HOUSE_OVERSIGHT_024209.jpg

{kind=link}

Extracted Text (OCR)

Global Utility White Paper CONFIDENTIAL

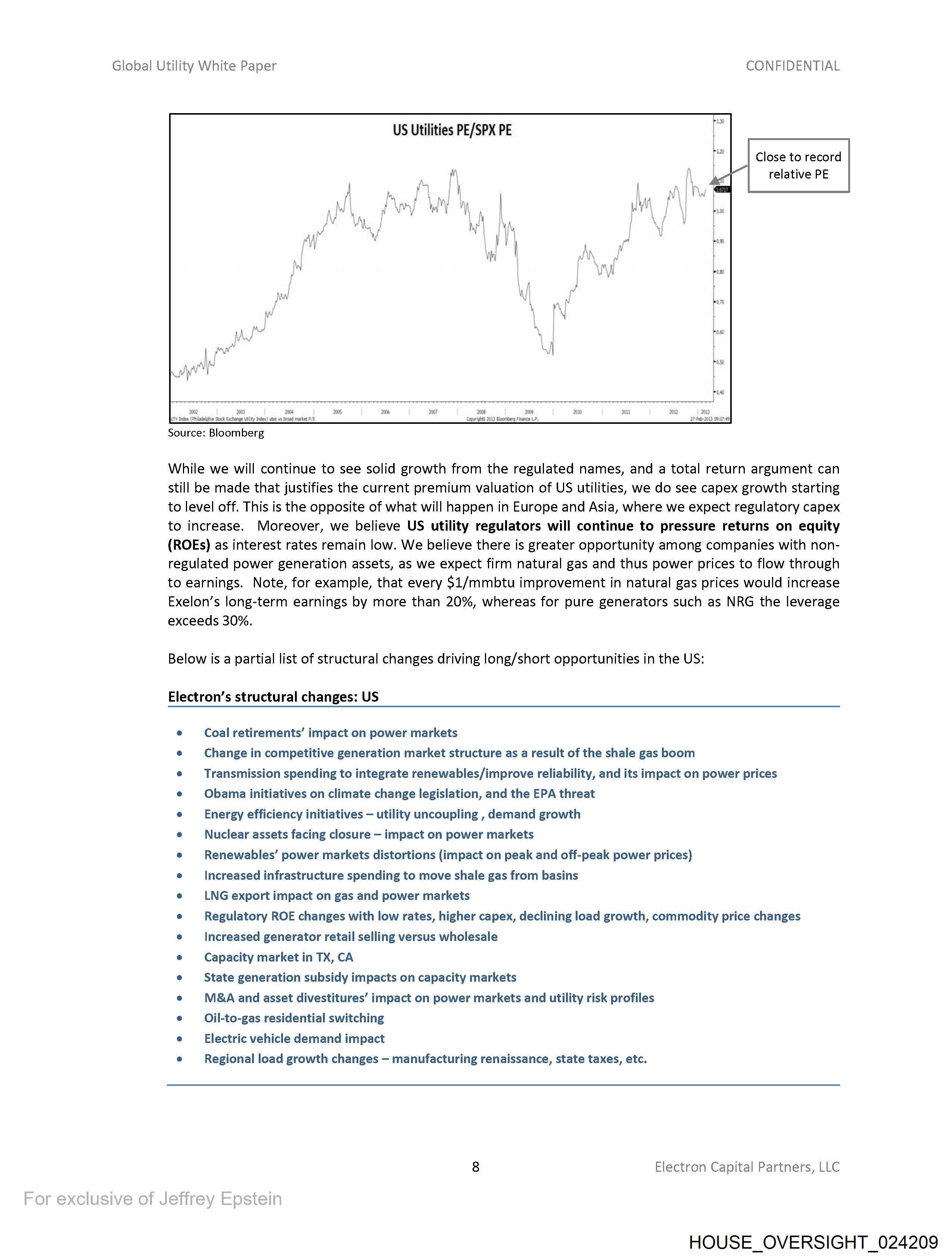

US Utilities PE/SPX PE

Close to record

relative PE

oot Bs) Ee

JUTY face (Piladeighia Sock Eachurige Utlity Inca) utes vn tread mare #1

Source: Bloomberg

While we will continue to see solid growth from the regulated names, and a total return argument can

still be made that justifies the current premium valuation of US utilities, we do see capex growth starting

to level off. This is the opposite of what will happen in Europe and Asia, where we expect regulatory capex

to increase. Moreover, we believe US utility regulators will continue to pressure returns on equity

(ROEs) as interest rates remain low. We believe there is greater opportunity among companies with non-

regulated power generation assets, as we expect firm natural gas and thus power prices to flow through

to earnings. Note, for example, that every $1/mmbtu improvement in natural gas prices would increase

Exelon’s long-term earnings by more than 20%, whereas for pure generators such as NRG the leverage

exceeds 30%.

Below is a partial list of structural changes driving long/short opportunities in the US:

Electron’s structural changes: US

e Coal retirements’ impact on power markets

e Change in competitive generation market structure as a result of the shale gas boom

¢ Transmission spending to integrate renewables/improve reliability, and its impact on power prices

e Obama initiatives on climate change legislation, and the EPA threat

e = Energy efficiency initiatives — utility uncoupling , demand growth

e Nuclear assets facing closure — impact on power markets

e Renewables’ power markets distortions (impact on peak and off-peak power prices)

e Increased infrastructure spending to move shale gas from basins

e LNG export impact on gas and power markets

e Regulatory ROE changes with low rates, higher capex, declining load growth, commodity price changes

e Increased generator retail selling versus wholesale

e Capacity market in TX, CA

e State generation subsidy impacts on capacity markets

e M&A and asset divestitures’ impact on power markets and utility risk profiles

e = Oil-to-gas residential switching

e —_ Electric vehicle demand impact

e Regional load growth changes — manufacturing renaissance, state taxes, etc.

8 Electron Capital Partners, LLC

HOUSE_OVERSIGHT_024209

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_024209.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 2,326 characters |

| Indexed | 2026-02-04T16:53:30.386934 |

Related Documents

Documents connected by shared names, same document type, or nearby in the archive.