HOUSE_OVERSIGHT_025988.jpg

{kind=link}

Extracted Text (OCR)

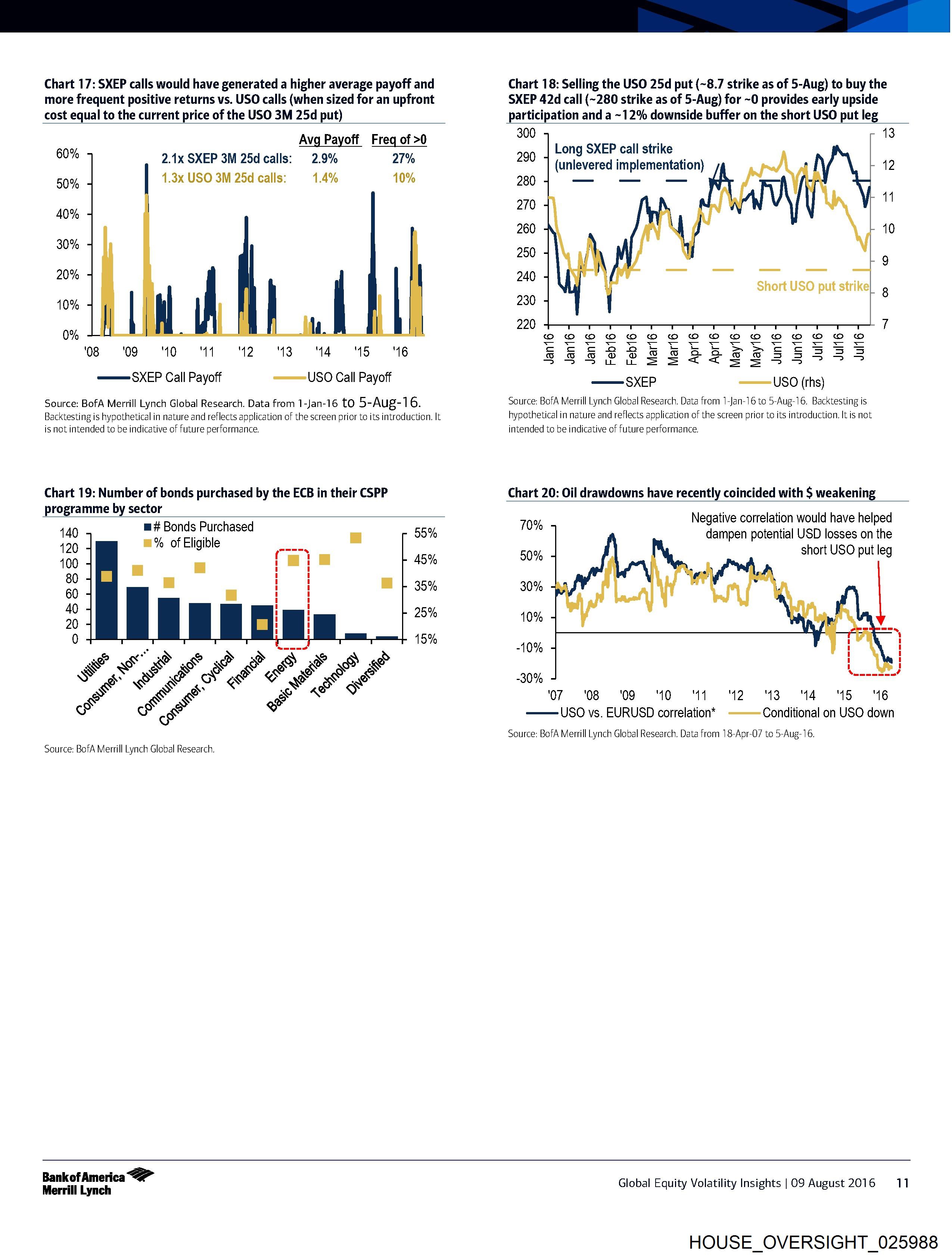

Chart 17: SXEP calls would have generated a higher average payoff and

more frequent positive returns vs. USO calls (when sized for an upfront

cost equal to the current price of the USO 3M 25d put)

Avg Payoff Freq of >0

2.1x SXEP 3M 25d calls: 2.9% 27%

1.3x USO 3M 25d calls: 1.4% 10%

60%

50%

40%

30%

20%

10%

0%

08 09 ‘10 M40 ‘12138 141516

SXEP Call Payoff = USO Call Payoff

Source: BofA Merrill Lynch Global Research. Data from 1-Jan-16 to 5-Aug-1 6.

Backtesting is hypothetical in nature and reflects application of the screen prior to its introduction. It

is not intended to be indicative of future performance.

Chart 19: Number of bonds purchased by the ECB in their CSPP

programme by sector

Chart 18: Selling the USO 25d put (~8.7 strike as of 5-Aug) to buy the

SXEP 42d call (~280 strike as of 5-Aug) for ~0 provides early upside

participation and a ~12% downside buffer on the short USO put leg

300

290

280

270

260

290

240

13

Long SXEP call strike

(unlevered implementation) 12

Short USO put strike|_ 9

230

220 7

oo owo ©O©§ 0 © © © © © © © © © ©

SEESSEEEEEEESS35

SXEP ——USO (rhs)

Source: BofA Merrill Lynch Global Research. Data from 1-Jan-16 to 5-Aug-16. Backtesting is

hypothetical in nature and reflects application of the screen prior to its introduction. It is not

intended to be indicative of future performance.

Chart 20: Oil drawdowns have recently coincided with $ weakening

25%

15%

440 m# Bonds Purchased 55%

138 m% of Eligible __. a °

400 - = { aie 45%

80 o i H |

35%

60 _ °

yt

a 1

1 1

Source: BofA Merrill Lynch Global Research.

Negative correlation would have helped

dampen potential USD losses on the

short USO put leg

70%

50%

30%

10%

10% 1

i

I

-30% saeeter

‘O7 08 09 10 11 12— 13 1415 16

USO vs. EURUSD correlation* Conditional on USO down

Source: BofA Merrill Lynch Global Research. Data from 18-Apr-07 to 5-Aug-16.

Bankof America

Merrill Lynch

Global Equity Volatility Insights |O9 August 2016 =-11

HOUSE_OVERSIGHT_025988

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_025988.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 1,972 characters |

| Indexed | 2026-02-04T16:58:09.175046 |