HOUSE_OVERSIGHT_024150.jpg

{kind=link}

Extracted Text (OCR)

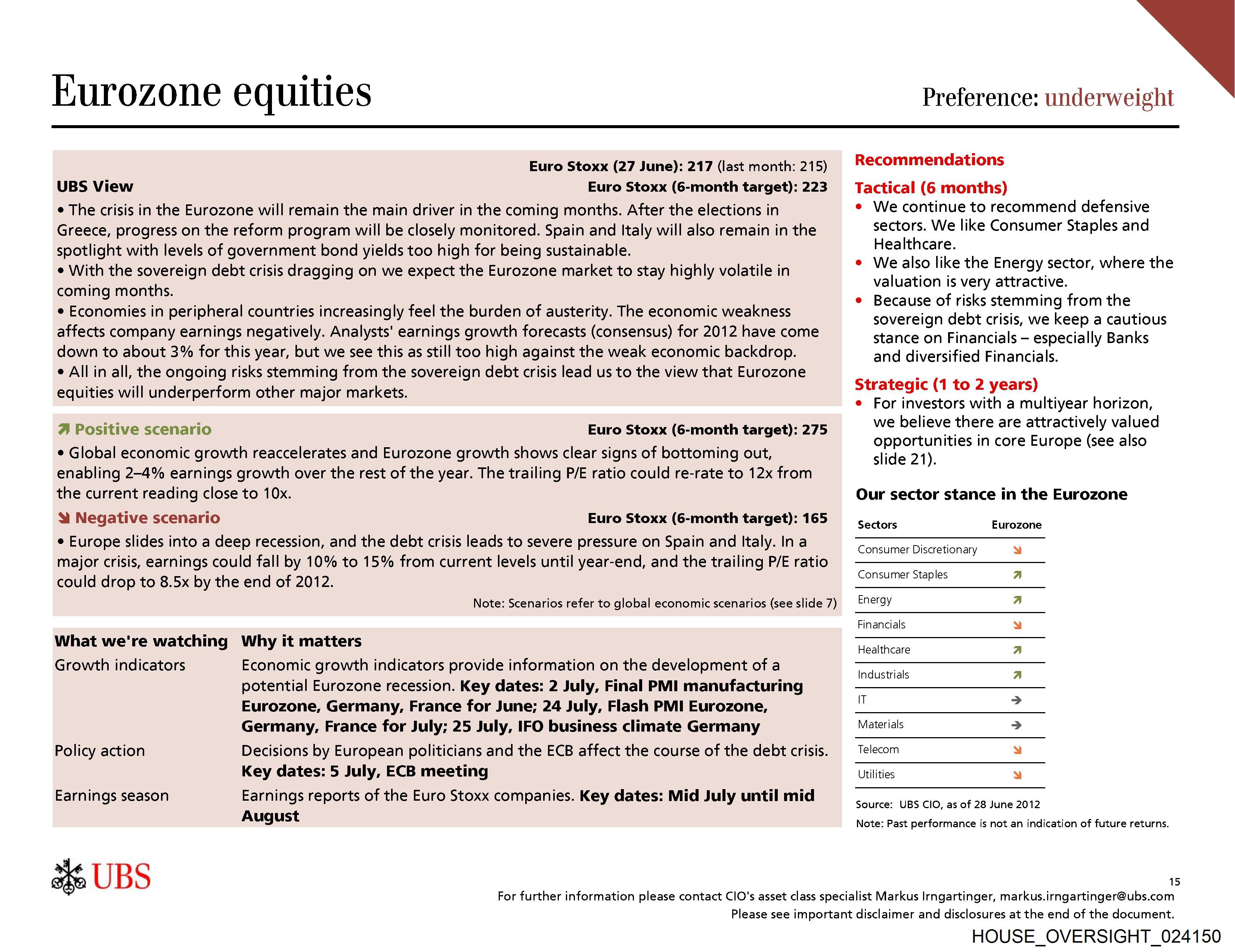

Eurozone equities

Euro Stoxx (27 June): 217 (last month: 215)

UBS View Euro Stoxx (6-month target): 223

¢ The crisis in the Eurozone will remain the main driver in the coming months. After the elections in

Greece, progress on the reform program will be closely monitored. Spain and Italy will also remain in the

spotlight with levels of government bond yields too high for being sustainable.

e With the sovereign debt crisis dragging on we expect the Eurozone market to stay highly volatile in

coming months.

e Economies in peripheral countries increasingly feel the burden of austerity. The economic weakness

affects company earnings negatively. Analysts' earnings growth forecasts (consensus) for 2012 have come

down to about 3% for this year, but we see this as still too high against the weak economic backdrop.

¢ All in all, the ongoing risks stemming from the sovereign debt crisis lead us to the view that Eurozone

equities will underperform other major markets.

A Positive scenario Euro Stoxx (6-month target): 275

¢ Global economic growth reaccelerates and Eurozone growth shows clear signs of bottoming out,

enabling 2-4% earnings growth over the rest of the year. The trailing P/E ratio could re-rate to 12x from

the current reading close to 10x.

& Negative scenario Euro Stoxx (6-month target): 165

¢ Europe slides into a deep recession, and the debt crisis leads to severe pressure on Spain and Italy. In a

major crisis, earnings could fall by 10% to 15% from current levels until year-end, and the trailing P/E ratio

could drop to 8.5x by the end of 2012.

Note: Scenarios refer to global economic scenarios (see slide 7)

What we're watching Why it matters

Growth indicators Economic growth indicators provide information on the development of a

potential Eurozone recession. Key dates: 2 July, Final PMI manufacturing

Eurozone, Germany, France for June; 24 July, Flash PMI Eurozone,

Germany, France for July; 25 July, IFO business climate Germany

Decisions by European politicians and the ECB affect the course of the debt crisis.

Key dates: 5 July, ECB meeting

Earnings reports of the Euro Stoxx companies. Key dates: Mid July until mid

August

Policy action

Earnings season

36 UBS

Preference: underweight

Recommendations

Tactical (6 months)

We continue to recommend defensive

sectors. We like Consumer Staples and

Healthcare.

We also like the Energy sector, where the

valuation is very attractive.

Because of risks stemming from the

sovereign debt crisis, we keep a cautious

stance on Financials — especially Banks

and diversified Financials.

pitnegee (1 to 2 years)

For investors with a multiyear horizon,

we believe there are attractively valued

opportunities in core Europe (see also

slide 21).

Our sector stance in the Eurozone

Sectors

Consumer Discretionary

Consumer Staples

Energy

T

Financials

Healthcare

ndustrials

Telecom

Utilities

Eurozone

4

aterials

~e;/e_|/vjviulule;aulyau

Source: UBS CIO, as of 28 June 2012

Note: Past performance is not an indication of future returns.

15

For further information please contact CIO's asset class specialist Markus Irngartinger, markus.irngartinger@ubs.com

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_024150

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_024150.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,254 characters |

| Indexed | 2026-02-04T16:53:17.843635 |