HOUSE_OVERSIGHT_025260.jpg

{kind=link}

Extracted Text (OCR)

Equities overview

Global equity markets - Key points

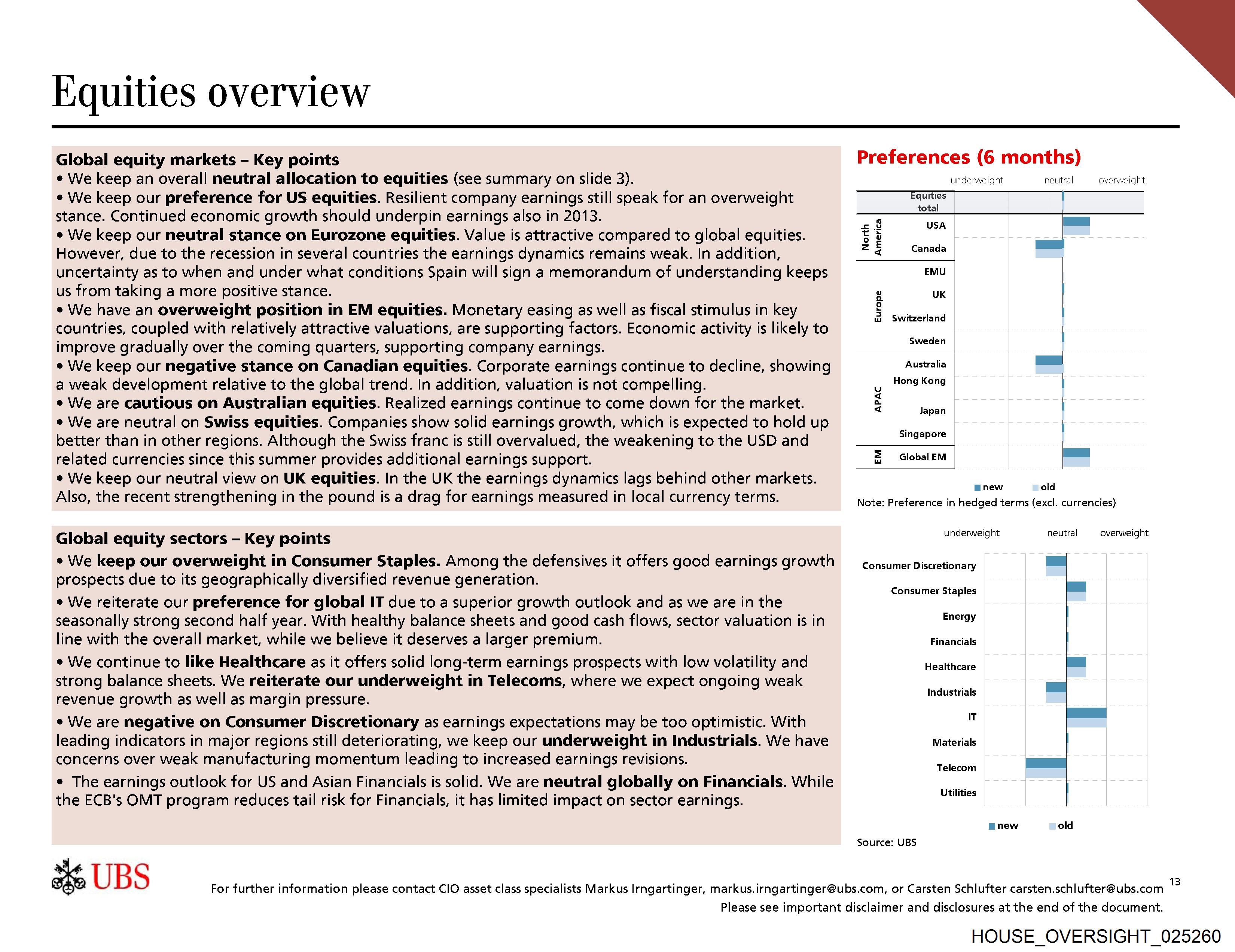

¢ We keep an overall neutral allocation to equities (see summary on slide 3).

¢ We keep our preference for US equities. Resilient company earnings still soeak for an overweight

stance. Continued economic growth should underpin earnings also in 2013.

¢ We keep our neutral stance on Eurozone equities. Value is attractive compared to global equities.

However, due to the recession in several countries the earnings dynamics remains weak. In addition,

uncertainty as to when and under what conditions Spain will sign a memorandum of understanding keeps

us from taking a more positive stance.

¢ We have an overweight position in EM equities. Monetary easing as well as fiscal stimulus in key

countries, coupled with relatively attractive valuations, are supporting factors. Economic activity is likely to

improve gradually over the coming quarters, supporting company earnings.

¢ We keep our negative stance on Canadian equities. Corporate earnings continue to decline, showing

a weak development relative to the global trend. In addition, valuation is not compelling.

¢ We are cautious on Australian equities. Realized earnings continue to come down for the market.

¢ We are neutral on Swiss equities. Companies show solid earnings growth, which is expected to hold up

better than in other regions. Although the Swiss franc is still overvalued, the weakening to the USD and

related currencies since this summer provides additional earnings support.

¢ We keep our neutral view on UK equities. In the UK the earnings dynamics lags behind other markets.

Also, the recent strengthening in the pound is a drag for earnings measured in local currency terms.

Global equity sectors - Key points

¢ We keep our overweight in Consumer Staples. Among the defensives it offers good earnings growth

prospects due to its geographically diversified revenue generation.

¢ We reiterate our preference for global IT due to a superior growth outlook and as we are in the

seasonally strong second half year. With healthy balance sheets and goad cash flows, sector valuation is in

line with the overall market, while we believe it deserves a larger premium.

¢ We continue to like Healthcare as it offers solid long-term earnings prospects with low volatility and

strong balance sheets. We reiterate our underweight in Telecoms, where we expect ongoing weak

revenue growth as well as margin pressure.

e We are negative on Consumer Discretionary as earnings expectations may be too optimistic. With

leading indicators in major regions still deteriorating, we keep our underweight in Industrials. We have

concerns over weak manufacturing momentum leading to increased earnings revisions.

¢ The earnings outlook for US and Asian Financials is solid. We are neutral globally on Financials. While

the ECB's OMT program reduces tail risk for Financials, it has limited impact on sector earnings.

2 UBS

Preferences (6 months)

underweight neutral overweight

Equities T

total

Canada

North

America

Cc

wn

>

EMU

Q UK

2

@ Switzerland

Sweden

Australia |

Hong Kong |

iS)

4

a I

zt Japan

Singapore |

= Global—EM =

Bnew old

Note: Preference in hedged terms (excl. currencies)

underweight neutral overweight

Consumer Discretionary =

Consumer Staples =a

Energy |

Financials |

Healthcare =

Industrials |

IT |

Materials |

Telecom Ss

Utilities |

mnew old

Source: UBS

For further information please contact ClO asset class specialists Markus Irngartinger, markus.irngartinger@ubs.com, or Carsten Schlufter carsten.schlufter@ubs.com 18

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_025260

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_025260.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,667 characters |

| Indexed | 2026-02-04T16:56:38.673569 |