HOUSE_OVERSIGHT_023590.jpg

{kind=link}

Extracted Text (OCR)

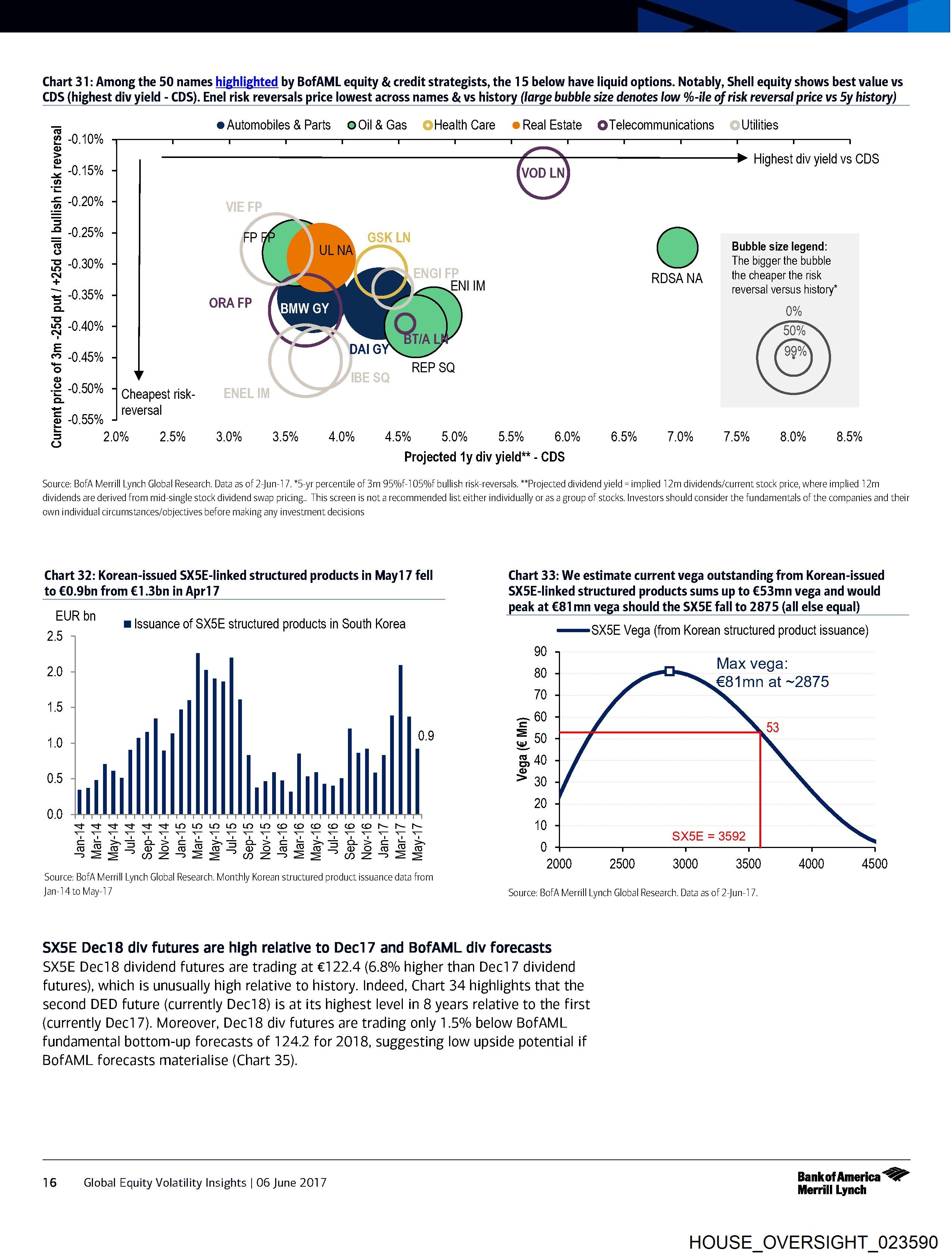

Chart 31: Among the 50 names highlighted by BofAML equity & credit strategists, the 15 below have liquid options. Notably, Shell equity shows best value vs

CDS (highest div yield - CDS). Enel risk reversals price lowest across names & vs history (large bubble size denotes low %-ile of risk reversal price vs 5y history)

e@ Automobiles & Parts @Oil&Gas HealthCare @RealEstate O@Telecommunications Utilities

-0.10%

Highest div yield vs CDS

Bubble size legend:

The bigger the bubble

RDSA NA the cheaper the risk

reversal versus history*

0.15%

0.20%

0.25%

0.30%

0.35%

0%

-~0.40%

-~0.45%

0.50%

Cheapest risk-

0.55% reversal

i 0

2.0% 2.5% 3.0% 3.5% 40% 45% 5.0% 5.5% 6.0% 6.5% 7.0% 7.5% 8.0% 8.5%

Projected 1y div yield** - CDS

Current price of 3m -25d put / +25d call bullish risk reversal

Source: BofA Merrill Lynch Global Research. Data as of 2-Jun-17. *5-yr percentile of 3m 959%f-105%f bullish risk-reversals. **Projected dividend yield = implied 12m dividends/current stack price, where implied 12m

dividends are derived from mid-single stock dividend swap pricing. This screen is not a recommended list either individually or as a group of stocks. Investors should consider the fundamentals of the companies and their

own individual circumstances/abjectives before making any investment decisions

Chart 32: Korean-issued SX5E-linked structured products in May1/7 fell Chart 33: We estimate current vega outstanding from Korean-issued

to €0.9bn from €1.3bn in Apr17 SX5E-linked structured products sums up to €53mn vega and would

peak at €81mn vega should the SX5E fall to 2875 (all else equal)

EUR bn .

35 m Issuance of SX5E structured products in South Korea SX5E Vega (from Korean structured product issuance)

90 M

ax vega:

2.0 80

€81mn at ~2875

45 70

, — 60

=

1.0 0.9 w 50

> 40

0.5 > 30

20

0.0

tttTTTMONMONMNNNDODOWOWOORRRER 10

= 08 = 0 BOS SO 8 = 2000 2500 3000 3500 4000 — 4500

Source: BofA Merrill Lynch Global Research. Monthly Korean structured product issuance data from

Jan-14 to May-17 Source: BofA Merrill Lynch Global Research. Data as of 2-Jun-17.

SX5E Dec18 div futures are high relative to Dec17 and BofAML div forecasts

SX5E Dec18 dividend futures are trading at €122.4 (6.8% higher than Dec17 dividend

futures), which is unusually high relative to history. Indeed, Chart 34 highlights that the

second DED future (currently Dec18) is at its highest level in 8 years relative to the first

(currently Dec17). Moreover, Dec18 div futures are trading only 1.5% below BofAML

fundamental bottom-up forecasts of 124.2 for 2018, suggesting low upside potential if

BofAML forecasts materialise (Chart 35).

deg oct Bankof America

16 Global Equity Volatility Insights | 06 June 2017 Merrill Lynch

HOUSE_OVERSIGHT_023590

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_023590.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 2,750 characters |

| Indexed | 2026-02-04T16:51:29.864281 |