HOUSE_OVERSIGHT_024218.jpg

{kind=link}

Extracted Text (OCR)

Global Utility White Paper CONFIDENTIAL

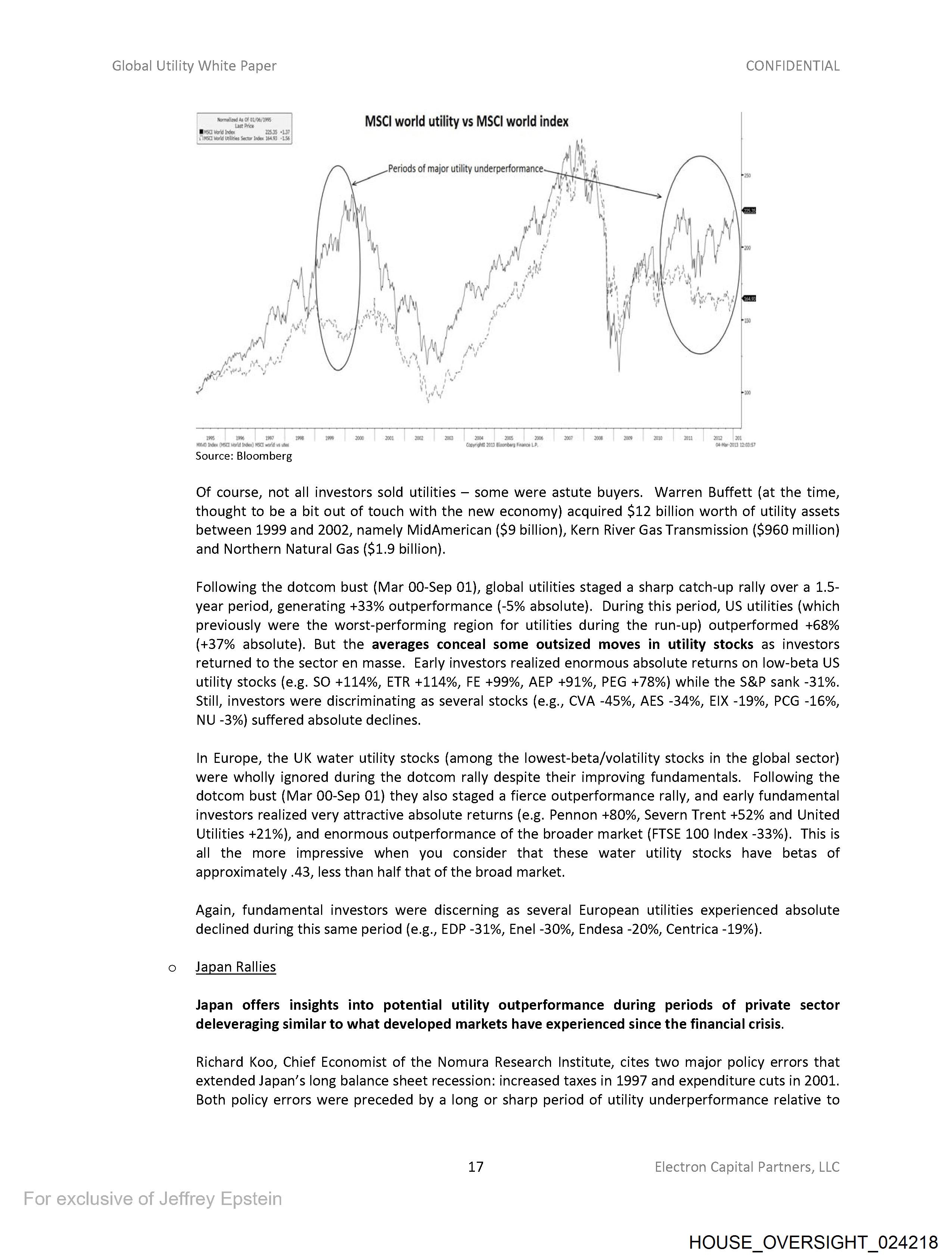

MSCI world utility vs MSCI world index

__———=

Source: Bloomberg

Of course, not all investors sold utilities - some were astute buyers. Warren Buffett (at the time,

thought to be a bit out of touch with the new economy) acquired $12 billion worth of utility assets

between 1999 and 2002, namely MidAmerican ($9 billion), Kern River Gas Transmission (S960 million)

and Northern Natural Gas ($1.9 billion).

Following the dotcom bust (Mar 00-Sep 01), global utilities staged a sharp catch-up rally over a 1.5-

year period, generating +33% outperformance (-5% absolute). During this period, US utilities (which

previously were the worst-performing region for utilities during the run-up) outperformed +68%

(+37% absolute). But the averages conceal some outsized moves in utility stocks as investors

returned to the sector en masse. Early investors realized enormous absolute returns on low-beta US

utility stocks (e.g. SO +114%, ETR +114%, FE +99%, AEP +91%, PEG +78%) while the S&P sank -31%.

Still, investors were discriminating as several stocks (e.g., CVA -45%, AES -34%, EIX -19%, PCG -16%,

NU -3%) suffered absolute declines.

In Europe, the UK water utility stocks (among the lowest-beta/volatility stocks in the global sector)

were wholly ignored during the dotcom rally despite their improving fundamentals. Following the

dotcom bust (Mar 00-Sep 01) they also staged a fierce outperformance rally, and early fundamental

investors realized very attractive absolute returns (e.g. Pennon +80%, Severn Trent +52% and United

Utilities +21%), and enormous outperformance of the broader market (FTSE 100 Index -33%). This is

all the more impressive when you consider that these water utility stocks have betas of

approximately .43, less than half that of the broad market.

Again, fundamental investors were discerning as several European utilities experienced absolute

declined during this same period (e.g., EDP -31%, Enel -30%, Endesa -20%, Centrica -19%).

o Japan Rallies

Japan offers insights into potential utility outperformance during periods of private sector

deleveraging similar to what developed markets have experienced since the financial crisis.

Richard Koo, Chief Economist of the Nomura Research Institute, cites two major policy errors that

extended Japan’s long balance sheet recession: increased taxes in 1997 and expenditure cuts in 2001.

Both policy errors were preceded by a long or sharp period of utility underperformance relative to

17 Electron Capital Partners, LLC

HOUSE_OVERSIGHT_024218

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_024218.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 2,563 characters |

| Indexed | 2026-02-04T16:53:32.524478 |