HOUSE_OVERSIGHT_024151.jpg

{kind=link}

Extracted Text (OCR)

UK equities

FTSE 100 (27 June): 5,524 (last month: 5,266)

UBS View FTSE 100 (6-month target): 5,785

¢ We continue to like UK equities relative to global ones. An expected improvement in the global economy

over the coming quarters should support UK companies as 70% of revenues are generated abroad.

e Energy is the largest sector of the UK market. While the oil price eased sharply over the past months, we

expect it to stabilize in the second half of 2012. An attractive valuation of the energy sector at 6.5x trailing

earnings provides some buffer for earnings volatility going forward.

e Profitability of UK banks is reasonable. They are less affected by the sovereign debt crisis than their

Eurozone peers. While the recent easing of collateral requirements by the Bank of England is supportive in

the short-term, the profitability of the domestic operations could be negatively affected by the

implementation of the ring-fencing bank reform by 2015.

¢ UK equities’ P/E, at about 10.0x trailing, indicates attractive value relative to global equities. Based on our

12-month forward earnings growth estimate of about 5% and the P/E multiple slightly expanding to 10.3x,

we expect UK equities to show good returns over the next six months.

4 Positive scenario FTSE 100 (6-month target): 6,650

¢ Continued global growth and strong demand from emerging markets should support demand for

commodities, helping the Materials and Energy sectors to lead the market higher. The market could re-rate

to a P/E multiple of close to 12.0x, and we would expect earnings growth of 5-8% over 12 months.

& Negative scenario FTSE 100 (6-month target): 4,400

e A global recession drags UK earnings down by 15-20%. The market's defensive characteristics would only

partly offset its strong exposure to commodity-related sectors. We would expect the trailing P/E multiple to

drop towards slightly below 9x.

Note: Scenarios refer to global economic scenarios (see slide 7)

What we're watching Why it matters

Growth indicators Business survey indicators provide information on the economic development in

the UK. Key date: 2 July, PMI manufacturing for June; 4 July, PMI services

for June;

Commodity prices Energy and Materials together are about 30% of the UK market by market

capitalization. Developments in commodity prices affect earnings estimates.

Policy action Loose monetary policy by the Bank of England (BoE) supports equities. Key date:

05 July, Bank of England policy meeting

Preference: overweight

Recommendations

Tactical (6 months)

e We like the Energy sector due to

attractive valuations; Consumer Staples

is another preferred sector Because of

its defensive qualities.

e Approaching the end of the patent cliff

should remove some uncertainty on the

Healthcare sector and enable a re-

rating.

Strategic (1 to 2 years)

e As commodity-related sectors, Energy

and Materials should benefit from

robust demand in emerging markets.

e The UK market's 4% dividend yield

provides a good income stream.

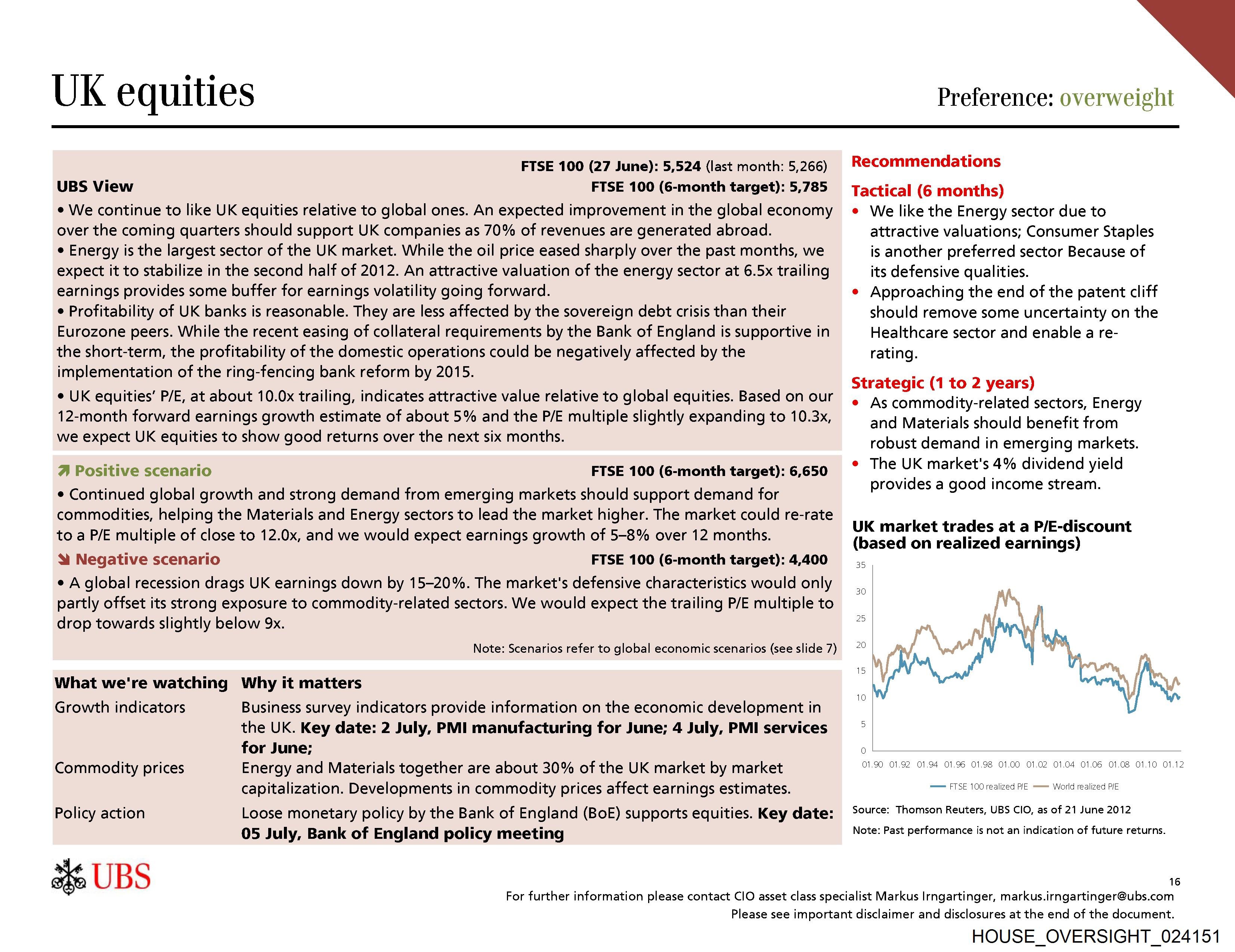

UK market trades at a P/E-discount

(based on realized earnings)

01.90 01.92 01.94 01.96 01.98 01.00 01.02 01.04 01.06 01.08 01.10 01.12

—— FTSE 100 realized PIE World realized PIE

Source: Thomsen Reuters, UBS CIO, as of 21 June 2012

Note: Past performance is not an indication of future returns.

16

For further information please contact CIO asset class specialist Markus Irngartinger, markus.irngartinger@ubs.com

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_024151

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_024151.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,533 characters |

| Indexed | 2026-02-04T16:53:17.337705 |