HOUSE_OVERSIGHT_025987.jpg

{kind=link}

Extracted Text (OCR)

Volatility in Europe

Buy the seasonal oil dip via bullish X-market risk reversals

Levered X-market risk reversal: Sell 1x USO 3M 25d (~88% strike) puts

to fully fund 2.1x SXEP (Oil & Gas equity) 25d (~106% strike) calls (indic.)

Alternative (unlevered) implementation: Sell USO 25d puts to fund fully

fund closer to the money SXEP calls

The seasonal sell-off in oil presents a ‘buy the dip’ opportunity according to our

commodity strategists, who expect prices to rebound to $55/bbl by year end. In fact

current levels of ~S40 are close to the summer floor ($39) they had previously

suggested.

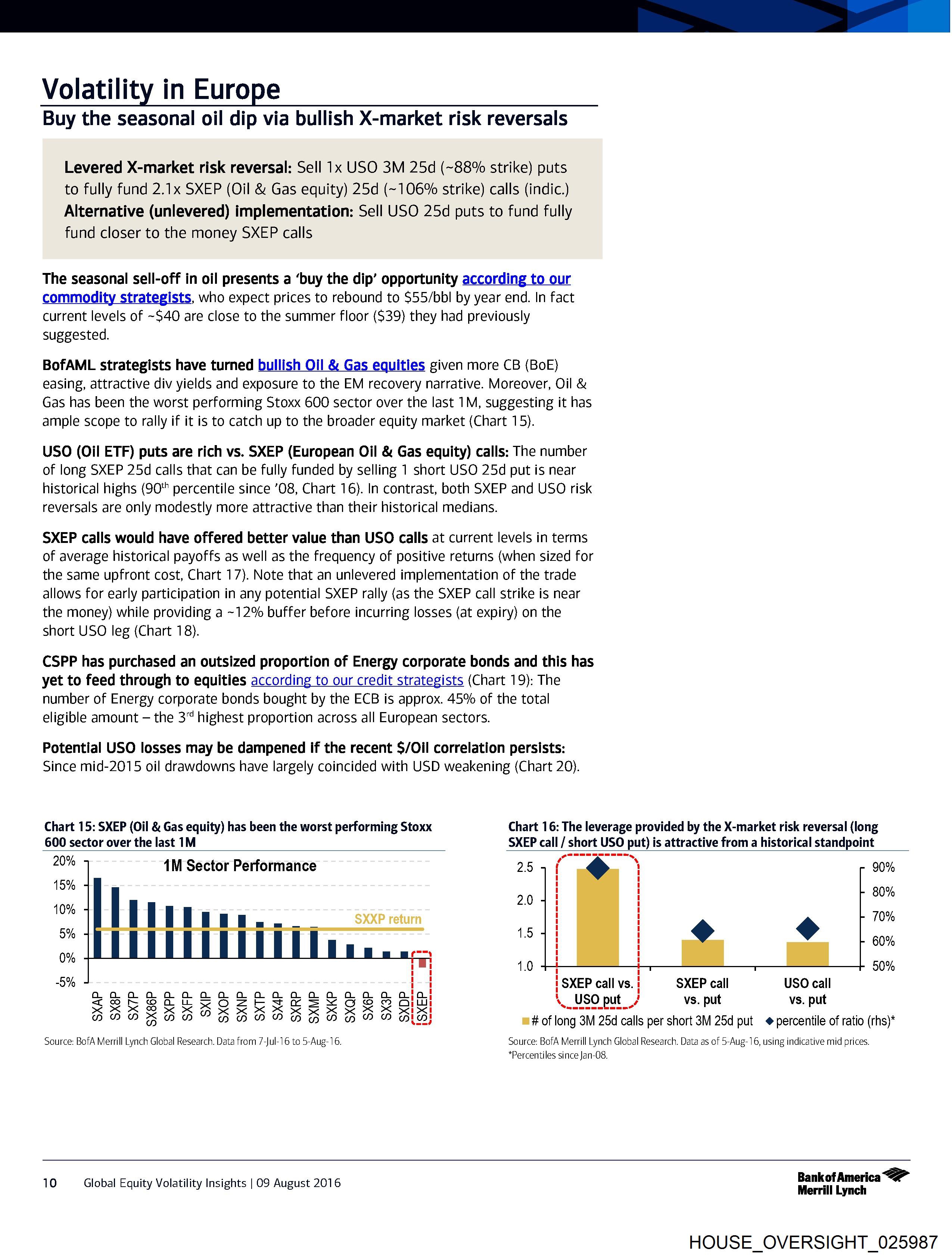

BofAML strategists have turned bullish Oil & Gas equities given more CB (BoE)

easing, attractive div yields and exposure to the EM recovery narrative. Moreover, Oil &

Gas has been the worst performing Stoxx 600 sector over the last 1M, suggesting it has

ample scope to rally if it is to catch up to the broader equity market (Chart 15).

USO (Oil ETF) puts are rich vs. SXEP (European Oil & Gas equity) calls: The number

of long SXEP 25d calls that can be fully funded by selling 1 short USO 25d put is near

historical highs (90" percentile since ’08, Chart 16). In contrast, both SXEP and USO risk

reversals are only modestly more attractive than their historical medians.

SXEP calls would have offered better value than USO calls at current levels in terms

of average historical payoffs as well as the frequency of positive returns (when sized for

the same upfront cost, Chart 17). Note that an unlevered implementation of the trade

allows for early participation in any potential SXEP rally (as the SXEP call strike is near

the money) while providing a ~12% buffer before incurring losses (at expiry) on the

short USO leg (Chart 18).

CSPP has purchased an outsized proportion of Energy corporate bonds and this has

yet to feed through to equities according to our credit strategists (Chart 19): The

number of Energy corporate bonds bought by the ECB is approx. 45% of the total

eligible amount — the 3“ highest proportion across all European sectors.

Potential USO losses may be dampened if the recent $/Oil correlation persists:

Since mid-2015 oil drawdowns have largely coincided with USD weakening (Chart 20).

Chart 15: SXEP (Oil & Gas equity) has been the worst performing Stoxx Chart 16: The leverage provided by the X-market risk reversal (long

600 sector over the last 1M SXEP call / short USO put) is attractive from a historical standpoint

20% 1M Sector Performance 254 : 90%

15%

10%

5%

80%

SXXP return 10%

60%

0% ny

rw 1.0 50%

5% it SXEP call vs. SXEP call USO call

ZSebr-eveantRoZzerTeresxocee au VS. pu VS. pu

BOM BBAK SM SBSKSKRRABMS ape oa . .

” GPP TN BAAOOD DOW DY; m# of long 3M 25d calls per short 3M 25d put + percentile of ratio (rhs)*

Source: BofA Merrill Lynch Global Research. Data from 7-Jul-16 to 5-Aug-16. Source: BofA Merrill Lynch Global Research. Data as of 5-Aug-16, using indicative mid prices.

*Percentiles since Jan-08.

BankofAmerica <2”

10 Global Equity Volatility Insights | O09 August 2016 Merrill Lynch

HOUSE_OVERSIGHT_025987

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_025987.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,075 characters |

| Indexed | 2026-02-04T16:58:09.950347 |