HOUSE_OVERSIGHT_024149.jpg

{kind=link}

Extracted Text (OCR)

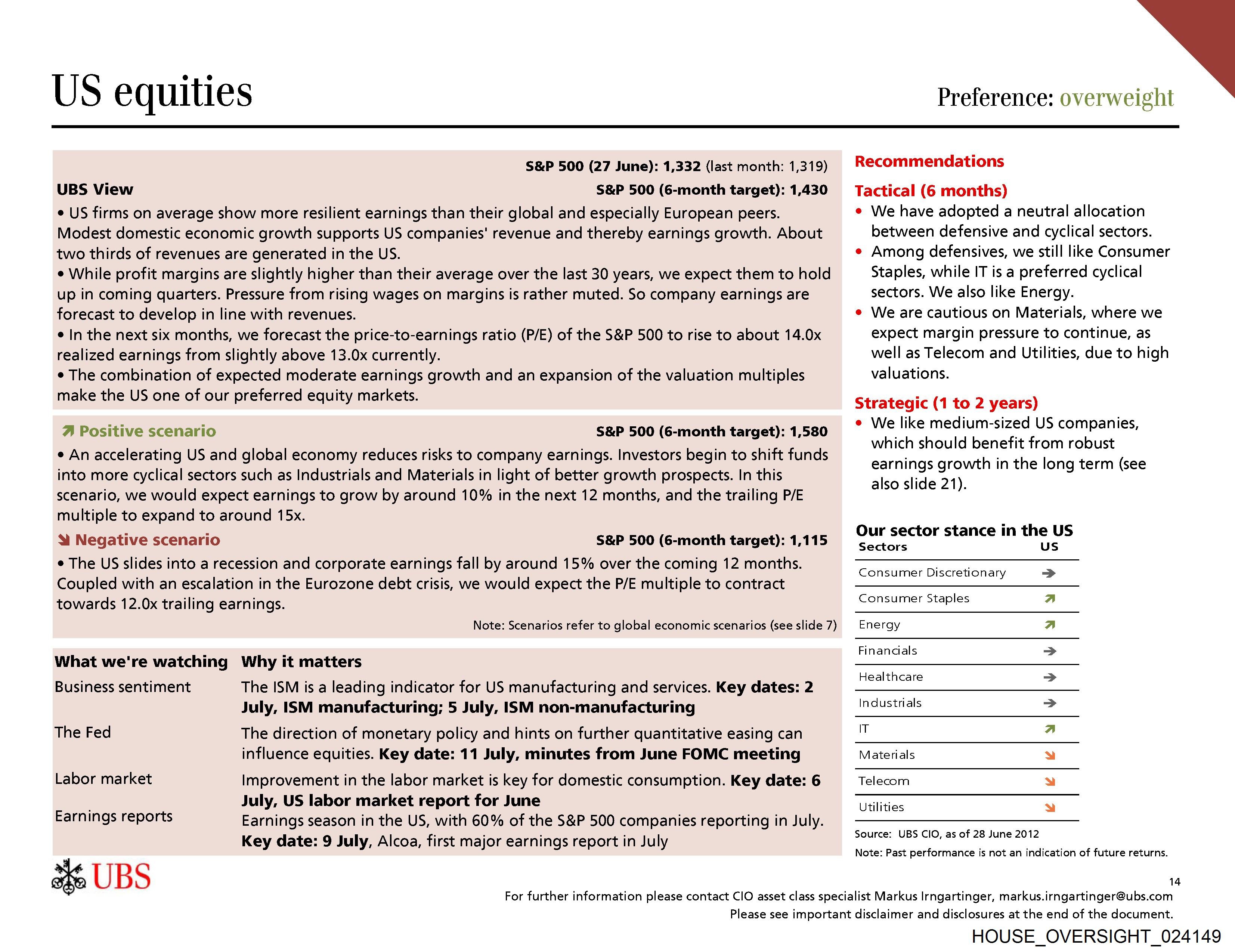

US equities

S&P 500 (27 June): 1,332 (last month: 1,319)

UBS View S&P 500 (6-month target): 1,430

e US firms on average show more resilient earnings than their global and especially European peers.

Modest domestic economic growth supports US companies' revenue and thereby earnings growth. About

two thirds of revenues are generated in the US.

¢ While profit margins are slightly higher than their average over the last 30 years, we expect them to hold

up in coming quarters. Pressure from rising wages on margins is rather muted. So company earnings are

forecast to develop in line with revenues.

e In the next six months, we forecast the price-to-earnings ratio (P/E) of the S&P 500 to rise to about 14.0x

realized earnings from slightly above 13.0x currently.

¢ The combination of expected moderate earnings growth and an expansion of the valuation multiples

make the US one of our preferred equity markets.

A Positive scenario S&P 500 (6-month target): 1,580

e An accelerating US and global economy reduces risks to company earnings. Investors begin to shift funds

into more cyclical sectors such as Industrials and Materials in light of better growth prospects. In this

scenario, we would expect earnings to grow by around 10% in the next 12 months, and the trailing P/E

multiple to expand to around 15x.

& Negative scenario S&P 500 (6-month target): 1,115

e The US slides into a recession and corporate earnings fall by around 15% over the coming 12 months.

Coupled with an escalation in the Eurozone debt crisis, we would expect the P/E multiple to contract

towards 12.0x trailing earnings.

Note: Scenarios refer to global economic scenarios (see slide 7)

What we're watching Why it matters

Business sentiment The ISM is a leading indicator for US manufacturing and services. Key dates: 2

July, ISM manufacturing; 5 July, ISM non-manufacturing

The Fed The direction of monetary policy and hints on further quantitative easing can

influence equities. Key date: 11 July, minutes from June FOMC meeting

Labor market Improvement in the labor market is key for domestic consumption. Key date: 6

July, US labor market report for June

Earnings reports Earnings season in the US, with 60% of the S&P 500 companies reporting in July.

Key date: 9 July, Alcoa, first major earnings report in July

3 UBS

Preference: overweight

Recommendations

Tactical (6 months)

e We have adopted a neutral allocation

between defensive and cyclical sectors.

e Among defensives, we still like Consumer

Staples, while IT is a preferred cyclical

sectors. We also like Energy.

e We are cautious on Materials, where we

expect margin pressure to continue, as

well as Telecom and Utilities, due to high

valuations.

Strategic (1 to 2 years)

e We like medium-sized US companies,

which should benefit from robust

earnings growth in the long term (see

also slide 21).

Our sector stance in the US

Sectors us

Consumer Discretionary

v

Consumer Staples

Energy

Financials

Healthcare

ndustrials

T

Materials

Telecom

e1e2¢/e;ulvlveyviauya

Utilities

Source: UBS CIO, as of 28 June 2012

Note: Past performance is not an indication of future returns.

14

For further information please contact CIO asset class specialist Markus Irngartinger, markus.irngartinger@ubs.com

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_024149

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_024149.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,360 characters |

| Indexed | 2026-02-04T16:53:17.028442 |