HOUSE_OVERSIGHT_025262.jpg

{kind=link}

Extracted Text (OCR)

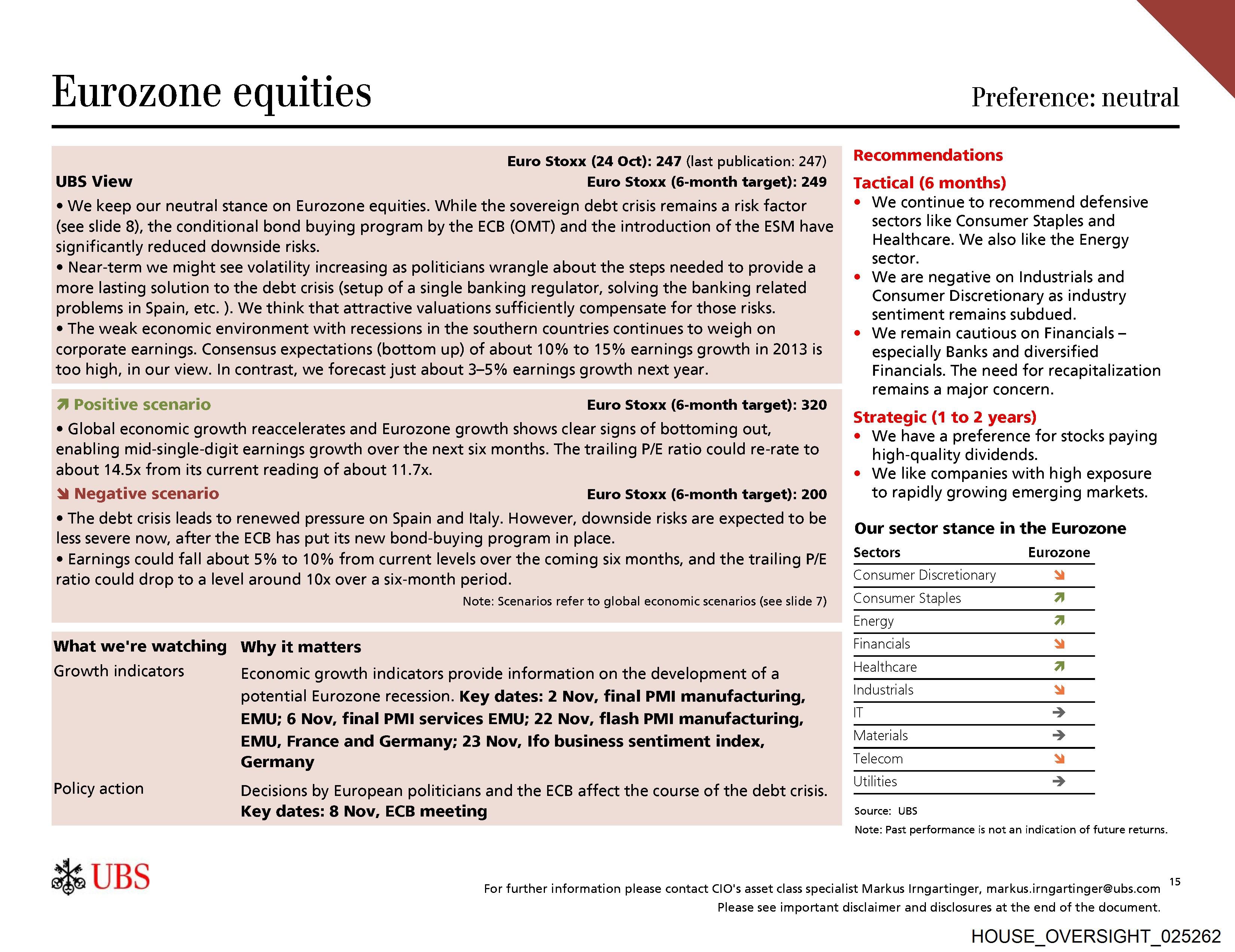

Eurozone equities

Preference: neutral

Euro Stoxx (24 Oct): 247 (last publication: 247)

UBS View Euro Stoxx (6-month target): 249

¢ We keep our neutral stance on Eurozone equities. While the sovereign debt crisis remains a risk factor

(see slide 8), the conditional bond buying program by the ECB (OMT) and the introduction of the ESM have

significantly reduced downside risks.

¢ Near-term we might see volatility increasing as politicians wrangle about the steps needed to provide a

more lasting solution to the debt crisis (setup of a single banking regulator, solving the banking related

problems in Spain, etc. ). We think that attractive valuations sufficiently compensate for those risks.

¢ The weak economic environment with recessions in the southern countries continues to weigh on

corporate earnings. Consensus expectations (bottom up) of about 10% to 15% earnings growth in 2013 is

too high, in our view. In contrast, we forecast just about 3-5% earnings growth next year.

4 Positive scenario Euro Stoxx (6-month target): 320

¢ Global economic growth reaccelerates and Eurozone growth shows clear signs of bottoming out,

enabling mid-single-digit earnings growth over the next six months. The trailing P/E ratio could re-rate to

about 14.5x from its current reading of about 11.7x.

& Negative scenario Euro Stoxx (6-month target): 200

¢ The debt crisis leads to renewed pressure on Spain and Italy. However, downside risks are expected to be

less severe now, after the ECB has put its new bond-buying program in place.

e Earnings could fall about 5% to 10% from current levels over the coming six months, and the trailing P/E

ratio could drop to a level around 10x over a six-month period.

Note: Scenarios refer to global economic scenarios (see slide 7)

What we're watching Why it matters

Growth indicators Economic growth indicators provide information on the development of a

potential Eurozone recession. Key dates: 2 Nov, final PMI manufacturing,

EMU; 6 Nov, final PMI services EMU; 22 Nov, flash PMI manufacturing,

EMU, France and Germany; 23 Nov, Ifo business sentiment index,

Germany

Policy action Decisions by European politicians and the ECB affect the course of the debt crisis.

Key dates: 8 Nov, ECB meeting

2 UBS

Recommendations

Tactical (6 months)

e We continue to recommend defensive

sectors like Consumer Staples and

Healthcare. We also like the Energy

sector.

e We are negative on Industrials and

Consumer Discretionary as industry

sentiment remains subdued.

e We remain cautious on Financials -

especially Banks and diversified

Financials. The need for recapitalization

remains a major concern.

Strategic (1 to 2 years)

e We have a preference for stocks paying

high-quality dividends.

e We like companies with high exposure

to rapidly growing emerging markets.

Our sector stance in the Eurozone

Sectors Eurozone

Consumer Discretionary

Consumer Staples

Energy

Financials

Healthcare

ndustrials

=

aterials

Telecom

Utilities

VieglvVi viel ule; ulale

Source: UBS

Note: Past performance is not an indication of future returns.

For further information please contact ClO's asset class specialist Markus Irngartinger, markus.irngartinger@ubs.com 1

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_025262

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_025262.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,296 characters |

| Indexed | 2026-02-04T16:56:38.044993 |