HOUSE_OVERSIGHT_025267.jpg

{kind=link}

Extracted Text (OCR)

Asian equities (ex-Japan)

MSCI Asia ex-Japan (24 Oct): 518 (last publication: 510)

UBS view MSCI Asia ex-Japan (6-month target): 545

¢ China released a set of positive data for September. While the headline 3Q GDP number only met

expectations at +7.4% YoY (consensus +7.4%, prior +7.6%), the higher frequency data was better.

Industrial production of +9.2% YoY (consensus +9.0%, prior +8.9%), retail sales of +14.2% YoY

(consensus +13.2%, prior +13.2%), and fixed asset investment of +20.5% (+20.2% consensus, prior

+20.2%) all came in higher.

Chinese H-Shares are up almost 10% in the last month, while the S&P 500 is within 0.4 index points of

where it was a month ago. Valuations of MSCI China remain extremely attractive as the market

continues to price in a hard landing scenario, although sentiment is clearly turning. In India, the

government has proposed several key economic reforms, but there are implementation risks and

consensus GDP forecasts still have downside risk, while Indonesia's economic momentum is on track.

We expect 12.8% earnings-per-share growth over 12 months for the MSCI Asia ex-Japan. It trades on

11.0x 12-m forward earnings and 1.6x price-to-book. We expect a stable earnings multiple in the next six

months. Economic growth should stabilize and earnings downgrades come to an end toward the end of

2012.

A Positive scenario MSCI Asia ex-Japan (6-month target): 670

e More supportive monetary and fiscal policy, stable inflation, sustained domestic demand growth, and an

improved global growth outlook lead to a better earnings outlook. In such a scenario, we expect

earnings growth of 15% and a trailing P/E of about 15.0x.

& Negative scenario MSCI Asia ex-Japan (6-month target): 400

e A hard landing in China with a global recession leads to negative earnings revisions for 2012. In this

scenario, Asia ex-Japan could trade down to about 10.5x realized earnings.

What we're watching Why it matters

Politics Leadership in China is set to change, resulting in a newly defined future

economic policy. The US Presidential elections have implications on the

outcome of the Fiscal Cliff. Key dates: Nov 6, 57" US Presidential

Elections; Nov 8, 18" Communist Party Congress

Policy responses Some other countries in the region have near-term macroeconomic issues due

to fiscal and current account deficits, as well as hiccups in market and economic

reforms. Policy responses often come on an ad-hoc basis.

2 UBS

Recommendations

Tactical (6 months)

° The Fed's implementation of QE3 provides

support to Asia ex-Japan equities. In

conjunction with improving growth

prospects we see good near term upside.

Should economic growth surprise to the

upside, more defensive markets such as

Singapore and Malaysia are likely to

underperform. Instead, higher beta,

export-oriented markets like South Korea,

Taiwan, Hong Kong and China are likely to

take advantage from a strengthening in

global growth.

Strategic (1 to 2 years)

¢ Consider a portfolio mix of high yield

stocks largely found in Singapore, Taiwan

& HK, complemented by growth-oriented

stocks in the rest of Asia.

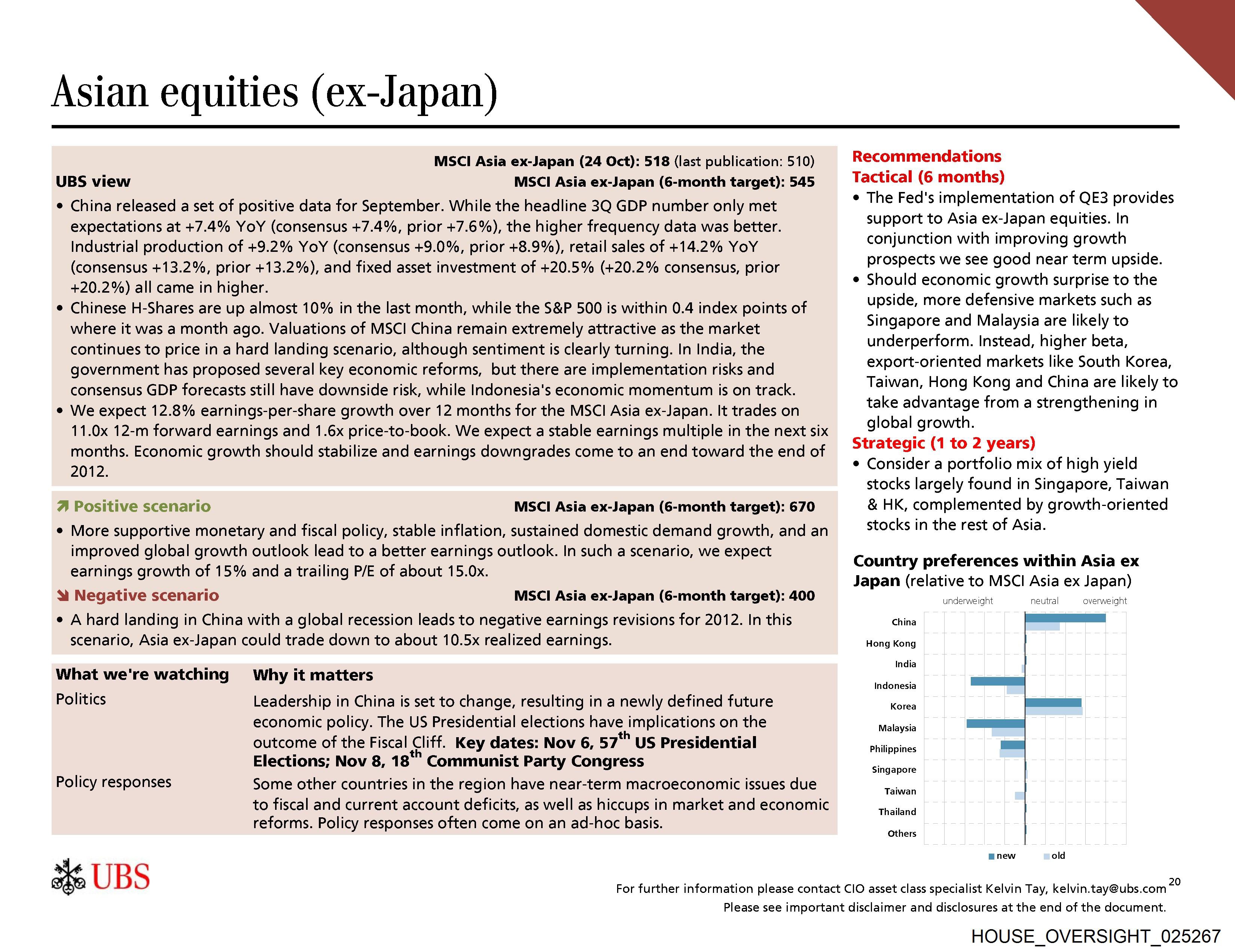

Country preferences within Asia ex

Japan (relative to MSCI Asia ex Japan)

underweight neutral overweight

China —————]

Hong Kong

India

Indonesia |

Korea a

Malaysia Saaz

Philippines fz

Singapore

Taiwan

Thailand

Others

Bnew old

For further information please contact ClO asset class specialist Kelvin Tay, kelvin.tay@ubs.com 20

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_025267

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_025267.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,551 characters |

| Indexed | 2026-02-04T16:56:39.481645 |