HOUSE_OVERSIGHT_023576.jpg

{kind=link}

Extracted Text (OCR)

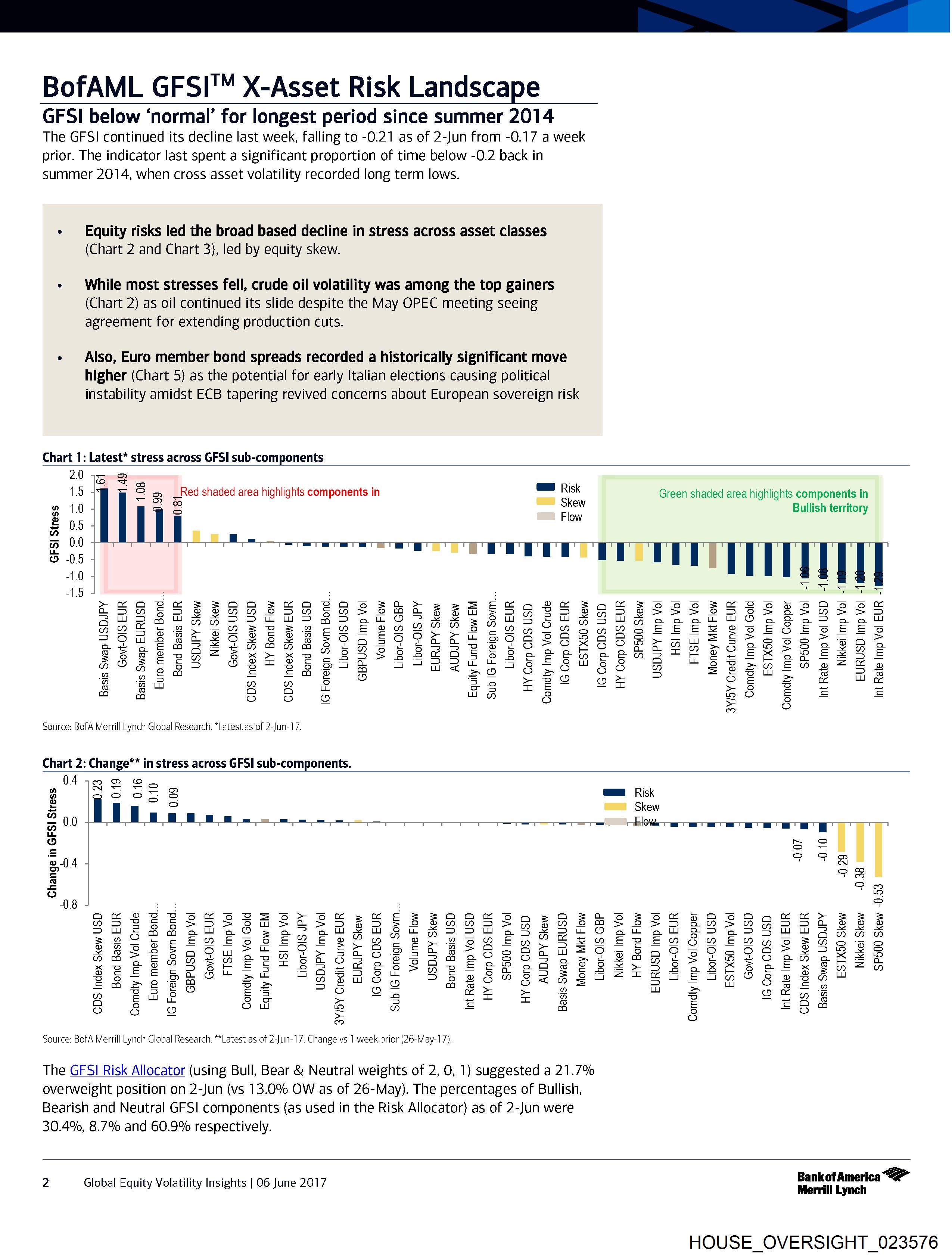

BofAML GFSI™ X-Asset Risk Landscape

GFSI below ‘normal’ for longest period since summer 2014

The GFSI continued its decline last week, falling to -0.21 as of 2-Jun from -0.17 a week

prior. The indicator last spent a significant proportion of time below -0.2 back in

summer 2014, when cross asset volatility recorded long term lows.

+ Equity risks led the broad based decline in stress across asset classes

(Chart 2 and Chart 3), led by equity skew.

¢ While most stresses fell, crude oil volatility was among the top gainers

(Chart 2) as oil continued its slide despite the May OPEC meeting seeing

agreement for extending production cuts.

« Also, Euro member bond spreads recorded a historically significant move

higher (Chart 5) as the potential for early Italian elections causing political

instability amidst ECB tapering revived concerns about European sovereign risk

Chart 1: Latest* stress across GFSI sub-components

2.0 5

1.5 4 2 2 _Red shaded area highlights components in = ak Green shaded area highlights components in

2 10 4 _ = Blew. Bullish territory

= 05

© 05 +

-1.0 2éeé

>eave aa erapras o> ce o x oc SBS erszsneunpSnBaS SEL

OTR EEE RR ESHRESBSEHSE EER ESR ES ESS SESESESSSRERESES

aAaMYrPatAHZ?-DPEYO mM et OTs K te SG4IDSGSFLDAYHZ eee bh Ue Ber ractt

RLAgGZ>~eVOREeEEZ eVEel2S rr FeclusBeseBsgEFLEETSeESOESEES

2Ome ee eOog ss see a soOleaes SPOsesscRe2oeser~njuzseagsgeresasa

See EDTA SPPTHODAZsSHRe ps se eet se ae EZtAPHRFOPRSFSEHBHE

$8 2Ba Sx XD BrP >see OR SB eo BAH BELG R =~ 2©®LTtE&EReaPEX SE

SSeE2EES ® @ tr oeecoco#E f®Fsaaf7ue £5 £Eet s 8 a “5 e535,5 2 Sr

Ao B Ee ESPta AT Tee zao 7S SB°° EO B@ SseFztntre2e" 52

n 2¢ a £ £ oO oo amv eas =) - co Ww oO oO

B 23 3 © = > so oz Og = « Wo

g gw & @ pe os 8 am & =x > 6 z = =

foe]

Source: BofA Merrill Lynch Global Research. *Latest as of 2-Jun-17.

Chart 2: Change** in stress across GFSI sub-components.

W499 2 Lo ;

a a — rr Gm Risk

FS i i i S oo Skew

un

é 2 |

= -

304 | o8

E Fg

08 | =

“ are evds or zB > oe we aAaaAKks fan as Se pasa oo >

Be See TS SSE SET ESSER BSSRPEGBSGESESSEESRSHRASSHESESES

TUF aAMmMeteOzpeoaPr ates sGtrAFrrDIuMes FItOet et ese5 oe td5guunRg FG

BE MPSOT FC END ES EEL ERS ApVPeSwenEDAgVEBZEMDEBENDSRENRDZEBRSGZS

@2@esesgs Ss) >i = oO FEF, Q2RnE8 8F84 az,ma=o75 oes) oAaAF> B®@a5 LS

AAFrESRPZERZ eeprHAseG BSR Z SG 2°88 SSE mr PSoRTS ti SstztoasnaokK =P

xpeePSesrestsesret ess hvtEestepes s SSBFr>SSasksee& x FH=zGH

[= a : [o} fast o = ca = so =

2eeeo PSC SS WGRBGSH PZeSV*BSZGZrATSATEWAGFS Lea"

2 202° Bs - Ya ez = 8 u 6s fy 8

a 3 = oO =~ BO

is) 8 oO ow & 7) = ao = EQa

a ra

Source: BofA Merrill Lynch Global Research. **Latest as of 2-Jun-17. Change vs 1 week prior (26-May-17).

The GFSI Risk Allocator (using Bull, Bear & Neutral weights of 2, 0, 1} suggested a 21.7%

overweight position on 2-Jun (vs 13.0% OW as of 26-May). The percentages of Bullish,

Bearish and Neutral GFSI components (as used in the Risk Allocator) as of 2-Jun were

30.4%, 8.7% and 60.9% respectively.

2 Global Equity Volatility Insights | 06 June 2017 oat Z

HOUSE_OVERSIGHT_023576

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_023576.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,057 characters |

| Indexed | 2026-02-04T16:51:27.186910 |