HOUSE_OVERSIGHT_024175.jpg

{kind=link}

Extracted Text (OCR)

Hedge funds

UBS View Prefer Relative value and Event-driven

° We expect hedge funds (HF) to offer positive asymmetric returns characteristics vs. the S&P 500 due to

active management and stop-loss strategies. (HF were down 1.9% in May 2012 vs MSCI world at -8.5%)

¢ Decelerating global growth prospects, the next leg in the ongoing Eurozone crisis, is challenging mostly

equity long-short managers, who are net-long the market. While event-driven managers share some of

the performance drivers, idiosyncratic bets (event) reduce the exposure to markets. The real reason to own

this strategy, however, is the potential for out-sized return in distressed, high yield and other credit

investments as the Eurozone crisis plays out. The inherent hedging in relative-value should remain

appealing. Credit relative-value managers should perform well in this environment of higher fixed income

volatility and increasing pricing anomalies created by central bank interventions (OT2) and limited

competition.

A Positive scenario Prefer Equity long-short

e A reduction of uncertainty (e.g. resolution in Europe) lowers equities’ correlation and volatility. This

helps bottom-up fundamental analysis and equity long/short managers the most. Also, CEOs will likely

make more corporate transactions that can be monetized by event-driven managers, and a clearer

macroeconomic environment with more persistent trends would be supportive for macro managers

‘Negative scenario Prefer Trading (Global Macro + CTA)

e A 2011-type scenario in which hedge fund managers get whipsawed through the year with risk-on and

risk-off circumstances, driven by a multitude of political interventions, is difficult to anticipate. That would

impact long-short managers, event-driven, and to a lesser extent global macro managers.

Note: Scenarios refer to global economic scenarios (see slide 7)

What we're watching Why it matters

Global equity direction The outlook for global equities becomes an important HF performance driver.

/ economic cycle The economic cycle impacts the strategies differently.

Correlation Correlation among pair-stocks; an important performance/alpha driver for

equity long/short, the largest HF strategy by assets under management.

Leverage Gross and net leverage are key to monitoring risk.

Volatility The direction influences certain HF strategies (e.g. convertible arbitrage).

Liquidity Particularly for large HF that are less nimble to enter and exit their strategies

Regulation Volcker's rule, USCITS III/IV

36 UBS

Recommendations

Strategic (1 to 2 years)

Active risk management is instrumental for

capital preservation during adverse market

conditions. At the moment, we therefore

favor relative value and event-driven

strategies, since they are less hinged to

equity markets and other risky assets than

trading is.

Value proposition: Hedge funds should

achieve robust performance over an

extended horizon, while displaying limited

volatility vis-a-vis equities and other risky

assets, in general. Hedge funds minimize

downside losses in adverse market

conditions (e.g. active risk management)

and play a crucial role in wealth

appreciation, since there is less ground to

regain in the recovery phase and

ultimately greater chances for superior

long-term returns.

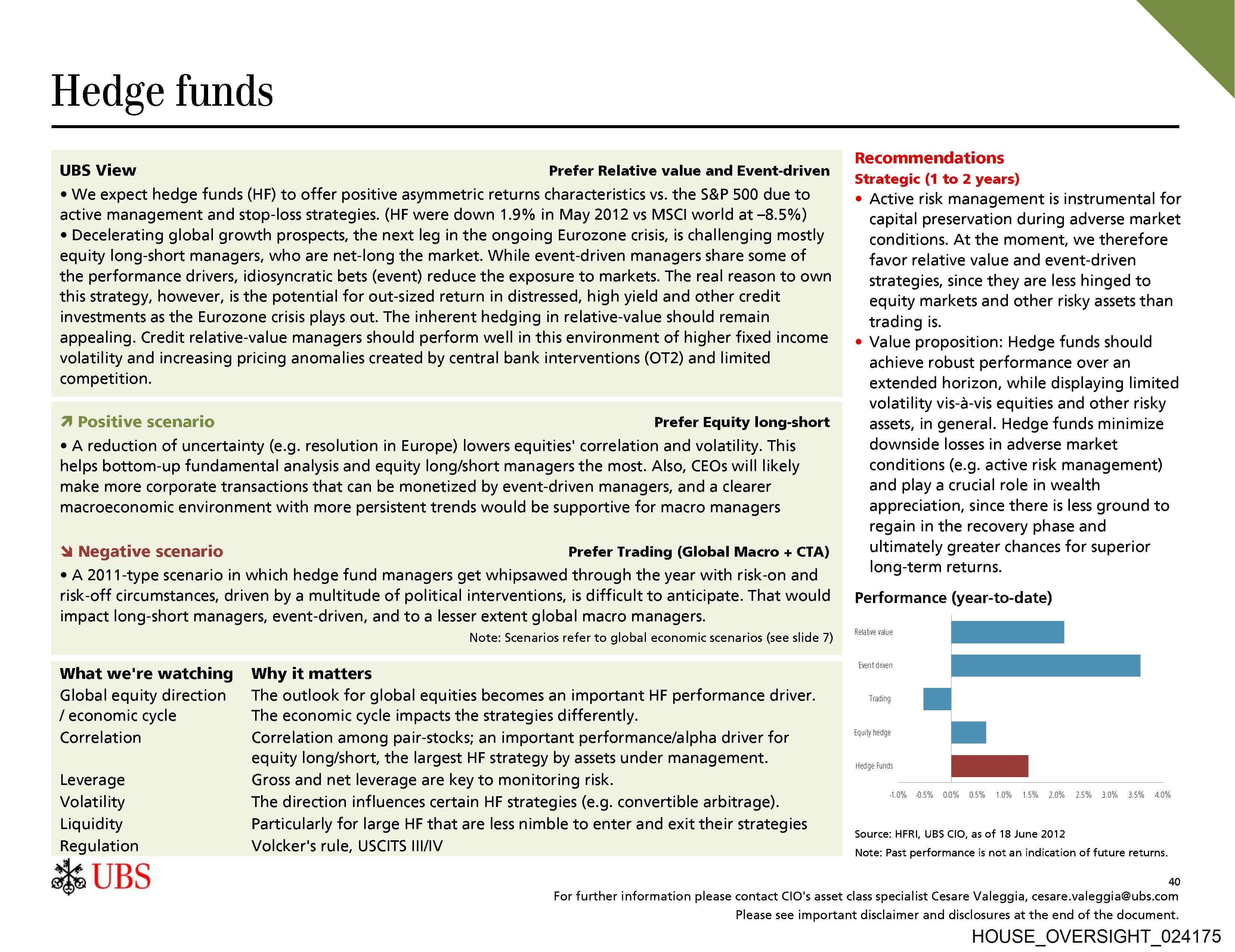

Performance (year-to-date)

Relative value

Event driven

Equity hedge

Hedge Funds

Trading

1.0% 0.5% 0.0% 05% 1.0% 15% 20% 25% 3.0% 3.5% 40%

Source: HFRI, UBS CIO, as of 18 June 2012

Note: Past performance is not an indication of future returns.

40

For further information please contact CIO's asset class specialist Cesare Valeggia, cesare.valeggia@ubs.com

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_024175

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_024175.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,745 characters |

| Indexed | 2026-02-04T16:53:24.320304 |