HOUSE_OVERSIGHT_025286.jpg

{kind=link}

Extracted Text (OCR)

Preference: neutral

Listed real estate

Recommendations

Tactical (6 months)

e We continue to be neutral global listed

UBS Global Index DTR (24 Oct): 1,490 (last month: 1,500)

UBS View UBS Global Index DTR (6-month target): 1,600

¢ Since July global listed real estate has again performed well. Despite the good performance the asset class

remains slightly attractive based the high dividend yield and implied property yield compared to bonds.

Asia has been the strongest performer and Europe has outperformed the US year-to-date as tail risk was

reduced by the ECB launching the OMT. QE3 is not an imminent performance driver but provides a support

for capital values going forward and helps to keep interest levels low.

¢ Due to the current search for yields, listed real estate companies are able to refinance their investments at

lower yields with longer maturities. The implied property yields to bonds and earnings yields over five-year

swap rates are even more attractive due to low interest rates offering good opportunities within the global

real estate recommending to have

exposure to the Hong Kong, Singapore

and Australia markets. The asset class is

overall slightly attractive on relative

valuation and the current low interest

rate is supportive, but the uncertain

environment warrants a neutral stance.

Strategic (1 to 2 years)

e Real estate is supported by several factors

in the long term. We anticipate a gradual

increase in payout ratios coupled with

portfolio optimizations and ongoing cost-

cutting. A weak economy limits strong

rental growth, but low supply supports

high occupancy rates keeping rents up.

real estate space.

e Low to decent supply of commercial surfaces helps to push vacancy rates down which in turn increases

the rent. We further see capital appreciation as possible in the light of overall stable fundamentals.

e Asia remain the positive performance generators in our view as this is the more cyclical market, whereas

Australia is supported by high dividend yields. Overall Europe remains comparatively weak, while the UK

and the US have already priced in some market improvements.

4 Positive scenario UBS Global Index DTR (6-month target): 1,650

¢ Improving fundamentals maintain listed real estate in fairly valued territory, despite stronger

performance as occupancy rates grow faster than expected and rental income accelerate. Ongoing

reflationary monetary policies across the world help to maintain favorable spreads between rental yields

and bonds, maintaining real estate as a comparatively attractive asset class. Refinancing costs remain low.

& Negative scenario UBS Global Index DTR (6-month target): 1,300

e US, European and Chinese growth rates disappoint investor expectations and cause the comparatively

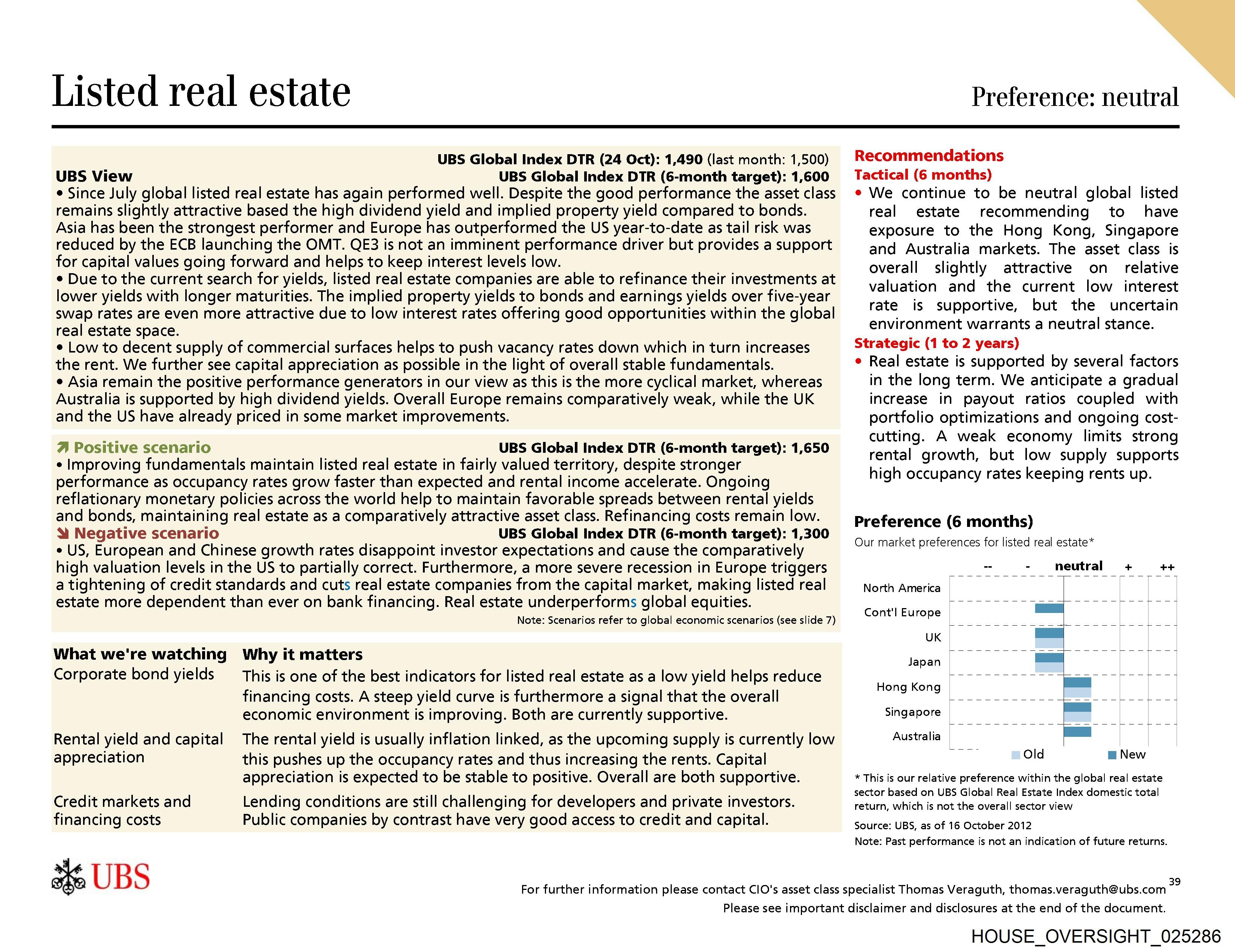

Preference (6 months)

Our market preferences for listed real estate*

high valuation levels in the US to partially correct. Furthermore, a more severe recession in Europe triggers — oom neutral + ++

a tightening of credit standards and cuts real estate companies from the capital market, making listed real North America

estate more dependent than ever on bank financing. Real estate underperforms global equities. eee eeg PME EETG —-- oro

Note: Scenarios refer to global economic scenarios (see slide 7) ContlEurope | ee ee |

UK ||

What we're watching Why it matters japan Cid = COU

Corporate bond yields _ This is one of the best indicators for listed real estate as a low yield helps reduce Honakena mee

financing costs. A steep yield curve is furthermore a signal that the overall i i ee 2

economic environment is improving. Both are currently supportive. Singapote | eee we EB ff

Rental yield and capital The rental yield is usually inflation linked, as the upcoming supply is currently low Australia 7 —_

a Oo m New

appreciation this pushes up the occupancy rates and thus increasing the rents. Capital

appreciation is expected to be stable to positive. Overall are both supportive.

Lending conditions are still challenging for developers and private investors.

Public companies by contrast have very good access to credit and capital.

* This is our relative preference within the global real estate

sector based on UBS Global Real Estate Index domestic total

return, which is not the overall sector view

Source: UBS, as of 16 Octeber 2012

Note: Past performance is not an indication of future returns.

Credit markets and

financing costs

2 UBS

For further information please contact CIO's asset class specialist Thomas Veraguth, thomas.veraguth@ubs.com

Please see important disclaimer and disclosures at the end of the document.

HOUSE_OVERSIGHT_025286

Document Preview

Click to view full size

Extracted Information

Email Addresses

Document Details

| Filename | HOUSE_OVERSIGHT_025286.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 4,642 characters |

| Indexed | 2026-02-04T16:56:43.662946 |

Related Documents

Documents connected by shared names, same document type, or nearby in the archive.