HOUSE_OVERSIGHT_023592.jpg

{kind=link}

Extracted Text (OCR)

Volatility in Asia

Use best-of puts to cheaply hedge a reversal in the rally

BofAML global strategists note that the massive central bank liquidity supernova has

allowed the Wall Street bull to flare higher, led by uber "growth" (EM internet stock

returns annualizing 125%). In light of this, we feel that it is prudent that investors

protect gains as we think today’s low volatility environment remains highly fragile,

characterized by the below stats:

« The MSCI Asia Pac index is up for the 5" consecutive month and is trading at multi-

year highs, while equity foreign inflows year-to-date are at the highest since 2004.

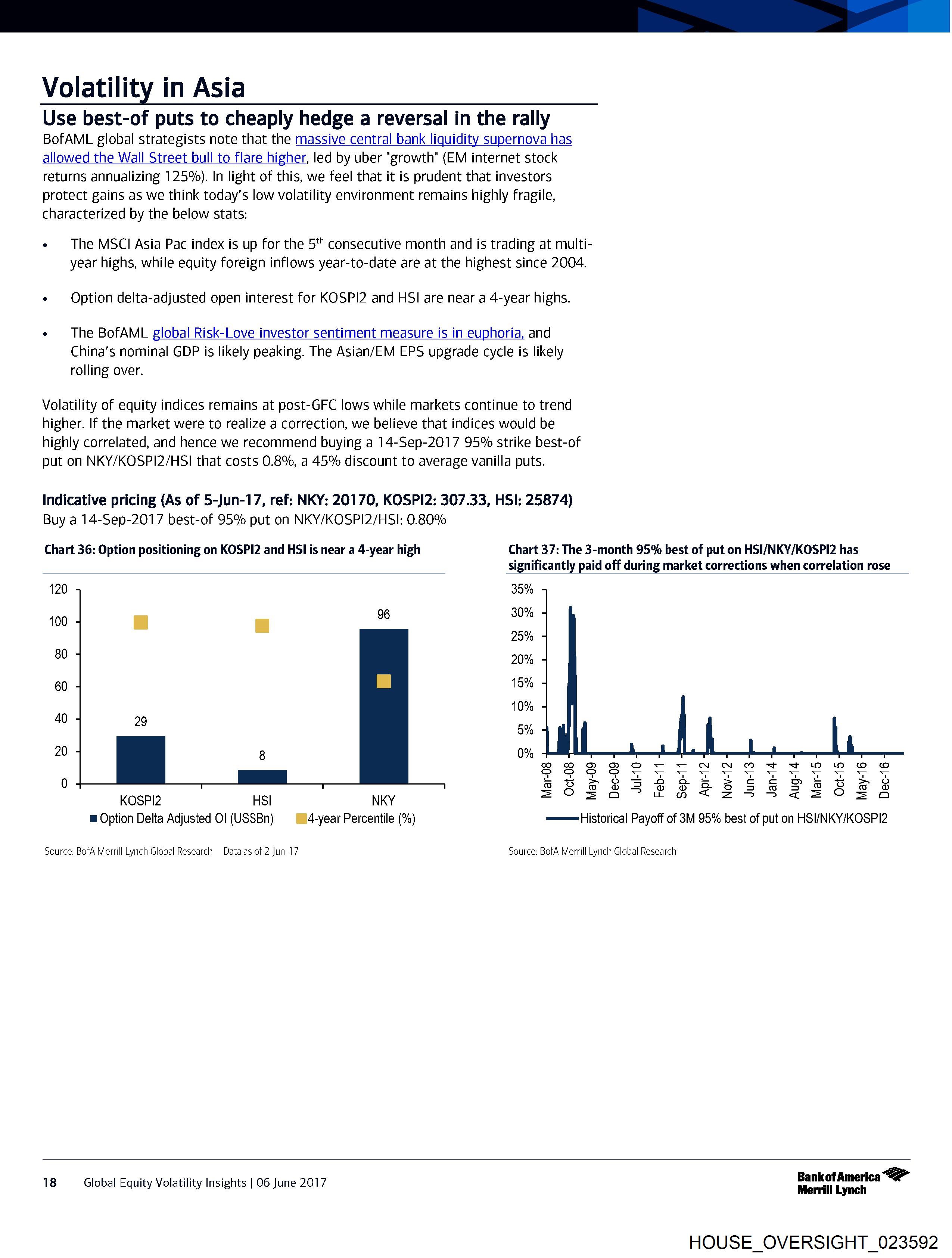

* Option delta-adjusted open interest for KOSPI2 and HSI are near a 4-year highs.

* The BofAML global Risk-Love investor sentiment measure is in euphoria, and

China’s nominal GDP is likely peaking. The Asian/EM EPS upgrade cycle is likely

rolling over.

Volatility of equity indices remains at post-GFC lows while markets continue to trend

higher. If the market were to realize a correction, we believe that indices would be

highly correlated, and hence we recommend buying a 14-Sep-2017 95% strike best-of

put on NKY/KOSPI2/HSI that costs 0.8%, a 45% discount to average vanilla puts.

Indicative pricing (As of 5-Jun-17, ref: NKY: 20170, KOSPI2: 307.33, HSI: 25874)

Buy a 14-Sep-2017 best-of 95% put on NKY/KOSPI2/HSI: 0.80%

Chart 36: Option positioning on KOSPI2 and HSI is near a 4-year high Chart 37: The 3-month 95% best of put on HSI/NKY/KOSPI2 has

significantly paid off during market corrections when correlation rose

120 35%

96 30%

100 Ol

= 25%

a0 20%

60 15%

Pn 10%

29 50%

20 8 0%

0 SRBPSESRSFEESEVEREB

} = 3 38 3}

KOSPI2 HSI NKY eve eet a Se . =" Se

@ Option Delta Adjusted Ol (US$Bn) ‘4-year Percentile (%) — Historical Payoff of 3M 95% best of put on HSI/NKY/KOSPI2

Source: BofA Merrill Lynch Global Research Data as of 2-Jun-17 Source: BofA Merrill Lynch Global Research

18 Global Equity Volatility Insights | 06 June 2017 oat 2

HOUSE_OVERSIGHT_023592

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_023592.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 1,997 characters |

| Indexed | 2026-02-04T16:51:29.565698 |