HOUSE_OVERSIGHT_014451.jpg

{kind=link}

Extracted Text (OCR)

Healthcare’s forward PE is now down to just a 7% premium relative to the market and

nearing the valuation lows recorded in 2010-12 when the patent cliff was at its worst

and pipelines were very weak. Today pipelines are twice the size they were in 2011 and

innovation is the key to growth in the sector - pricing power remains strong in drug

categories with differentiated products.

Credit: Long Spreads in Europe and US

Europe: Long Xover short Main

Rate cuts are off the table it seems, as central banks are starting to recognise the side

effects of NIRP. This reinforces our view that a continuation of CSPP, entails that the

reach for yield will extend to those assets that have not seen it yet; long Crossover vs

iTraxx Main.

The beta outperformance has already started in the cash market. We look at synthetics

and we see that Crossover has not mirrored that performance. Even though XO has

outperformed recently, it still has further to go to close the gap vs cash market’s

performance.

loannis Angelakis thinks that rising political risks in the following twelve months are

more likely to weigh on iTraxx Main performance than Crossover, as Main has higher

concentration vs XO on names domiciled in countries with elections.

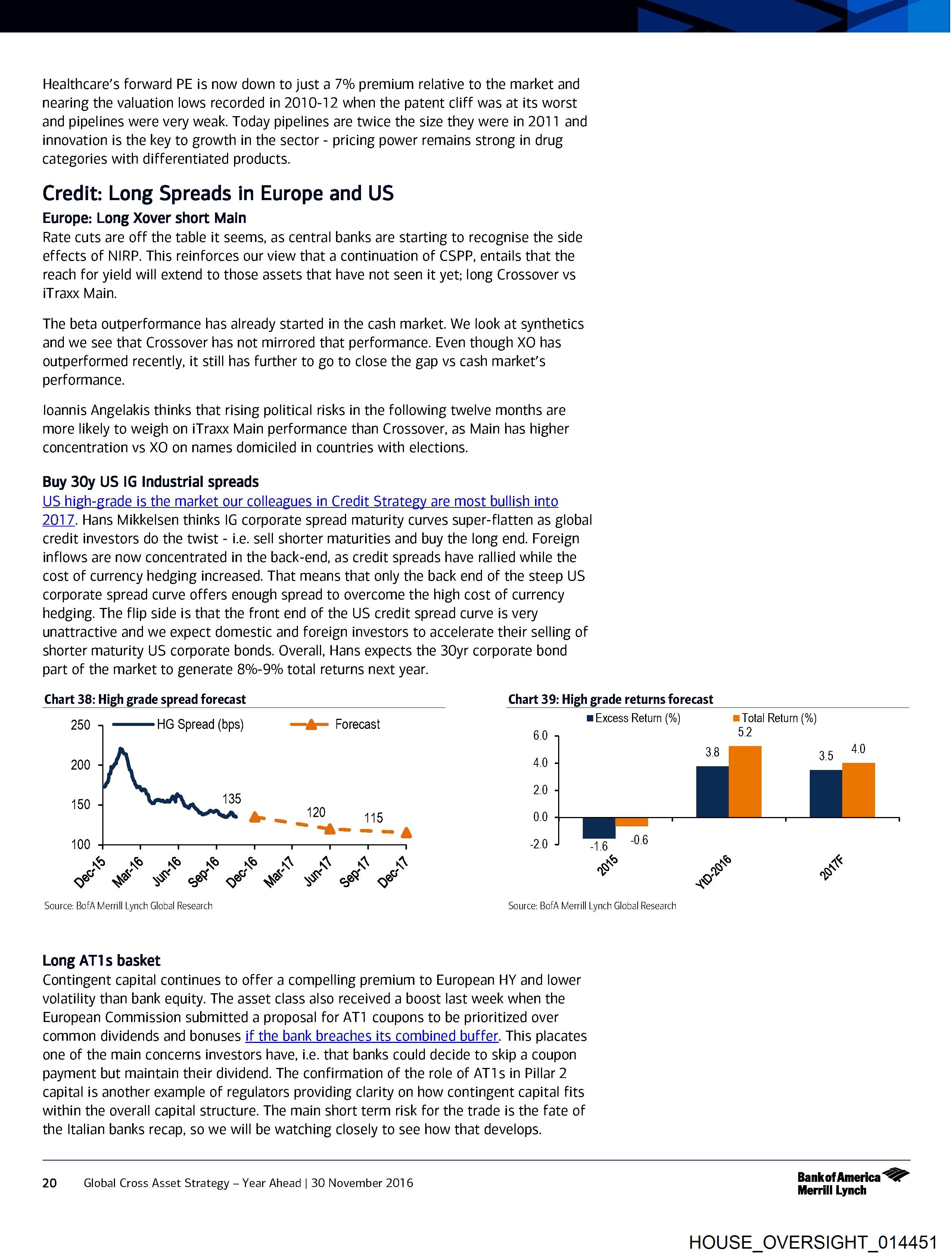

Buy 30y US IG Industrial spreads

US high-grade is the market our colleagues in Credit Strategy are most bullish into

2017. Hans Mikkelsen thinks IG corporate spread maturity curves super-flatten as global

credit investors do the twist - i.e. sell shorter maturities and buy the long end. Foreign

inflows are now concentrated in the back-end, as credit spreads have rallied while the

cost of currency hedging increased. That means that only the back end of the steep US

corporate spread curve offers enough spread to overcome the high cost of currency

hedging. The flip side is that the front end of the US credit spread curve is very

unattractive and we expect domestic and foreign investors to accelerate their selling of

shorter maturity US corporate bonds. Overall, Hans expects the 30yr corporate bond

part of the market to generate 8%-9% total returns next year.

Chart 38: High grade spread forecast Chart 39: High grade returns forecast

250

6.0

2.0

0.0

-2.0

Oo © SF FS SB KN KN N XN

a ve \ Se Ra we Se Ra

Source: BofA Merrill Lynch Global Research Source: BofA Merrill Lynch Global Research

Long AT1s basket

Contingent capital continues to offer a compelling premium to European HY and lower

volatility than bank equity. The asset class also received a boost last week when the

European Commission submitted a proposal for AT1 coupons to be prioritized over

common dividends and bonuses if the bank breaches its combined buffer. This placates

one of the main concerns investors have, i.e. that banks could decide to skip a coupon

payment but maintain their dividend. The confirmation of the role of AT1s in Pillar 2

capital is another example of regulators providing clarity on how contingent capital fits

within the overall capital structure. The main short term risk for the trade is the fate of

the Italian banks recap, so we will be watching closely to see how that develops.

HG Spread (bps) ——#— Forecast wExcess Return (%)

= Total Return (%)

5.2

20 Global Cross Asset Strategy - Year Ahead | 30 November 2016

BankofAmerica <2”

Merrill Lynch

HOUSE_OVERSIGHT_014451

Document Preview

Click to view full size

Document Details

| Filename | HOUSE_OVERSIGHT_014451.jpg |

| File Size | 0.0 KB |

| OCR Confidence | 85.0% |

| Has Readable Text | Yes |

| Text Length | 3,329 characters |

| Indexed | 2026-02-04T16:22:32.570362 |

Related Documents

Documents connected by shared names, same document type, or nearby in the archive.