HOUSE_OVERSIGHT_023588.jpg

{kind=link}

Extracted Text (OCR)

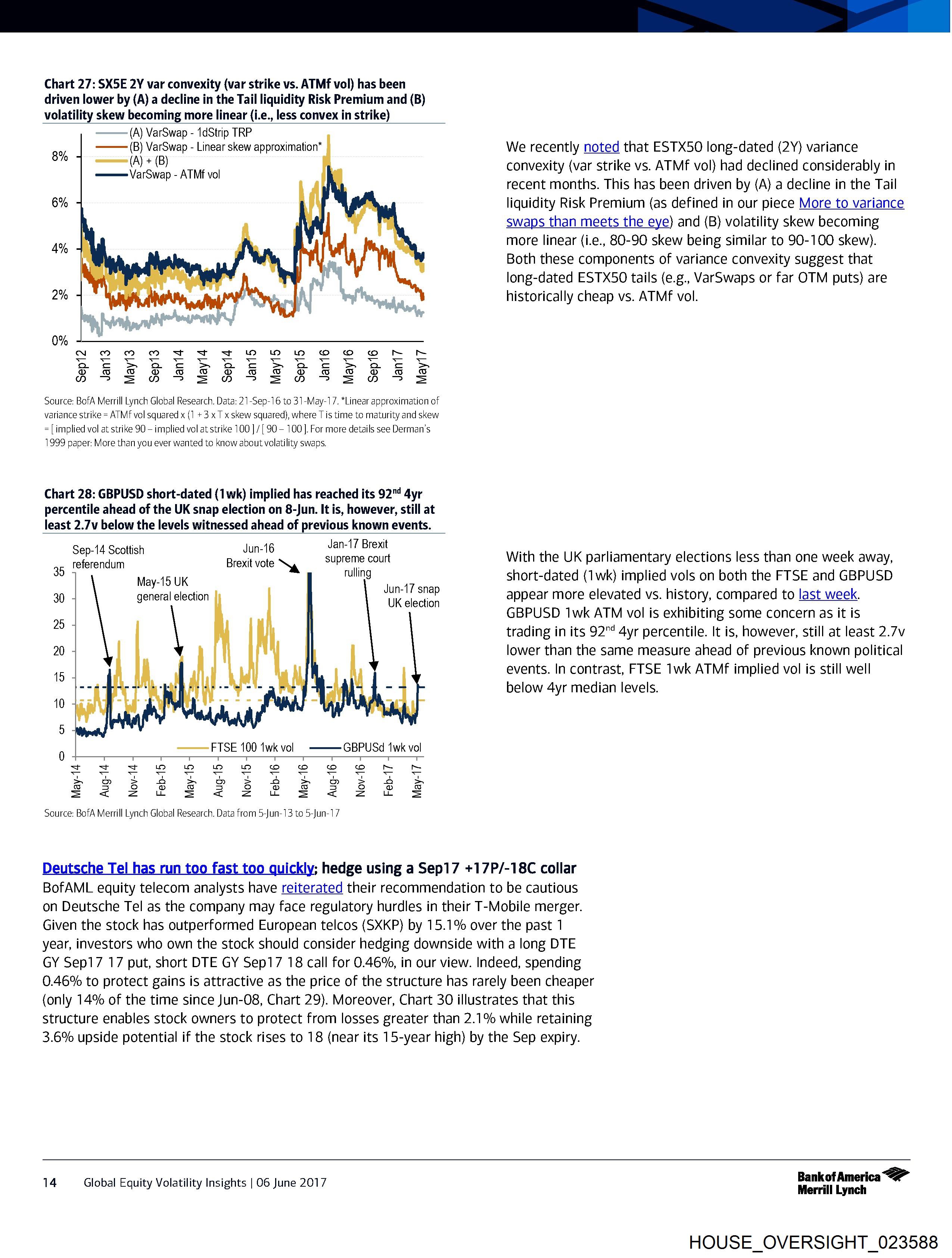

Chart 27: SX5E 2Y var convexity (var strike vs. ATMf vol) has been

driven lower by (A) a decline in the Tail liquidity Risk Premium and (B)

volatility skew becoming more linear (i.e., less convex in strike)

(A) VarSwap - 1dStrip TRP

any ——(B) VarSwap - Linear skew approximation* We recently noted that ESTX50 long-dated (2Y) variance

TF convexity (var strike vs. ATMf vol) had declined considerably in

———VarSwap - ATMf vol , F Boose od ‘

recent months. This has been driven by (A) a decline in the Tail

liquidity Risk Premium (as defined in our piece More to variance

swaps than meets the eye) and (B) volatility skew becoming

more linear (i.e., 80-90 skew being similar to 90-100 skew).

Both these components of variance convexity suggest that

long-dated ESTX50 tails (e.g., VarSwaps or far OTM puts} are

historically cheap vs. ATMf vol.

6%

4%

2%

0%

N OO MO OF FP TF TFT ODO DO) HO OO Ob Oo ~ Mm

Qo C£¢ > a2 ff SS a fC Se oho fll SlOelrl OT OD

on © funy wo fin] oC ®D o © fay o

QD - Soa > BSEnA FO BO FO BY OB

Source: BofA Merrill Lynch Global Research. Data: 21-Sep-16 to 31-May-17. *Linear approximation of

variance strike = ATMf vol squared x (1 +3 x T x skew squared), where Tis time to maturity and skew

= [implied vol at strike 90 - implied vol at strike 100 ]/[ 90- 100]. For more details see Derman’s

1999 paper: More than you ever wanted to know about volatility swaps.

Chart 28: GBPUSD short-dated (1 wk) implied has reached its 92"! 4yr

percentile ahead of the UK snap election on 8-Jun. It is, however, still at

least 2.7v below the levels witnessed ahead of previous known events.

_ ; Jun-16 Jan-17 Brexit ; ; ;

Se eatin Saseiarate Ng upteme court With the UK parliamentary elections less than one week away,

35 rulling

May-15 UK short-dated (1wk} implied vols on both the FTSE and GBPUSD

30 general election Jun-17 snap appear more elevated vs. history, compared to last week.

UK election . base mg, 2

GBPUSD 1wk ATM vol is exhibiting some concern as it is

a trading in its 92" 4yr percentile. It is, however, still at least 2.7v

20 lower than the same measure ahead of previous known political

15 events. In contrast, FTSE 1wk ATMf implied vol is still well

below 4yr median levels.

10

5

0

= = as Ww wo Ww Lo co co ico} co | aeed | maeed

eS 5 8rF bs BFF &b BE

=s 2228s 22828 82228 8

Source: BofA Merrill Lynch Global Research. Data from 5-Jun-13 to 5-Jun-17

D he Tel has run fi ickly; hedge using a Sep17 +17P/-18C collar

BofAML equity telecom analysts have reiterated their recommendation to be cautious

on Deutsche Tel as the company may face regulatory hurdles in their T-Mobile merger.

Given the stock has outperformed European telcos (SXKP) by 15.1% over the past 1

year, investors who own the stock should consider hedging downside with a long DTE

GY Sep17 17 put, short DTE GY Sep17 18 call for 0.46%, in our view. Indeed, spending

0.46% to protect gains is attractive as the price of the structure has rarely been cheaper

(only 14% of the time since Jun-08, Chart 29). Moreover, Chart 30 illustrates that this

structure enables stock owners to protect from losses greater than 2.1% while retaining

3.6% upside potential if the stock rises to 18 (near its 15-year high) by the Sep expiry.

deg oct Bankof America

14 Global Equity Volatility Insights | 06 June 2017 Merrill Lynch

HOUSE_OVERSIGHT_023588

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_023588.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,340 characters |

| Indexed | 2026-02-04T16:51:30.147055 |