HOUSE_OVERSIGHT_024148.jpg

{kind=link}

Extracted Text (OCR)

Equities overview

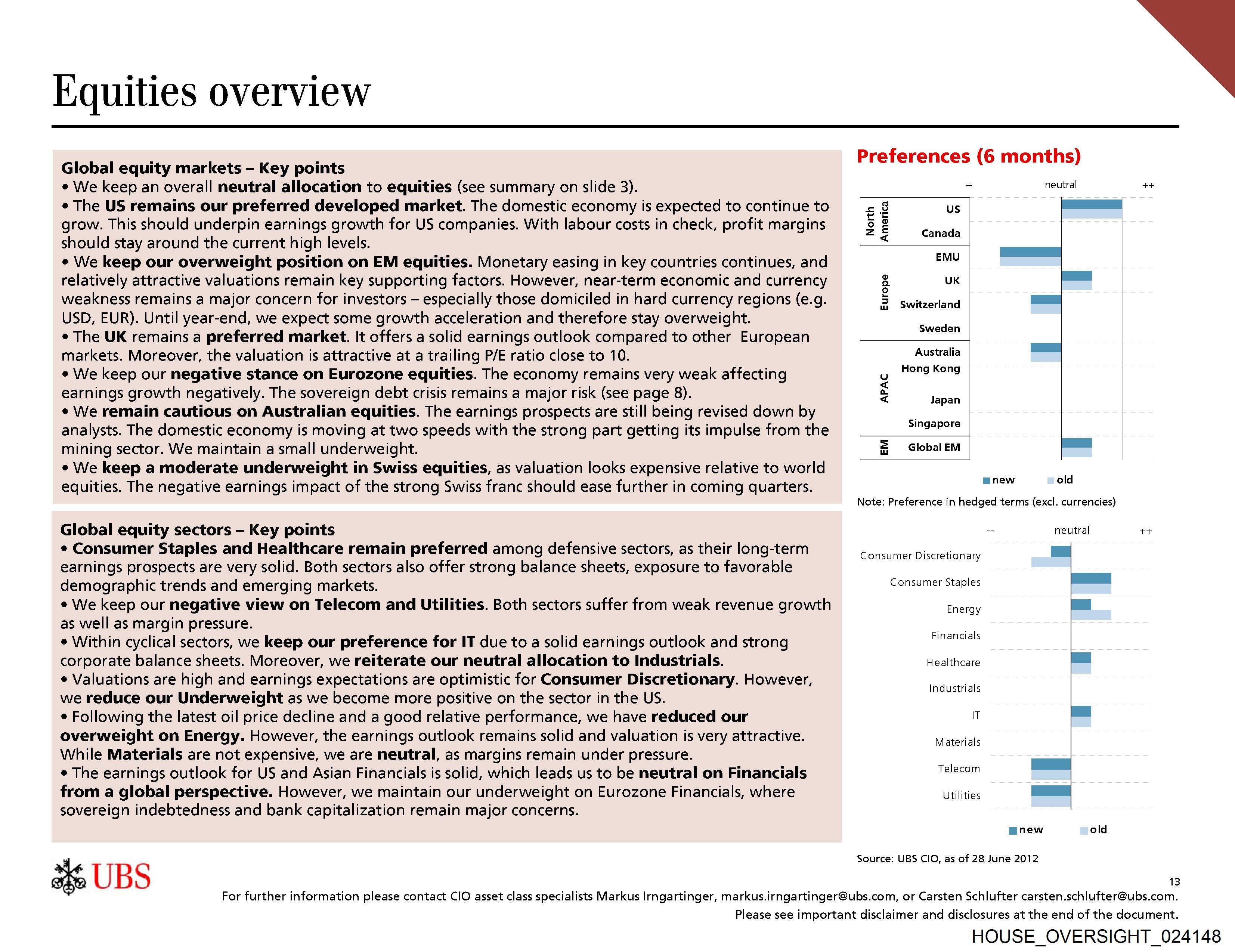

Global equity markets -— Key points

¢ We keep an overall neutral allocation to equities (see summary on slide 3).

¢ The US remains our preferred developed market. The domestic economy is expected to continue to

grow. This should underpin earnings growth for US companies. With labour costs in check, profit margins

should stay around the current high levels.

e We keep our overweight position on EM equities. Monetary easing in key countries continues, and

relatively attractive valuations remain key supporting factors. However, near-term economic and currency

weakness remains a major concern for investors — especially those domiciled in hard currency regions (e.g.

USD, EUR). Until year-end, we expect some growth acceleration and therefore stay overweight.

¢ The UK remains a preferred market. It offers a solid earnings outlook compared to other European

markets. Moreover, the valuation is attractive at a trailing P/E ratio close to 10.

¢ We keep our negative stance on Eurozone equities. The economy remains very weak affecting

earnings growth negatively. The sovereign debt crisis remains a major risk (see page 8).

¢ We remain cautious on Australian equities. The earnings prospects are still being revised down by

analysts. The domestic economy is moving at two speeds with the strong part getting its impulse from the

mining sector. We maintain a small underweight.

¢ We keep a moderate underweight in Swiss equities, as valuation looks expensive relative to world

equities. The negative earnings impact of the strong Swiss franc should ease further in coming quarters.

Global equity sectors - Key points

¢ Consumer Staples and Healthcare remain preferred among defensive sectors, as their long-term

earnings prospects are very solid. Both sectors also offer strong balance sheets, exposure to favorable

demographic trends and emerging markets.

¢ We keep our negative view on Telecom and Utilities. Both sectors suffer from weak revenue growth

as well as margin pressure.

¢ Within cyclical sectors, we keep our preference for IT due to a solid earnings outlook and strong

corporate balance sheets. Moreover, we reiterate our neutral allocation to Industrials.

¢ Valuations are high and earnings expectations are optimistic for Consumer Discretionary. However,

we reduce our Underweight as we become more positive on the sector in the US.

¢ Following the latest oil price decline and a good relative performance, we have reduced our

overweight on Energy. However, the earnings outlook remains solid and valuation is very attractive.

While Materials are not expensive, we are neutral, as margins remain under pressure.

¢ The earnings outlook for US and Asian Financials is solid, which leads us to be neutral on Financials

from a global perspective. However, we maintain our underweight on Eurozone Financials, where

sovereign indebtedness and bank capitalization remain major concerns.

36 UBS

Preferences (6 months)

- neutral ++

<8 US =a

53

2 L Canada

EMU Po

4 UK es

i Switzerland =|

Sweden

Australia =

Hong Kon

u g 9

<

a

4 Japan

Singapore

= GlobalEM —

mnew old

Note: Preference in hedged terms (excl. currencies)

- neutral ++

Consumer Discretionary

Consumer Staples

Energy

Financials

Healthcare

Industrials

IT

Materials

Telecom

Utilities

mnew old

Source: UBS CIO, as of 28 June 2012

13

For further information please contact CIO asset class specialists Markus Irngartinger, markus.irngartinger@ubs.com, or Carsten Schlufter carsten.schlufter@ubs.com.

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_024148

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_024148.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,610 characters |

| Indexed | 2026-02-04T16:53:17.347223 |