (Walton v. Commissioner, 115 T.C. No. 41 (Dec. 22, 2000))

allows GRAT to be “zeroed out,” eliminating the need to incur any gift tax.

J.P Morgan

4

HOUSE_OVERSIGHT_022354

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_022354.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 1,351 characters |

| Indexed | 2026-02-04T16:47:43.777327 |