HOUSE_OVERSIGHT_026150.jpg

{kind=link}

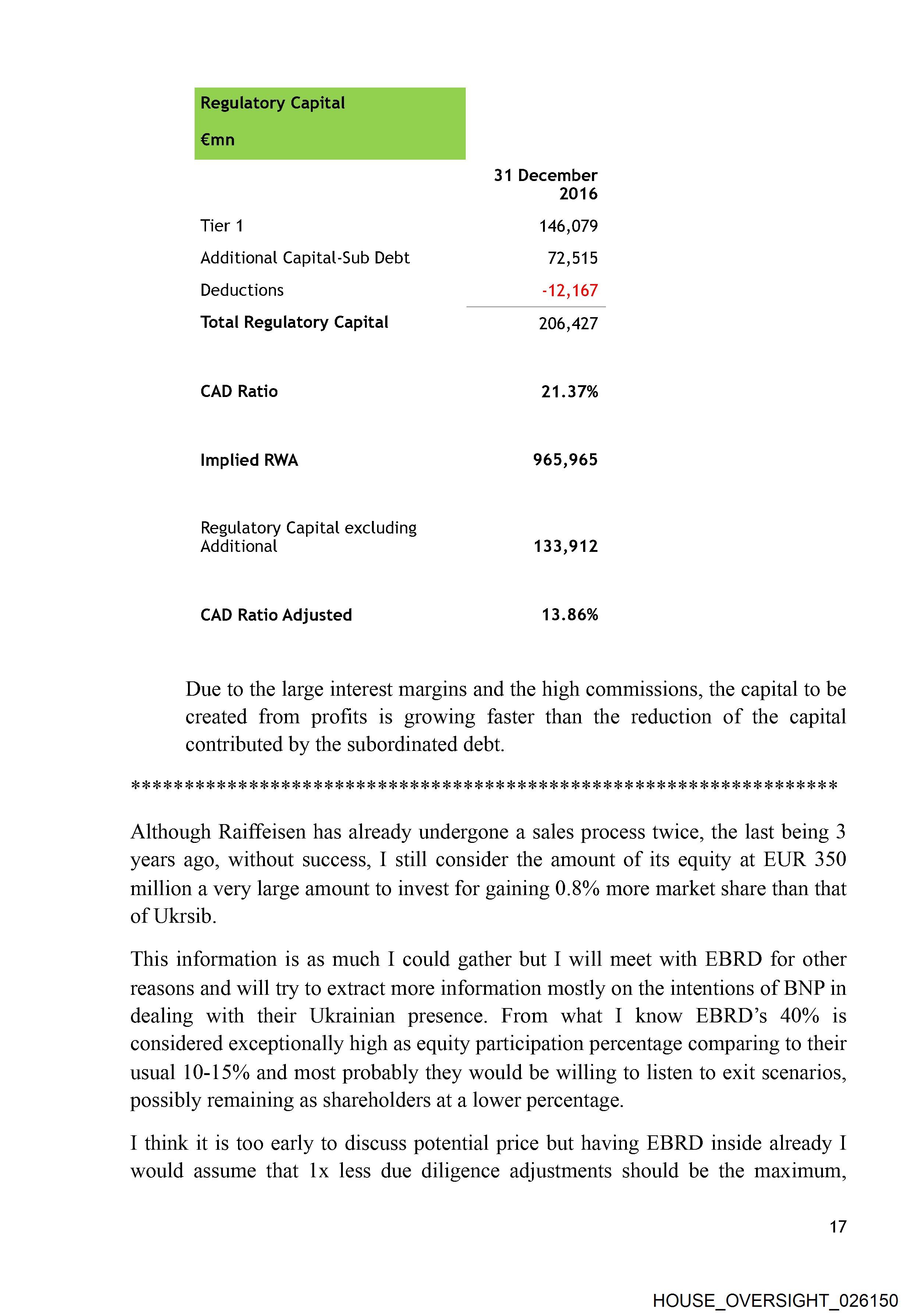

Extracted Text (OCR)

31 December

2016

Tier 1 146,079

Additional Capital-Sub Debt 72,515

Deductions -12,167

Total Regulatory Capital 206,427

CAD Ratio 21.37%

Implied RWA 965,965

Regulatory Capital excluding

Additional 133,912

CAD Ratio Adjusted 13.86%

Due to the large interest margins and the high commissions, the capital to be

created from profits is growing faster than the reduction of the capital

contributed by the subordinated debt.

3s 2k ig 2k 2s ie 2k ie ois ie 2s 2s 2c 2s 2c 2s 2c ok ie 2k 2 ok 2 2c 2s 2k fe 2c fe 2 ois 2 ois 2k ois ie 2k ie 2s 2s 2s ois 2k ois 2k is 2c os ie ok ke ok ie 2 2s 2 2g 2 at ok ok 2 ok ok ok ok

Although Raiffeisen has already undergone a sales process twice, the last being 3

years ago, without success, I still consider the amount of its equity at EUR 350

million a very large amount to invest for gaining 0.8% more market share than that

of Ukrsib.

This information is as much I could gather but I will meet with EBRD for other

reasons and will try to extract more information mostly on the intentions of BNP in

dealing with their Ukrainian presence. From what I know EBRD’s 40% is

considered exceptionally high as equity participation percentage comparing to their

usual 10-15% and most probably they would be willing to listen to exit scenarios,

possibly remaining as shareholders at a lower percentage.

I think it is too early to discuss potential price but having EBRD inside already I

would assume that 1x less due diligence adjustments should be the maximum,

17

HOUSE_OVERSIGHT_026150

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_026150.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 1,523 characters |

| Indexed | 2026-02-04T16:58:31.019403 |

Related Documents

Documents connected by shared names, same document type, or nearby in the archive.