HOUSE_OVERSIGHT_026699.jpg

{kind=link}

Extracted Text (OCR)

Sovereigns see potential in Indian private markets

Despite tactical switching between developed

markets, increasing investment into emerging markets

remains a long-term strategic objective for many

sovereigns (as stated in our 2016 report). Stock

markets have relatively small coverage of emerging

market economies, driving greater emphasis on

illiquid real asset categories. In fact, many sovereigns

use infrastructure deals to manage near-term macro

and geopolitical risk, as outlined in our 2015 study.

However, challenging placement dynamics and

uncertainty over commodity prices mean sovereigns

are being more selective in their emerging market

investments, focusing on the identification of high-

growth markets.

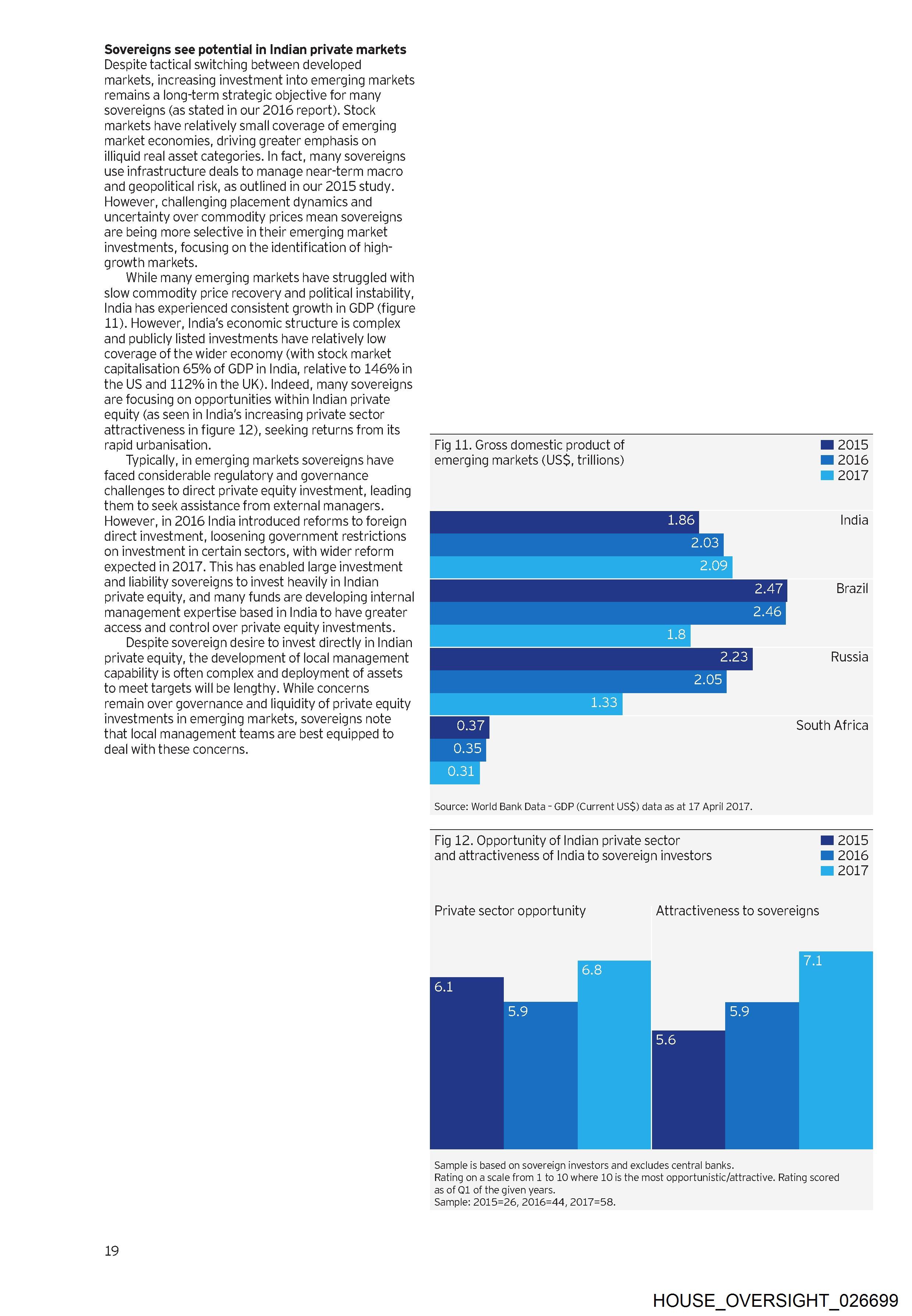

While many emerging markets have struggled with

slow commodity price recovery and political instability,

India has experienced consistent growth in GDP (figure

11). However, India’s economic structure is complex

and publicly listed investments have relatively low

coverage of the wider economy (with stock market

capitalisation 65% of GDP in India, relative to 146% in

the US and 112% in the Uk). Indeed, many sovereigns

are focusing on opportunities within Indian private

equity (as seen in India’s increasing private sector

attractiveness in figure 12), seeking returns from its

rapid urbanisation.

Typically, in emerging markets sovereigns have

faced considerable regulatory and governance

challenges to direct private equity investment, leading

them to seek assistance from external managers.

However, in 2016 India introduced reforms to foreign

direct investment, loosening government restrictions

on investment in certain sectors, with wider reform

expected in 2017. This has enabled large investment

and liability sovereigns to invest heavily in Indian

private equity, and many funds are developing internal

management expertise based in India to have greater

access and control over private equity investments.

Despite sovereign desire to invest directly in Indian

private equity, the development of local management

capability is often complex and deployment of assets

to meet targets will be lengthy. While concerns

remain over governance and liquidity of private equity

investments in emerging markets, sovereigns note

that local management teams are best equipped to

deal with these concerns.

19

Fig 11. Gross domestic product of mM 2015

emerging markets (USS, trillions) @ 2016

@ 2017

India

Brazil

Russia

South Africa

O31

Source: World Bank Data - GDP (Current USS) data as at 17 April 2017.

Fig 12. Opportunity of Indian private sector M@ 2015

and attractiveness of India to sovereign investors @ 2016

m 2017

Private sector opportunity Attractiveness to sovereigns

Sample is based on sovereign investors and excludes central banks.

Rating on a scale from 1 to 10 where 10 is the most opportunistic/attractive. Rating scored

as of Q1 of the given years.

Sample: 2015=26, 2016=44, 2017=58.

HOUSE_OVERSIGHT_026699

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_026699.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 2,955 characters |

| Indexed | 2026-02-04T16:59:41.359857 |