HOUSE_OVERSIGHT_025261.jpg

{kind=link}

Extracted Text (OCR)

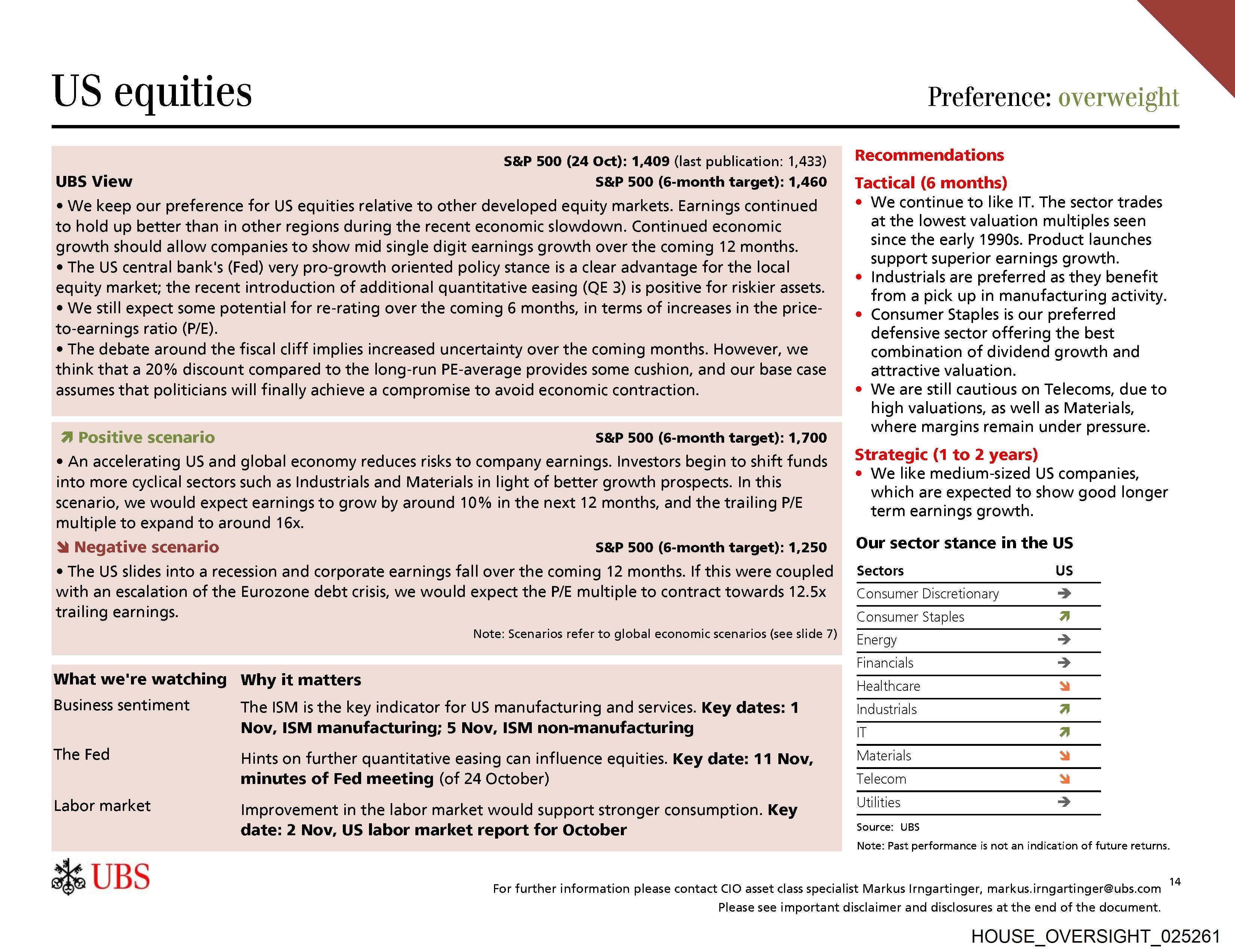

US equities

S&P 500 (24 Oct): 1,409 (last publication: 1,433)

UBS View S&P 500 (6-month target): 1,460

¢ We keep our preference for US equities relative to other developed equity markets. Earnings continued

to hold up better than in other regions during the recent economic slowdown. Continued economic

growth should allow companies to show mid single digit earnings growth over the coming 12 months.

¢ The US central bank's (Fed) very pro-growth oriented policy stance is a clear advantage for the local

equity market; the recent introduction of additional quantitative easing (QE 3) is positive for riskier assets.

° We still expect some potential for re-rating over the coming 6 months, in terms of increases in the price-

to-earnings ratio (P/E).

¢ The debate around the fiscal cliff implies increased uncertainty over the coming months. However, we

think that a 20% discount compared to the long-run PE-average provides some cushion, and our base case

assumes that politicians will finally achieve a compromise to avoid economic contraction.

4 Positive scenario S&P 500 (6-month target): 1,700

e An accelerating US and global economy reduces risks to company earnings. Investors begin to shift funds

into more cyclical sectors such as Industrials and Materials in light of better growth prospects. In this

scenario, we would expect earnings to grow by around 10% in the next 12 months, and the trailing P/E

multiple to expand to around 16x.

& Negative scenario S&P 500 (6-month target): 1,250

e The US slides into a recession and corporate earnings fall over the coming 12 months. If this were coupled

with an escalation of the Eurozone debt crisis, we would expect the P/E multiple to contract towards 12.5x

trailing earnings.

Note: Scenarios refer to global economic scenarios (see slide 7)

What we're watching Why it matters

Business sentiment The ISM is the key indicator for US manufacturing and services. Key dates: 1

Nov, ISM manufacturing; 5 Nov, ISM non-manufacturing

The Fed Hints on further quantitative easing can influence equities. Key date: 11 Nov,

minutes of Fed meeting (of 24 October)

Labor market Improvement in the labor market would support stronger consumption. Key

date: 2 Nov, US labor market report for October

2 UBS

Preference: overweight

Recommendations

Tactical (6 months)

We continue to like IT. The sector trades

at the lowest valuation multiples seen

since the early 1990s. Product launches

support superior earnings growth.

Industrials are preferred as they benefit

from a pick up in manufacturing activity.

Consumer Staples is our preferred

defensive sector offering the best

combination of dividend growth and

attractive valuation.

We are still cautious on Telecoms, due to

high valuations, as well as Materials,

where margins remain under pressure.

Strategic (1 to 2 years)

We like medium-sized US companies,

which are expected to show good longer

term earnings growth.

Our sector stance in the US

Sectors

Consumer Discretionary

Consumer Staples

Energy

Financials

T

Healthcare

ndustrials

Telecom

Utilities

aterials

Viclelulalely| vial ws

Source: UBS

Note: Past performance is not an indication of future returns.

For further information please contact ClO asset class specialist Markus Irngartinger, markus.irngartinger@ubs.com 4

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_025261

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_025261.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,407 characters |

| Indexed | 2026-02-04T16:56:38.314723 |